ZAGGLE PREPAID OCEAN SERVICES || Consistently Performing Stocks #58

What has led to the consistency?

Each week I analyze one company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.This week, Let’s explore the business & fundamentals of ZAGGLE PREPAID OCEAN SERVICES.

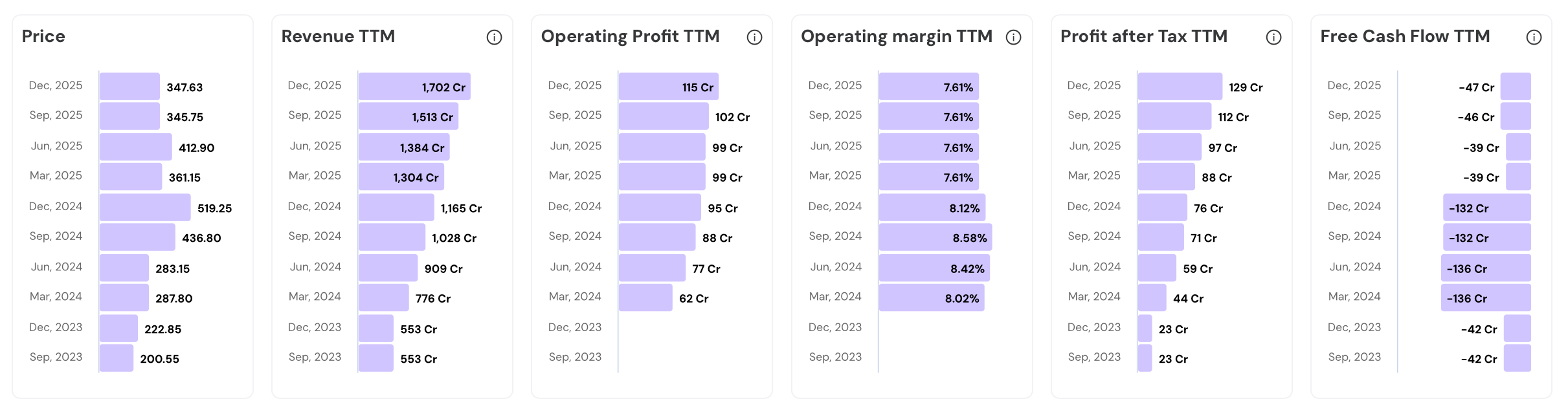

In the last 3 years…

- Stock price has grown 1.7x (from ₹200.55 to ₹347.63)

- Revenue TTM has grown 3.1x (from ₹553 Cr to ₹1,702 Cr)

- Operating Profit TTM has grown 1.9x (from ₹62 Cr to ₹115 Cr)

- PAT TTM has grown 5.6x (from ₹23 Cr to ₹129 Cr)

Take a look at the fundamentals chart below.Performance Chart || Last 3 Years

Their Road to Consistency

1. Overview and Business Model

Zaggle operates at the intersection of enterprise software and financial services. Founded in 2011 in Hyderabad by serial entrepreneur Dr. Raj Narayanam, it evolved from a prepaid card issuer to a full-stack corporate spend management platform. Revenue grew from ₹240 crore in FY21 to ₹1,303 crore in FY25, a 52% CAGR. Currently, it is serving about 3,455 corporate clients.

The B2B2C model onboards a corporate client and instantly activates their employees as platform users. One contract can unlock thousands of active end users. Structurally efficient by design.

Revenue comes from three streams:

Program fees at approximately 48%. Program fees are interchange income from banking partners, earned each time a Zaggle-powered card is swiped. Zaggle earns roughly 1.7-1.8% of spend value on an 80/20 split. More the transaction volumes, more the upside.

Propel platform redemptions at 49%. Propel platform revenue is earned when employees and channel partners redeem reward points for brand vouchers and products. Zaggle captures a 10-15% take rate on redemptions. Volumes and festivity drive this engine.

SaaS subscriptions at roughly 3%. SaaS fees are monthly per-user charges for modules like Save for employee tax benefits and Zoyer for accounts payable. Pricing has risen from ₹99 to ₹249 per month. Small in share, but high-margin business.

Zaggle has issued over 50 million prepaid cards cumulatively till date.

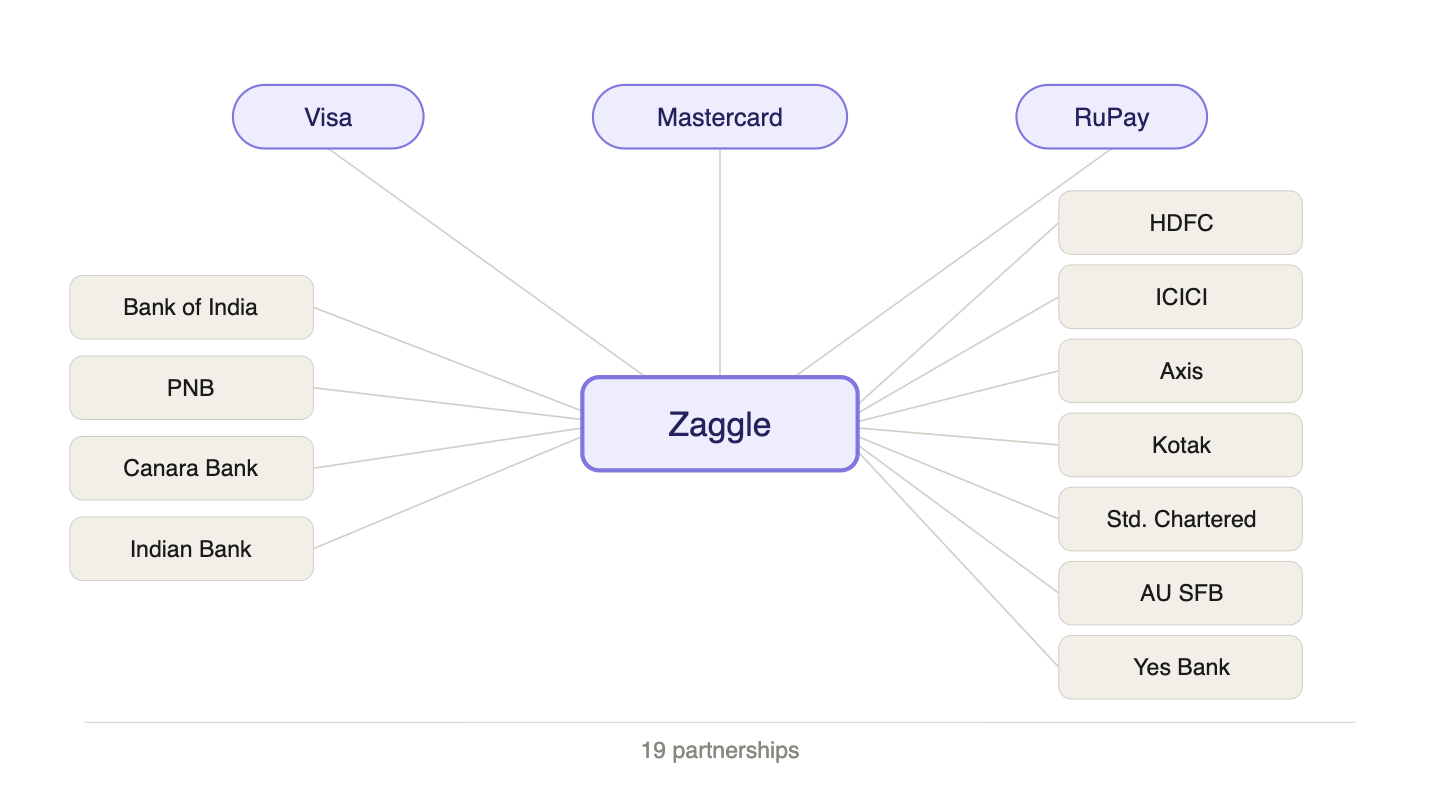

Zaggle maintains 19 banking partnerships alongside Visa, Mastercard, and RuPay tie-ups for card issuance. This infrastructure took over a decade to build.

CEO Avinash Godkhindi brings 15+ years across Citibank, Barclays, and ING Bank across 12 countries. Founder Dr. Narayanam previously built eYantra Industries to 4,500 clients in 45 countries at a 63% CAGR.

9M FY26 revenue of ₹1,260 crore nearly matched the entire FY25 revenue. PAT of ₹95 crore already exceeded FY25’s full-year profit of ₹87.5 crore. Growth is accelerating.

2. Recurring Software Revenue

Zaggle’s SaaS subscription business charges corporate clients monthly per-user fees for accessing expense management and accounts payable automation software. This segment is the smallest revenue contributor today but is the highest-margin anchor of the entire platform. It creates the workflow dependencies that feed every other revenue stream.

SaaS platform fees surged 754% year-on-year in the quarter ending December 2025. It kind of indicates corporate willingness to pay for financial workflow software.

Software fees hit a record ₹12 crore in Q3 FY26 alone, the highest ever for any single quarter.

Indian CFOs are now actively seeking better spend controls, and management explicitly cited this shift in the Q4 FY24 earnings call.

The Save platform manages employee flexible salary components and tax-exempt benefits under India’s evolving tax regime. It is now embedded in payroll processes at major corporates like Tata Steel and Toshiba.

Zoyer automates accounts payable with three-way PO, GRN, and invoice matching. CFOs use it for real-time spend visibility and vendor reconciliation.

BROME manages branch-level recurring expenses for distributed retail businesses. Clients like Blinkit and Physics Wallah deploy it across 850+ branches.

ZatiX provides AI-powered spend analytics as a premium upsell on top of core SaaS modules. Clients pay more for insights they did not have before.

TaxSpanner integration into Save creates a seamless tax filing journey for millions of existing users. This cross-sell deepens per-user value without any new client acquisition cost. Intelligent product bundling.

Per-user pricing increased from ₹99 to ₹249 per month, a 151% monetization increase from the same installed base. Zaggle is extracting more from what it already owns.

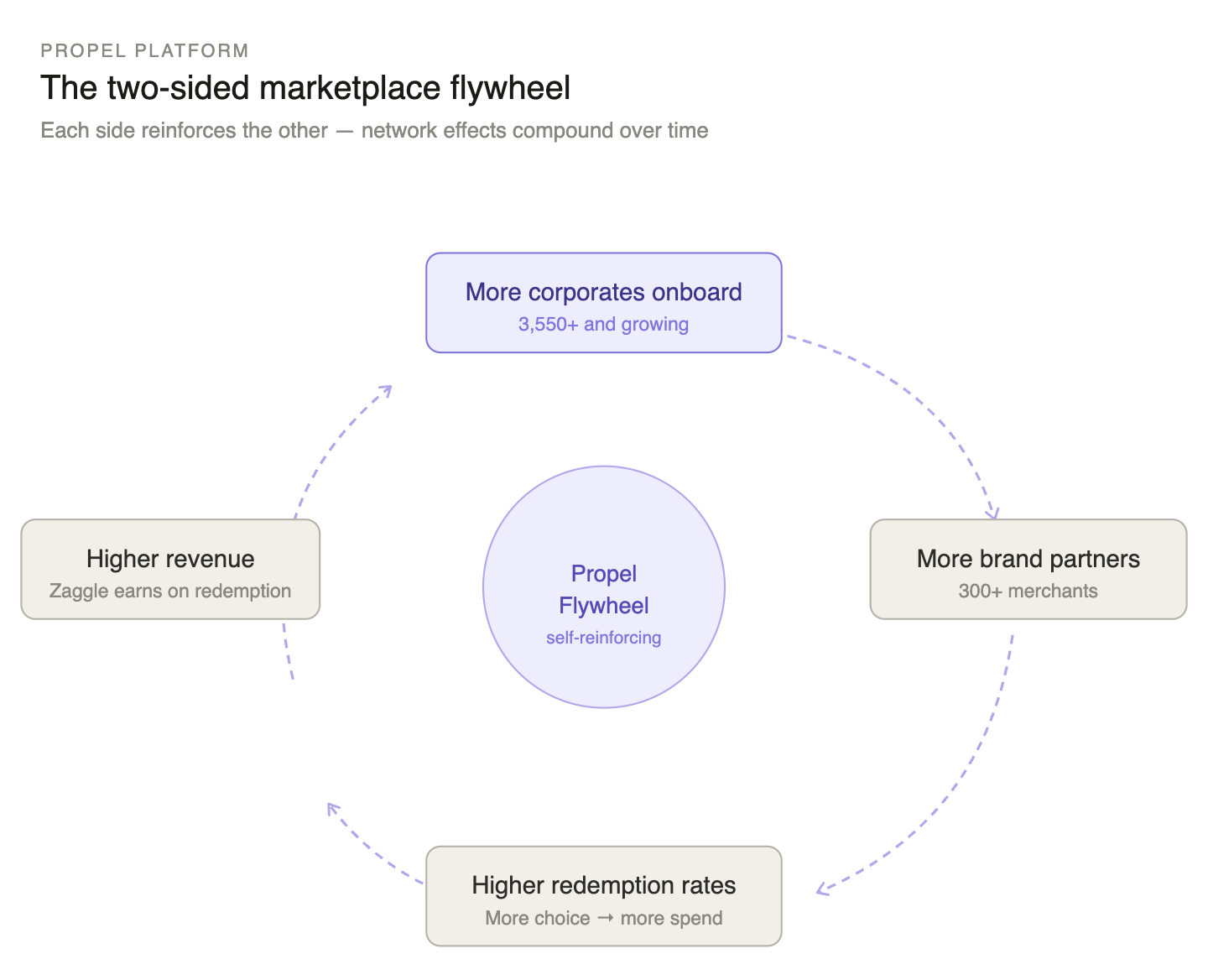

3. Propel Rewards Flywheel

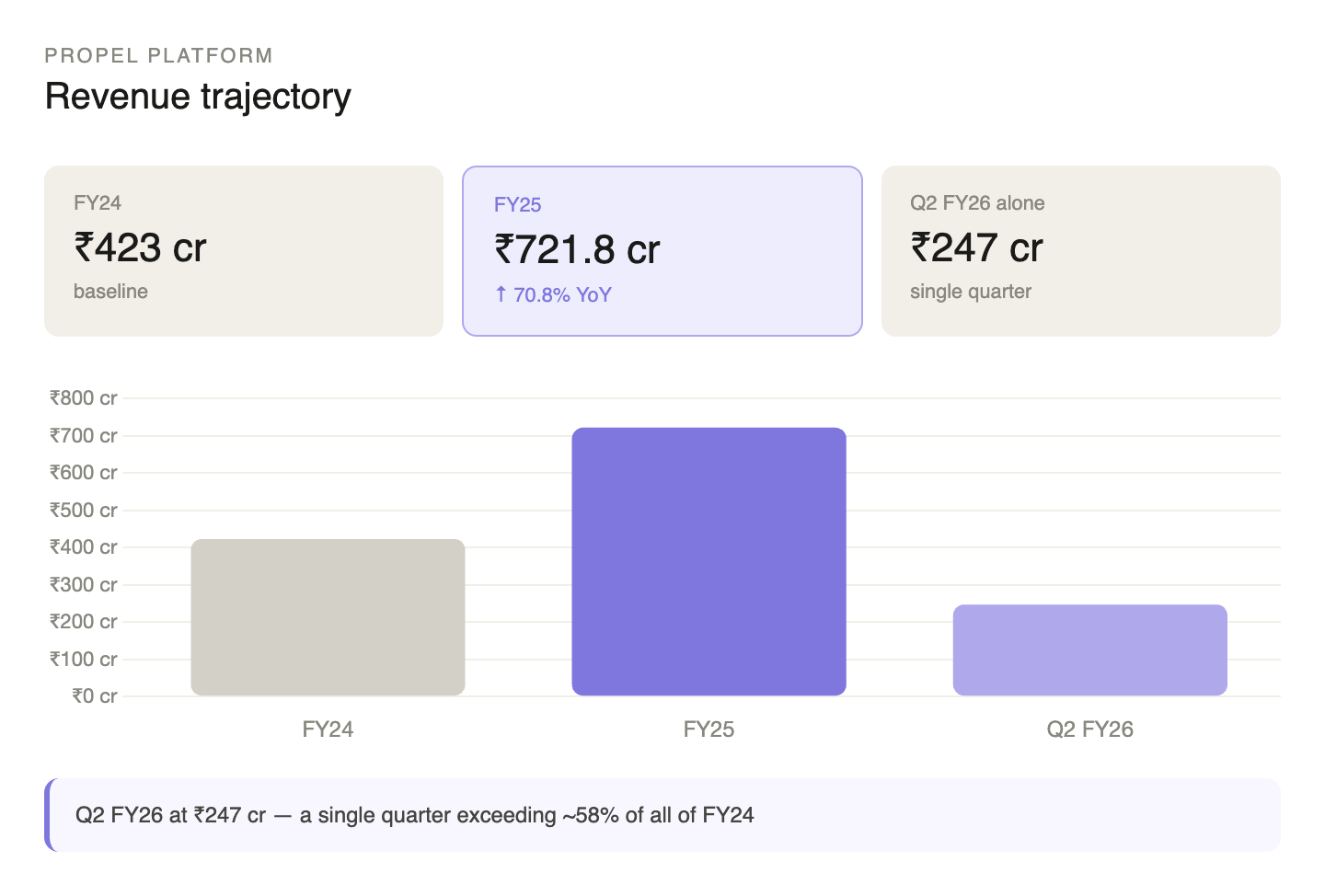

The Propel platform powers corporate gifting, employee recognition, and channel partner incentive programs. Revenue is earned when Propel Points issued to employees or dealers are redeemed for vouchers and products across 300+ brand partners. This is Zaggle’s largest revenue contributor and benefits from India’s formalizing incentive economy.

Propel platform revenue reached ₹721.8 crore in FY25, a 70.8% jump over FY24.

Q3 FY25 alone saw 87% growth in Propel revenue, driven by festive season redemptions around Diwali.

Over 3,550 corporates had onboarded their reward programs onto Propel as of late 2025. This creates a two-sided marketplace. Each new client makes the platform more attractive to merchants.

Zaggle aggregates thousands of merchants, enabling point redemptions across food, travel, electronics, and more. Greater choice increases redemption rates. Higher redemption rates translate directly into higher revenue for Zaggle.

Propel Points revenue stood at ₹247 crore in Q2 FY26 alone. It indicates that full-year contributions will substantially exceed FY25 levels.

Approximately 60% of Zaggle’s annual business falls in H2 due to festive and year-end reward cycles. This is a known and manageable cash flow pattern. Predictable seasonality is far less dangerous than erratic demand.

Zaggle provides a multilingual interface on Propel to serve blue-collar workers and retail channel partners.

Propel is also becoming a financial services entry point for gig workers through the new ZUGS offering.

4. Program Fee Scaling

Program fees are Zaggle’s most scalable revenue stream, earned from interchange income shared by banking partners on every card transaction. This revenue line grows directly with user spending volumes and does not require proportional cost increases.

Program fees reached ₹545.6 crore in FY25, growing 69.5% over ₹321.8 crore in FY24. Interchange income has compounded at an 18%+ CAGR since FY21.

Program fee revenue crossed ₹200 crore in a single quarter for the first time ever in Q3 FY26. Management expects this to become the new quarterly baseline.

Zaggle earns roughly 1.7-1.8% of spend value through an 80/20 revenue-sharing arrangement with partner banks. This is recurring, spend-indexed, and scales with the consumption habits of the user base.

Float income on prepaid card balances loaded by corporates but unspent by employees adds another layer to the positive economics. Other income including float grew from ₹0.3 crore in FY21 to ₹24.5 crore in FY25. Hidden but compounding.

Incentive costs currently represent 66-67% of program fees. Company Management has guided to reduce this toward approximately 50% over five years. If achieved, net margins on this segment improve materially without requiring any revenue growth.

The product mix is deliberately shifting toward commercial credit cards, which carry higher interchange rates than standard prepaid cards. HDFC Bank and AU Small Finance Bank credit card partnerships are serving this upgrade.

Rio Money, acquired for ₹22 crore, added UPI-linked consumer credit capabilities. Zaggle plans to issue one million credit cards over the next five years. Credit card interchange is meaningfully higher than prepaid.

5. Banking Network Depth

Zaggle’s 19 banking and card network partnerships form a structural moat that would take any new competitor time to build. Banks provide the regulatory and underwriting infrastructure. Zaggle handles software integration, customer acquisition, and user experience.

Zaggle works with private banks including HDFC Bank, ICICI Bank, Axis Bank, and Kotak Mahindra Bank, alongside public sector banks including Bank of India, PNB, Canara Bank, and Indian Bank.

A 7-year growth agreement with Visa Worldwide was signed in Dec 2025 for co-branded domestic prepaid cards.

A 5-year referral partnership with Mastercard covers credit card distribution. A separate 7-year Asia-Pacific Mastercard agreement handles domestic prepaid cards. Both global networks are commercially committed to Zaggle.

Standard Chartered Bank signed a 5-year referral agreement in August 2025 to offer Zaggle software and prepaid cards to Standard Chartered’s entire corporate client base.

The HDFC Bank credit card partnership, formalized in Q3 FY25, bundles Zaggle software with payment instruments for corporates.

AU Small Finance Bank launched co-branded retail credit cards with Zaggle in September 2025, including an AI-powered spending recommendation engine.

The Yes Bank partnership enables a Rio RuPay credit card accessible via QR codes on the UPI interface.

Banking partners carry regulatory, underwriting, and balance sheet risk. Zaggle handles software, client acquisition, and user experience. There is clear dependency on each other.

6. Inorganic Growth Engine

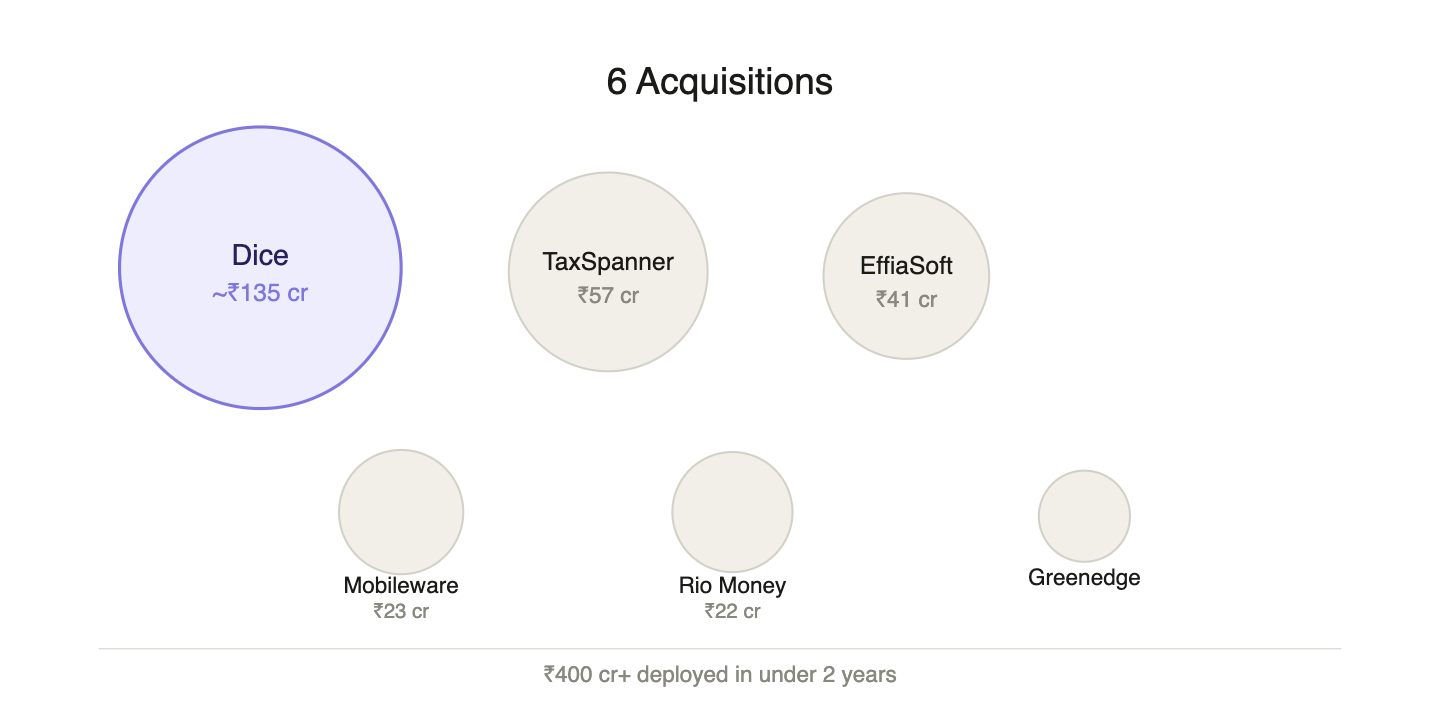

Zaggle has deployed IPO and QIP capital to build new capabilities through 6 targeted acquisitions in under 2 years, covering tax filing, UPI infrastructure, enterprise automation, and rewards. Each acquisition adds a monetization layer to the existing corporate client base without requiring proportional new client acquisition effort.

TaxSpanner was acquired for ₹57 crore in September 2024 at a 98.3% stake, adding tax filing and financial wellness to the platform. Integrated into Save, it turns expense management into a complete tax compliance journey.

Mobileware Technologies was acquired at a 38.34% stake for ₹23 crore, bringing NPCI-certified UPI and IMPS infrastructure. Mobileware’s revenue nearly doubled to ₹34 crore in FY25. It has been re-branded as 86400.

Dice Enterprises was acquired for approximately ₹123-150 crore in June 2025, strengthening enterprise automation in travel, procurement, and accounts payable. It immediately extended Zoyer’s capabilities in a meaningful way.

Rio Money (Rivpe Technology) was acquired for ₹22 crore in early 2025, giving Zaggle entry into UPI-linked consumer credit.

Greenedge Enterprises added experience-based premium rewards including golf travel to the Propel portfolio.

EffiaSoft, a Hyderabad-based billing software provider, was acquired at a 51% controlling stake for ₹41 crore. Billing software sits at the natural intersection of vendor management and spend control workflows.

Total acquisition spending exceeds ₹400 crore across six deals, funded primarily by QIP proceeds of ₹595 crore. Each deal has a strategic rationale. Capital deployment has been fast.

7. Platform Stickiness

Zaggle’s deepest competitive advantage comes from embedding its software into corporate payroll, accounting, and ERP systems. This creates switching costs that far outlast contract periods. The deeper the integration, the harder it becomes for any client to replace, keeping churn consistently below 1.5% year after year.

Customer churn has remained below 1.5% in FY25. Enterprise SaaS typically targets under 5%. Below 1.5% signals a product embedded in mission-critical workflows.

Zaggle’s ZIG integration gateway provides API connections to SAP, Oracle, Tally, and major HRMS platforms. Replacing this would require a full IT migration project. Sticky business.

Approximately 70% of total revenue comes from clients using multiple platform modules. Multi-module clients spend more, churn less, and require no incremental sales effort.

Customer acquisition cost stays below 5% of revenue because individual users are activated through the corporate contract, not acquired independently.

No listed peer in India offers the full stack. Happay was sold to MakeMyTrip. Open Financial Technologies posted ₹58 crore in FY25 revenue against cumulative losses of ₹1,831 crore. SAP Concur lacks embedded payment rails. Zaggle is filling the gap.

Existing Save module clients are routinely cross-sold into ZatiX analytics, Zoyer AP automation, and TaxSpanner tax filing. Each additional module deepens the integration.

The Smart Employee Purchase Program lets employees buy phones and electronics through tax-efficient leasing on the Zaggle app. This extends daily utility beyond expense claims and reimbursements.

The Propel network creates a reinforcing loop. More merchants make reward points more valuable. More valuable points attract more employees. More employees attract more corporates. The network grows its own value.

Recent marquee client additions include Google, Blue Star, HDFC Ergo, Apollo Health, Pernod Ricard India, and Chennai Super Kings across FY25 and FY26.

8. AI Operating Leverage

Zaggle has embedded artificial intelligence across product development, customer support, fraud detection, and vendor reconciliation. The impact is already visible in the financials. In FY25, net profit grew 99% on 68% revenue growth. Cost structures are not scaling proportionally with the top line. That asymmetry is called Operating leverage.

AI reduced product development cycles from over 75 days to under 30 days, a 60% improvement in time-to-market. In fintech where timing determines adoption, speed is a competitive weapon. Faster launches mean earlier revenue recognition.

The AI chatbot RazBot now deflects 60% of customer service tickets, with a stated target of 99% deflection. Every percentage point saved is support headcount that does not need to be added.

Agentic AI workflows independently execute vendor reconciliations, compliance monitoring, and spend approval processes. These were once labor-intensive manual tasks. Automating them directly reduces cost-per-transaction without compromising accuracy.

Adjusted EBITDA crossed ₹50 crore in a single quarter for the first time in Q3 FY26. Management attributed this milestone explicitly to improved operational agility from AI deployment.

ZatiX uses machine learning for expense categorization, fraud detection, and policy enforcement. These features are sold as premium analytics to CFOs.

Model Context Protocol (MCP) adoption enables standardized data interactions for faster client onboarding.

Machine learning models actively flag unauthorized spends and detect mule account activity. Fraud prevention here is both a product feature and a regulatory compliance tool.

9. Global Expansion

Zaggle is extending its corporate spend platform beyond India into international payments, the UAE market, GIFT City cross-border services, and government contracts. These are early-stage moves, but each is backed by a regulatory filing, a signed agreement, or specific capital allocation.

The board approved Zaggle Payments IFSC Limited in GIFT City in February 2026 for cross-border payment services targeting Indian corporates with international operations. The regulatory foundation is already laid.

The UAE entity is in its final formation stages, with Abu Dhabi identified as the primary MENA base. Direct engagement with UAE government stakeholders, including the Minister of AI, has already happened.

An MOU with US-based Mesh Payments was signed to serve Indian corporates managing global business expenses.

The Zaggle GlobalPay Forex Card automates cross-border expense reporting for international business travelers. For Indian multinationals with staff traveling regularly, this addresses a genuine pain point.

Zaggle secured a 5-year contract with GIFT City (GIFTCL) for a co-branded citizen card and visitor management system. Government accounts for approximately 8% of India’s spend management market.

The UAE base is positioned as a springboard into Africa and Europe over the longer term. The $1 billion annual revenue target within the next 5-7 years explicitly includes international market contributions.

10. Risks and Red Flags

Zaggle operates in a regulated, fast-moving environment where business model risks are real and require scrutiny.

The RBI’s 2025 Payment Aggregator Directions reclassified platforms like Zaggle as financial infrastructure. Compliance burdens for anti-money laundering and fraud monitoring have materially increased. The regulatory weight on this business is meaningfully heavier than it was a couple of years ago.

Prepaid card interchange rates can be capped by regulatory action. The 2020 zero-MDR policy on UPI and RuPay debit cards demonstrated how quickly a revenue stream can compress. Approximately half of Zaggle’s current revenue is interchange-dependent. This is a structural risk.

SaaS fees represent only about 3% of FY25 revenue. Despite the 754% quarterly growth rate, absolute size remains small. Until software revenue grows substantially in share, Zaggle will still be classified as a transaction facilitator and not a software business.

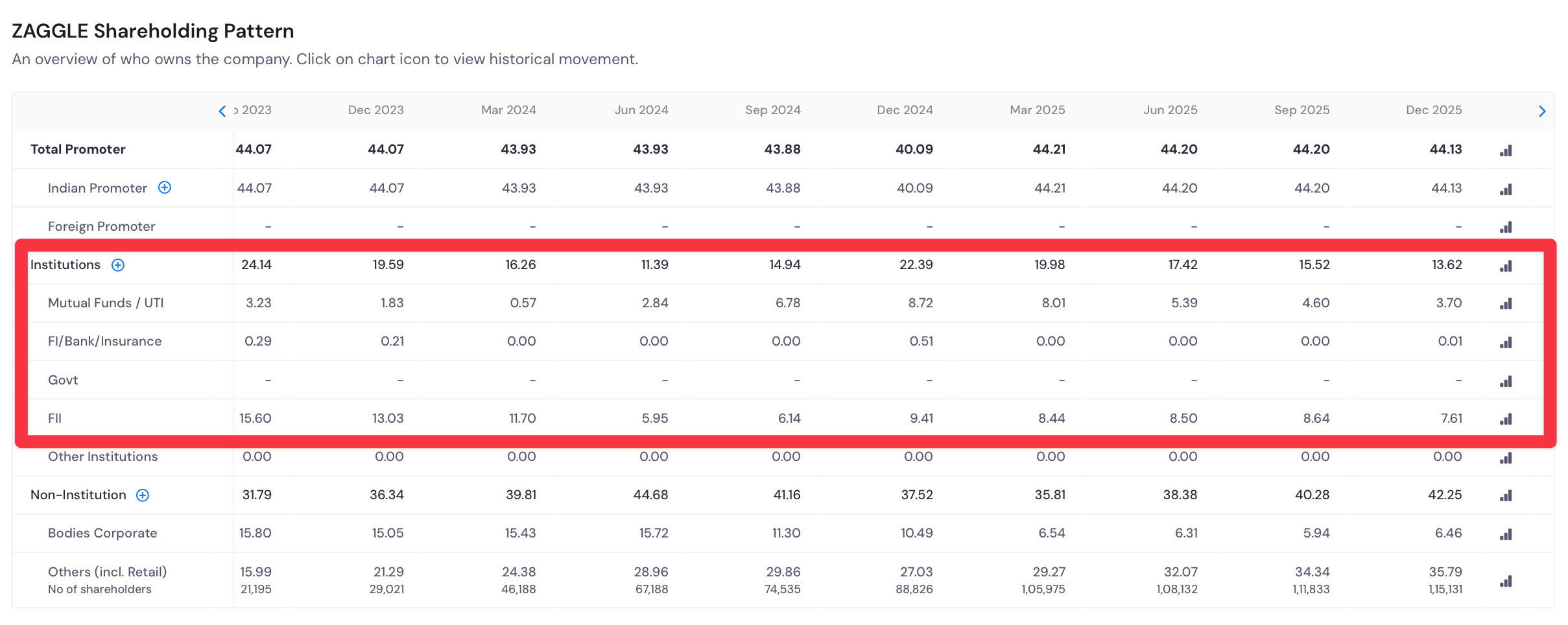

Mutual fund holdings declined from 8.72% in December 2024 to 3.70% in December 2025, a sustained three-quarter institutional selloff. FII holdings also fell from 15% in 2023 to 7.61% in 2025.

Operating cash flow turned positive only in FY25 at a modest ₹20 crore on ₹1,303 crore revenue. Free cash flow generation at scale is still unproven. The ₹653 crore cash buffer provides time, but it is finite.

Point redemption costs remain at approximately 49% of total revenues and rose further in late 2025. If incentive intensity does not normalize toward management’s stated 50% of program fees target, margin expansion stalls regardless of top-line growth.

Zaggle’s revenue depends significantly on Visa, Mastercard, and its top banking partners. A global policy shift from either card network, or deterioration in any major bank partnership, could disrupt card issuance.

Large banks like HDFC Bank and Kotak could theoretically build their own corporate expense management platforms and bypass intermediaries like Zaggle.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

https://earningsunwrapped.substack.com/p/inside-zaggle-the-quiet-fintech-that?utm_source=share&utm_medium=android&r=rer2b

Wrote about zaggle a couple of months back, very unique business from a spend control perspective. Business is thriving but the cash flow issues which management expects to continue for FY'26 as well has beaten it's share value down heavily. At the same time, feel share has reached its bottom . Great one to track from hereon.