All I want to know is where my Capital is going to Die

All I want to know is where my Capital is going to Die

The 3 paths you should avoid at all costs and the 3 paths you should explore

All I Want To Know Is Where I'm Going To Die So I'll Never Go There - Charlie Munger

We are going to discuss the 6 popular paths every market participant takes. You are also likely to take one of these 6 paths in your journey. Some of these paths are dangerous for your capital and you should avoid them. Understanding these paths will help you set realistic goals and expectations.

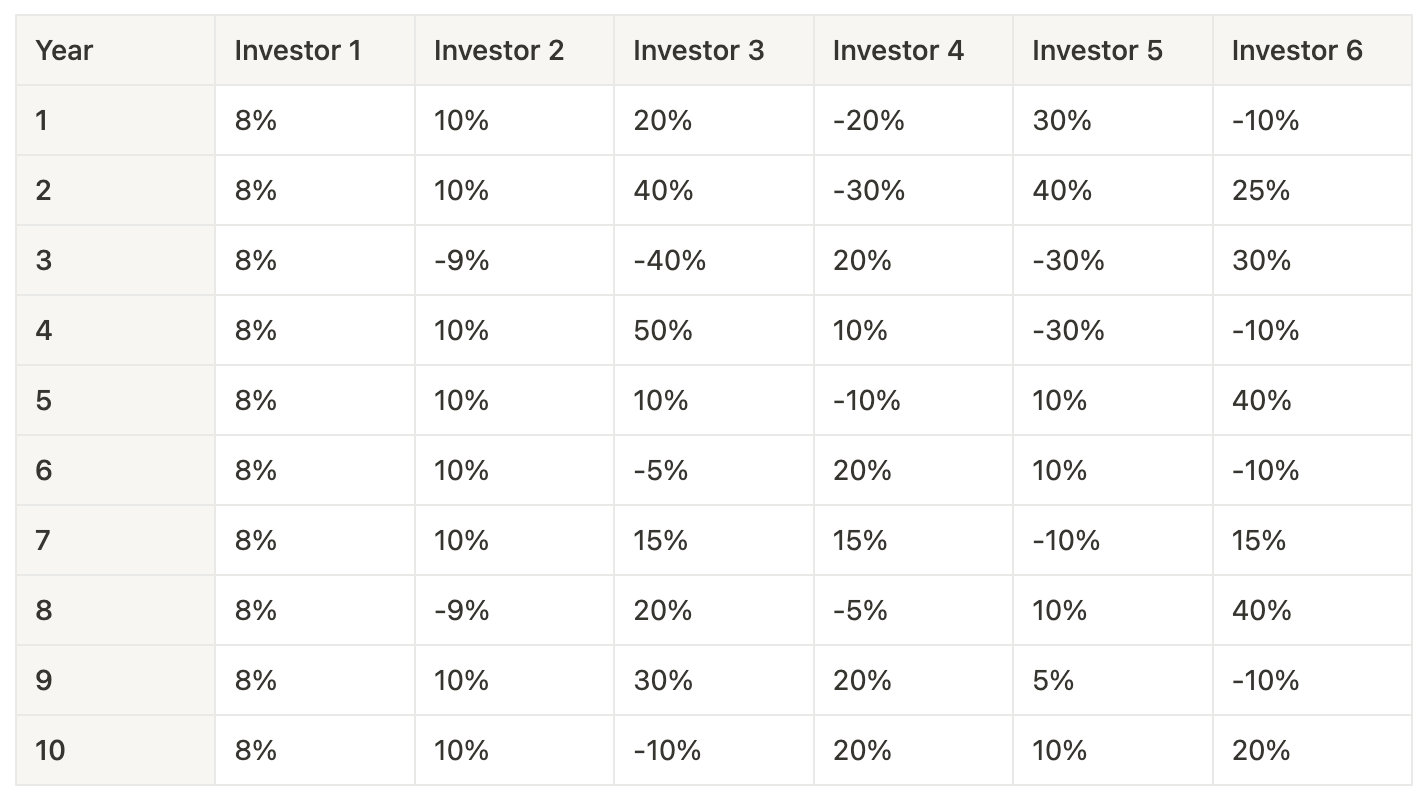

Let’s start. Below is a table with 6 different types of Market Participants who have taken different paths. The returns achieved by these Participants every year are tabulated below.

Now, just by reading the table can you guess which Investor made the best return in the last 10 years? Do not try to do extensive calculations. Just try to answer intuitively.

There is a simple way to think about this. All you have to check is who was the best in controlling the downside losses and at the same time grabbed those big wins in certain years.

For example, Investor 4 and Investor 5 have not been good at cutting losses. They have lost -20% to -30% of their capital in multiple years. Unlikely for them to end up winning.

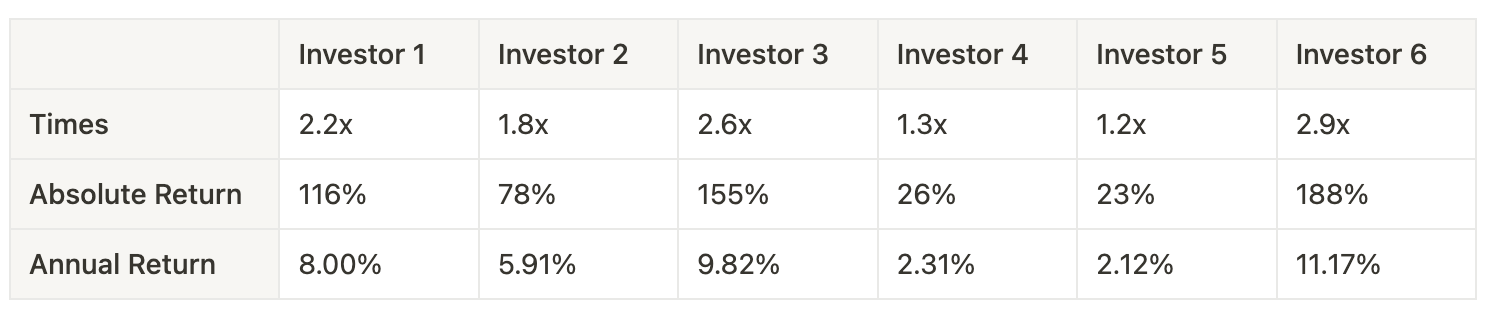

Here is the performance of all the 6 Investors.

Investor 6 is the winner. Investor 6 has been good in both cutting losses and getting those big wins.

Remember, Investor 6 is the winner based on Returns alone. But we need to evaluate these paths not only based on Returns but also on Time Spent, Stress Levels, Behavioural Difficulty & Regret. Let us look at each path in greater detail based on the above parameters.

Investor 1 - The Fixed Income Investor

Investor 1 gets a consistent 8% every year by investing in Fixed Income Instruments/Fixed Deposits/PPF etc. Managed to beat Investors 2,4 and 5 by a big margin.

Let us evaluate the path of Investor 1.

Time Spent- Almost Negligible

Stress Levels- Peaceful and Stress-Free

Return - Almost risk-free Return with no drawdowns.

Behavioural Difficulty - Low. Returns are not volatile and almost risk-free. No chance of impulse behaviour.

Regret - You won’t regret investing a part of your income in fixed-income instruments ever.

My mother taught me the biggest lesson of my life. She was at the clerical level throughout her career in a public-sector bank with a salary enough to sustain both of us. Unfortunately, my father was not with us. So, she had to manage everything by herself. She built a huge corpus at the time of her retirement with a very average salary.

How did she do it?

Invested only in Fixed Deposits, Savings Certificates & Savings Schemes.

No investments in the stock market at all.

Compounded money at ~8% for 35 years without a single loss-making year.

Controlled Expenses well and managed unexpected events through Insurance.

No Debt. No Credit cards.

Consistent and Disciplined in her approach.

Had realistic expectations, well-defined goals and plans.

She bought a house, gave me the best possible education and is now sitting on a pile of cash after all this. She outperformed the goals she set out at the beginning of her career and exceeded her expectations.

More than everything, she was content and happy with what she had all her life. No Greed. No Fear. No Regret.

I see people mocking Fixed Deposits on social media. There are some misconceptions about FDs and how inflation is a serious threat to FD investors etc. I will clarify those in another post.

Verdict: Fixed Income Investing is highly underrated and it should be a good part of any solid portfolio.

Investor 2

This type of Investor is a conservative Stock Picker. The person is good at cutting losses or exiting stocks before a big drawdown. However, this Investor is not good in letting the winners run.

One of the important models you need to keep in mind when it comes to Investing as well as Trading is “Asymmetry of Profits and Losses”. You need to get those big winners at some point to offset the losers. If your wins and losses are of a similar percentage, it is unlikely for you to outperform unless you have an extraordinary win rate.

Also, this type of Investor might think that they need to beat FD returns every single year. That is not how the market works. The market might underperform FDs for multiple years, but it will make a huge move in the subsequent years to make up for it. If you stop that from happening by not holding on to your profitable bets, you are putting your portfolio at risk.

Let us evaluate the path of Investor 2.

Time Spent- High. Significant time analysing and picking stocks.

Stress Levels- High. Frequent buying and selling involved.

Return - Poor. Unlikely to even beat FDs. Transaction costs are also high. Taxes to be paid every year. Compounding is hurt in every way possible by Investor 2.

Behavioural Difficulty - High.

Regret - High. When an investment doubles after you exited it at 10% profit, it hurts.

One of my close relatives followed this kind of approach. He has been an Investor/Trader in the markets for about 28 years. But his approach was to go for a win-loss ratio of 1:1. That is, exit winners at 10% profit and cut the loss at 10%. In investing, not getting the big profits is as risky as not cutting the downside.

His results from the 30-year journey have not been significantly better than my mom’s consistent 8% compounding for 35 years.

Verdict: Not worth doing. Avoid.

Investor 3 - The Index Investor

The return profile of Investor 3 is similar to that of an Index Investor. A crash of 40% once a decade. A Bear Market once in ~3 years.

Although there is a big fall once in 10 years, the markets have recovered quite quickly post such falls.

Let us evaluate the path of Investor 3.

Time Spent- Negligible. Select a low-cost Index fund and do regular SIPs. That’s it.

Stress Levels- Low. Just do regular SIPs and ignore everything else.

Return - Average Market Returns. Likely to beat FD over the long term. Long-term means at least 10 years.

Behavioural Difficulty - Moderate. One needs to understand that markets are volatile and they should not be perturbed by volatility. One should use Volatility to capture more units of the Index at lower levels. One should not time the Index. Some good behaviour and understanding is required.

Regret - You won’t regret doing a SIP in an Index Fund ever.

Verdict: For anyone just starting their investing journey, Index Investing is the way to go. It might just be the only thing you need to get exposure to stocks. No Trading. No Timing. This is enough to both survive and thrive. Should be a good part of your overall portfolio in the initial years.

Investor 4 & 5 - Enthusiastic New Participants

Investor 4 & Investor 5 have significantly underperformed even FDs. This type of Investor typically has unrealistic expectations from the market and is more focused on high returns rather than controlling risk. They indulge in regular buying and selling of stocks. They buy Options expecting a jackpot. They are not willing to invest time in learning and burn their hands very early. Once you lose significant capital early, it is difficult to get back on track. This might lead to taking even more unrealistic bets piling up even more losses. A vicious cycle you need to be aware of.

Let us evaluate the path of Investor 4 & Investor 5.

Time Spent - High

Stress Levels- Very High

Returns - Poor

Behavioural Difficulty - High

Regret - Very high. Lifelong sometimes.

Verdict: Not worth it when you are just beginning your stock market journey. Do not explore Short Term Trading or Regular buying/selling of Stocks. Do not indulge in speculative F&O trades. Use F&O only for hedging. It requires a deeper understanding and a strong behaviour to excel in Trading.

Investor 6 - The Seasoned Investor and Trader

By looking at the return profile of Investor 6, we can see that Investor 6 has not let the losses go beyond 10% in any year. Investor 6 has faced losses in 4 out of the 10 years. Yet, Investor 6 ended up winning. That is because Investor 6 picked up the big gains in multiple years. Investor 6 has been relentless in controlling risk and patient enough to reap the big rewards. A sign of a seasoned player.

Let us evaluate the path of Investor 6.

Time Spent - High. Need to spend quality time analyzing and preparing.

Stress Levels- Initially High. But, Stress reduces over time once you are at peace with the process and understand the game better.

Returns - Likely long-term outperformance but not guaranteed outperformance.

Behavioural Difficulty - High. Cutting losses is difficult. Staying patient to bag those big rewards is equally difficult. But it becomes second nature after a while.

Regret - Striving towards continuous minimisation of regret.

Although the path of Investor 6 seems to be the best in terms of returns, it compromises other parameters. It might not be easy for beginners to traverse this path without dedicating time to learn. It is good to get a mentor to get feedback on behavioural aspects. Even if you learn everything needed and develop good behaviour, it is not guaranteed to fetch you higher returns.

"I am not putting down the study of economics, business cycles, and even security analysis. But knowing them does not guarantee success, and if you haven't a clue about them, there may be hope for you yet." Adam Smith, The Money Game

"The most important thing in investments is not having a high IQ, thank God. I mean, the important thing is realism and discipline. And you don’t need to be extraordinarily bright to do well in investments if you are realistic and disciplined." Warren Buffett

Going in the path of Investor 6 might not be required for most of us to achieve our goals. Through a combination of Fixed Income Investing (Investor 1) and Index Investing (Investor 3), we are likely to achieve our goals and might even exceed our expectations.

Conclusion

You are likely to lose your capital/purchasing power if you take the path of Investor 2, Investor 4 or Investor 5.

If you are a beginner, it is good to take the path of Investor 1 and Investor 3. Focus on your work and build capital through your income instead of building capital through profits/capital gains. Develop skills and competence in a particular field. Learn everything related to Investing and Trading while doing this.

After doing the above for at least 10 years or after you have sufficient money to cover your lifelong expenses, you can take one of these 2 paths.

You might be passionate about your job/other areas more than the stock market. So you continue doing Fixed Income Investing and Index Investing.

You become more passionate about markets and want to pursue it full-time. You believe you are equipped with the right knowledge and behaviour to survive in the markets. That is when you need to take the path of Investor 6.

Hope I have been able to give some context on the paths you should take and avoid. I also believe this will help you set the right expectations and goals.

Now that you are aware of the different paths, we will do Goal Setting in the next post and then take it forward.