Transport Corporation of India || Consistently Performing Stocks #57

What has led to the consistency?

Each week I analyze one company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.This week, Let’s explore the business & fundamentals of Transport Corporation of India (TCI)

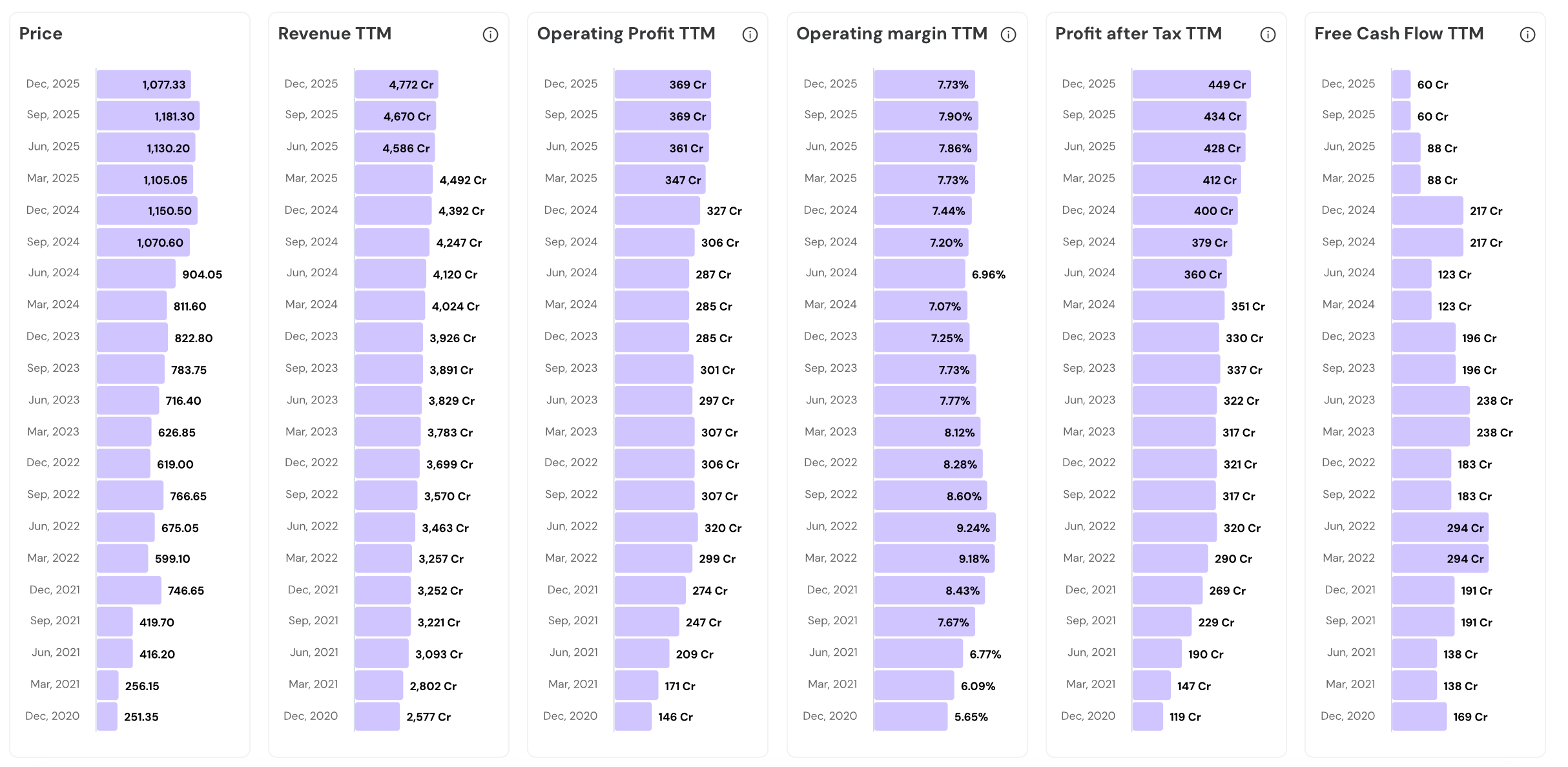

In the last 5 years…

- Stock price has grown 4.3x (from ₹251.35 to ₹1,077.33)

- Revenue has grown 1.9x (from ₹2,577 Cr to ₹4,772 Cr)

- Operating Profit has grown 2.5x (from ₹146 Cr to ₹369 Cr)

- PAT has grown 3.8x (from ₹119 Cr to ₹449 Cr)

Take a look at the fundamental charts below.Performance Chart || Last 5 Years

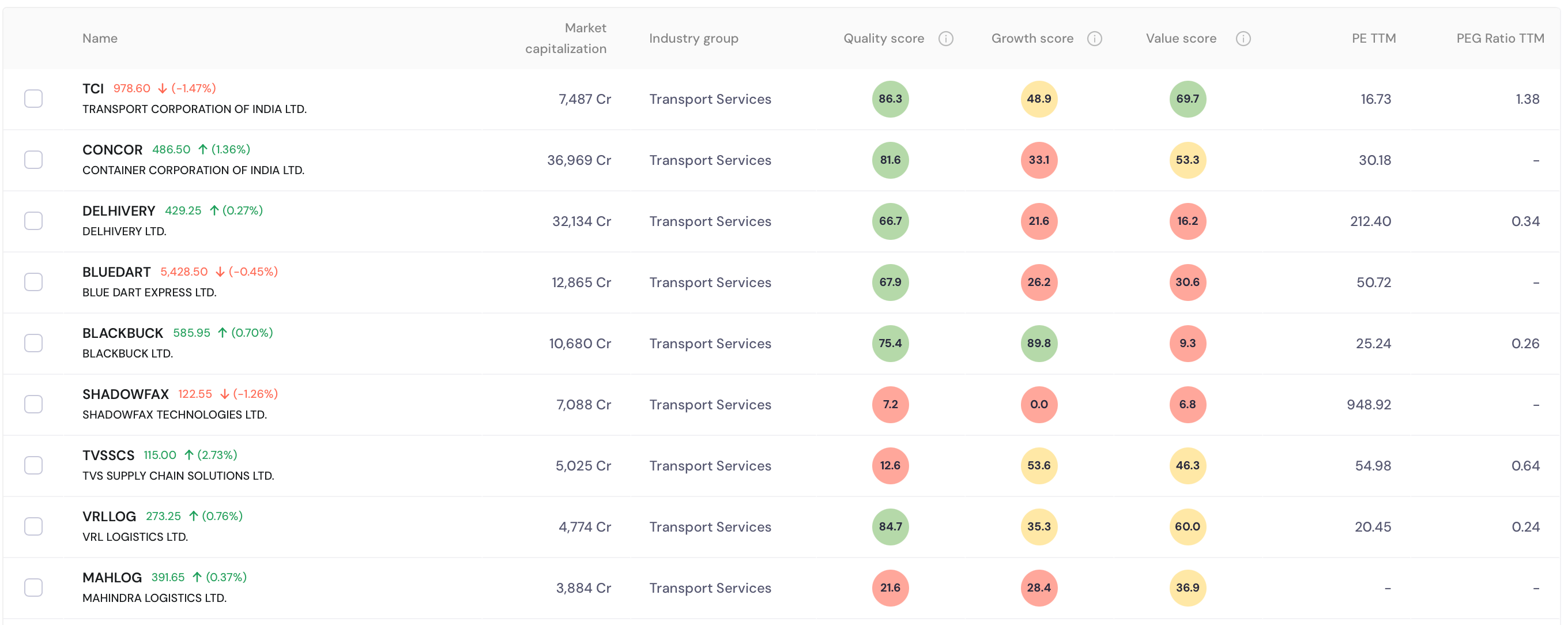

Peer Comparison

Their Road to Consistency

1. Overview & Business Model

Transport Corporation of India (TCI) is India’s only truly integrated multimodal logistics company, operating across road, rail, sea, and warehousing since 1958.

Founded by Prabhu Dayal Agarwal with a single truck in Kolkata, TCI today moves approximately 2.5% of India’s GDP by value annually.

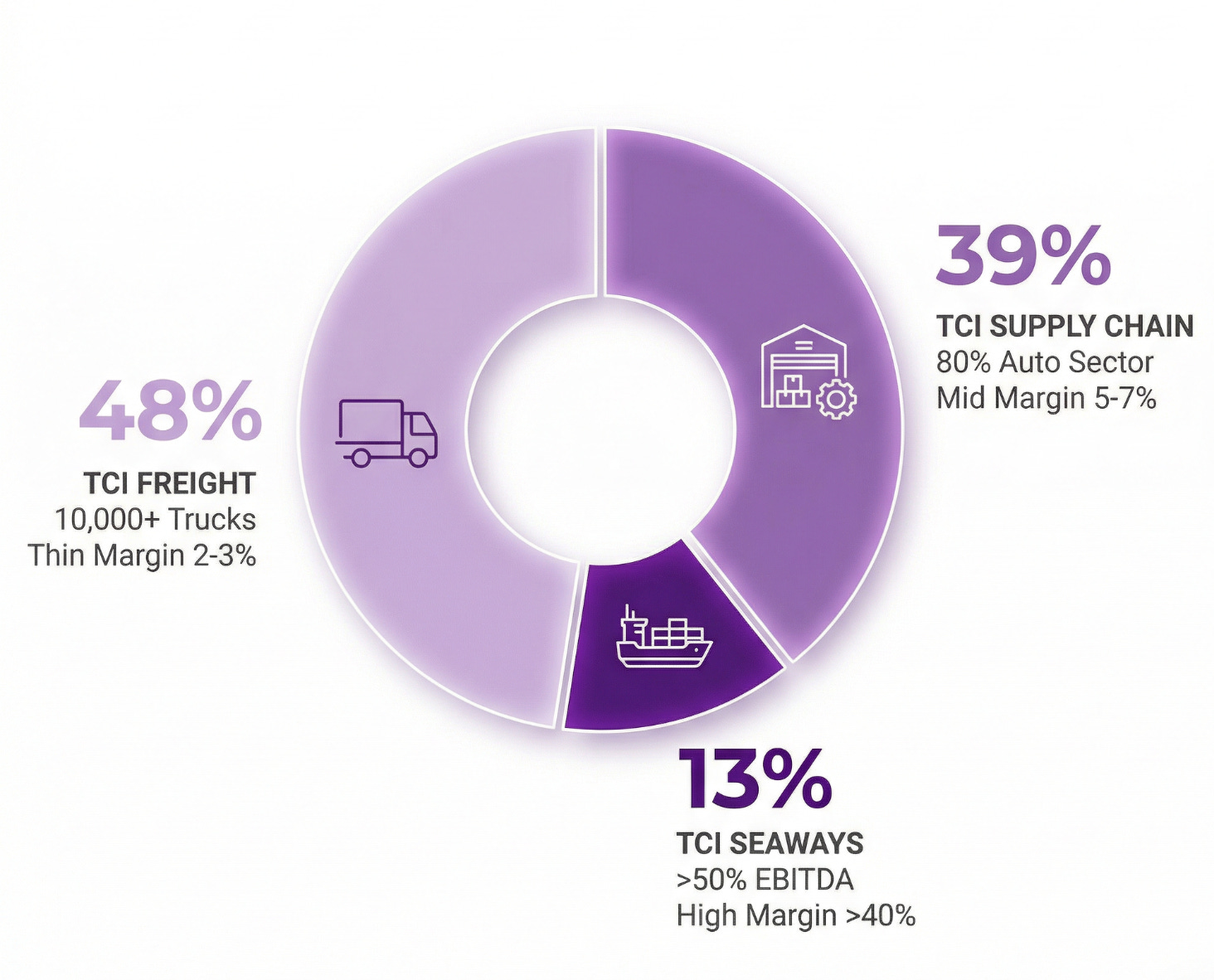

TCI operates through three core revenue segments.

TCI Freight contributes 48% of FY25 revenue, operating 10,000+ trucks across 25 hubs and 700+ branches for Full Truck Load, Less-than-Truck Load, and project logistics. Freight earns thin EBIT margins of 2-3%

TCI Supply Chain Solutions contributes 39%, providing end-to-end 3PL and 4PL services across 16+ million sq ft of warehousing. The automotive sector accounts for roughly 80% of SCS revenue. Supply Chain Solutions has EBIT margins of 5-7%.

TCI Seaways, at 13% of revenue, operates six coastal ships with 77,975 DWT capacity and serves 7 of India’s 13 major ports. Seaways generates over 50% of consolidated EBITDA despite being just 13% of revenue, with margins consistently above 40%.

Three strategic joint ventures add depth to the group.

Transystem Logistics International (51% stake, JV with Mitsui) generated ₹1,184 crore in FY25, serving Toyota Kirloskar with just-in-time automotive logistics.

TCI-CONCOR Multimodal Solutions (49% stake with Container Corporation of India) generated ₹456 crore in FY25, combining rail and road infrastructure.

TCI Cold Chain Solutions (80% stake with Mitsui) focuses on temperature-controlled logistics. Combined JV profit contribution to TCI grew 3x from FY20 to FY25.

2. Seaways Profit Engine

TCI Seaways is the crown jewel of the TCI portfolio, contributing over half of consolidated EBITDA from just 13% of revenue. Fully depreciated ships, structural cost advantages over road transport, and rising government support for coastal shipping create a moat that road-focused competitors cannot replicate easily. Two new vessels on order will expand capacity by 25%, adding to earnings growth from mid-2026 onwards.

All 6 existing ships are fully depreciated with zero interest costs. This means virtually every rupee earned at the EBITDA level flows directly to profit. In Q3 FY26, Seaways posted a 40.6% operating margin. Extraordinary capital efficiency.

Coastal shipping costs ₹1.19 per tonne-km versus ₹2.28 for highways. That is a 40-50% cost advantage for every client who switches from trucks to ships.

The ROCE for Seaways is around 50%. Building such a return profile on a fully depreciated asset base is intelligent capital allocation.

Seaways posted 8.7% revenue growth in Q3 FY26, reaching ₹168 crore. Margins expanded 787 basis points year on year in the same quarter. Bunker fuel prices falling 17% over nine months was a tailwind.

The company ordered two new container vessels from Nakanishi Shipbuilding in Japan, each 7,300 DWT. Total contract value is approximately USD 38.8 million. Delivery is expected by mid-to-late 2026, adding 25% to fleet capacity.

India’s coastal shipping carries just 6% of national freight versus 60-65% via roads. The government’s Sagarmala program has earmarked ₹5.79 lakh crore across 839 projects to reverse this imbalance. TCI is well positioned to ride this policy wave.

Coastal shipping emits 70% less CO2 than road transport. As large multinationals face scope 3 emission mandates, the green case for coastal shipping strengthens commercially. TCI’s Seaways division reported saving approximately 1.5 lakh tonnes of carbon emissions recently.

Two ships are scheduled for mandatory dry-docking in FY26. This temporarily constrains active fleet capacity and is the primary near-term headwind for the segment. But the margin buffer is so high that they can manage it.

Routes connect Mundra, Kandla, Mangalore, Kochi, Tuticorin, Chennai, Vizag, and the Andaman Islands. TCI Seaways runs critical supply lines connecting India’s two coasts and remote island territories.

3. LTL Freight Pivot

The management deliberately pivoted from Full Truck Load to Less-than-Truck Load business, targeting higher margins and a stickier customer base. This shift is structurally defensive. LTL volumes hold up better in downturns than industrial FTL volumes, making the freight division a more resilient earnings contributor over time.

LTL margins run at roughly 20% versus 10% for FTL freight. The company intentionally grew LTL’s share from 33% in FY20 to 38% in FY25. Every percentage point gained directly improves the divisional margin structure.

By Q3 FY26, LTL represented 37% of freight revenue. Management targets 42% by the end of FY26. Achieving this will likely expand divisional EBIT margins.

TCI Freight generated ₹595 crore in Q3 FY26, up a modest 2.6% year on year. Broader industrial and capital goods demand was soft in 2025. Despite macro headwinds, the LTL mix improvement kept margins from collapsing entirely.

Managing LTL cargo requires 25 strategically located sorting hubs across India. These hubs consolidate small parcels from multiple customers into efficient full truckloads for long-haul movement. Building this hub network took years.

The company added 40 new branches in FY25 and targeted 50 more in FY26. Denser branch coverage directly feeds LTL volumes by capturing smaller customers closer to their locations.

Premium value-added services including specialized packaging were integrated into the LTL offering. This repositions TCI from bulk carrier to solutions provider for electronics and consumer goods. Higher-value cargo commands higher yields than commodity freight.

EBIT margins in the freight division dipped to 1.9% in Q3 FY26. This is the current pressure point. Management believes margins have bottomed and expects roughly 100 basis points of recovery ahead. The LTL pivot is the primary lever driving this recovery.

4. Supply Chain Scaling

TCI Supply Chain Solutions is the fastest-growing division and is expected to overtake Freight as the largest segment by FY26-27. The business model is built on long-term contracts. Deep operational integration into client factories creates switching costs that insulate revenue far better than transactional logistics relationships. The automotive, FMCG, and quick-commerce verticals are all expanding simultaneously.

SCS generated ₹558 crore in Q3 FY26, growing at an impressive 25.3% year on year.

The division manages over 16 million sq ft of warehousing space across India. Automotive accounts for roughly 80% of SCS revenue. But FMCG, consumer durables, quick-commerce, healthcare, and renewables are all growing in share.

TCI opened a massive 3 lakh sq ft warehouse in Kolkata in September 2025. Located in CGTA Nagar on 10.5 acres, the facility features laser-screed flooring and robotics-compatible infrastructure. Clearly built for e-commerce and quick-commerce scale.

Managing in-plant logistics for automotive factories means controlling just-in-time parts delivery to assembly lines.

Finished vehicle distribution from factory yards to dealer networks is another specialized service. It requires customized rolling stock and real-time demand forecasting. TCI handles this for multiple automotive OEMs across India.

The division operating margin contracted to 5.2% in Q3 FY26 due to upfront investment in new assets. This is a deliberate margin-for-growth trade-off. Management is seeding capacity ahead of contract signings.

Quick-commerce contracts are accelerating SCS growth meaningfully. The explosion of 10-minute delivery platforms requires dense, sophisticated urban warehousing that only a network like TCI’s can provide.

SCS revenue has grown at approximately 15% CAGR over five years. The division is now approaching ₹2,000 crore annually. When it crosses that mark, it will likely also cross Freight division in revenue size.

5. Rail Multimodal Expansion

TCI’s rail logistics capability is genuinely differentiated. TCI operates specialized private freight trains in partnership with Indian Railways and CONCOR. The double-decker SUV rail rake, launched in Feb 2025, is a hard-to-replicate innovation that captures the specific logistics problem created by India’s shift toward larger passenger vehicles.

In February 2025, TCI launched the ACT1 model double-decker rail rake. The configuration uses 33 specially designed tall wagons. A single trip can transport up to 264 large SUVs, more than double standard wagon capacity.

The first commercial run moved Kia vehicles from Penukonda in Andhra Pradesh to Farukh Nagar in Haryana. This was India’s first dedicated SUV-only double-decker freight train. Kia’s willingness to partner on launch signals real operational confidence in TCI’s execution.

During 9M FY26, TCI operated 2,133 rail rakes, up from 1,783 in the same period last year. A 20% increase in rail volume in one year. The physical scale of rail operations is building rapidly.

TCI manages 67 dedicated rail yards across India. These yards are critical transfer points where containers move between trains and trucks without delays. Operating own yards rather than relying on third parties gives TCI scheduling control.

The TCI-CONCOR JV generated ₹455 crore in FY25, growing 32% year on year. In 9M FY26, it reached ₹396 crore, growing 21.1%. This JV is the direct commercial beneficiary of the Western Dedicated Freight Corridor’s near-completion.

The Western DFC is 96.4% complete, while the Eastern DFC is fully operational. DFCs have doubled freight speeds to 40-60 km/h and already handle 13.4% of Indian railway freight on just 4% of the network.

Two additional double-decker SUV rail rakes have been ordered for delivery by late 2026. The expansion order signals strong demand from automotive clients who want to scale this mode.

Rail transport emits dramatically less carbon than trucks. TCI’s 2,133 rakes in 9M FY26 saved approximately 1.6 lakh tonnes of carbon dioxide. For global automotive clients with scope 3 emission targets, this green credential influences contract decisions.

6. Cold Chain Opportunity

India’s cold chain logistics market is 80% unorganized, making it one of the highest-opportunity segments in the entire logistics landscape. TCI entered through a joint venture with Mitsui. It applies Japanese operational discipline to an Indian market starved of reliable temperature-controlled infrastructure.

TCI Cold Chain Solutions is a joint venture with Mitsui holding a 20% stake. Japanese cold chain expertise combined with TCI’s distribution network creates a formidable pairing. In 9M FY26, the entity generated ₹79 crore, growing 17.1% year on year.

In December 2025, TCI launched a 1.5 lakh sq ft temperature-controlled facility in Gurugram.The location sits between the KMP and Dwarka Expressways, giving unrestricted 24-hour heavy truck access.

The Gurugram facility offers frozen, chilled, and ambient temperature zones. This multi-temperature design attracts clients across pharmaceuticals, dairy, meat, and quick-commerce grocery simultaneously. One facility serves multiple high-margin sectors.

The warehouse uses SCADA-based electronic monitoring to maintain exact temperatures. Zero temperature deviation is non-negotiable for vaccines and biological products.

The facility operates on a pay-as-you-use billing model. Seasonal businesses can scale up or down without rigid leases. For FMCG clients managing festive season inventory spikes, this flexibility is commercially valuable.

Over 100 refrigerated trucks were deployed recently to maintain unbroken last-mile cold chains. Door-to-door cold chain integrity is the hardest part to execute. TCI’s decision to own reefer trucks rather than outsource this leg eliminates the weakest link in the chain.

The Gurugram facility features a 500 kilowatt rooftop solar installation. Refrigeration is enormously electricity-intensive. On-site solar directly reduces operating costs.

India is the world’s largest milk producer and second-largest fruit and vegetable producer. Post-harvest losses exceed 40% largely due to cold chain gaps. Cold chain will grow for decades regardless of short-term consumption trends.

7. Strategic Joint Ventures

TCI did not build every capability from scratch. It formed joint ventures that provided instant access to captive clients, specialized technology, and shared capital risk. The Mitsui partnership delivers Japanese automotive demand. The CONCOR partnership delivers rail infrastructure access. Together, these JVs have tripled their profit contribution to TCI from FY20 to FY25, from ₹277 crore to ₹896 crore.

Transystem Logistics International celebrated 25 years of operations in FY25. Built to serve Toyota Kirloskar Motors, it delivers just-in-time parts to vehicle assembly lines with zero tolerance for error.

Transystem generated ₹1,183 crore in FY25, growing 17% year on year. In 9M FY26, it added ₹974 crore, growing 11.3%. Japanese OEM demand in India is stable and long-duration. This is the most predictable revenue stream in the TCI group.

TCI-CONCOR Multimodal Solutions operates on an asset-light model. It combines CONCOR’s rail infrastructure with TCI’s first-mile and last-mile road network. Clients get seamless door-to-door service. Neither partner alone could offer this. The JV creates genuine capability multiplication.

All three JVs share capital expenditure with highly capitalized partners. TCI does not fund ships, rail infrastructure, or cold chain equipment alone. The financial burden splits across Mitsui’s balance sheet and CONCOR’s infrastructure.

Deep system integration with Japanese automakers and Indian Railways creates exit barriers for clients.

8. Technology and Efficiency

TCI invested in digital infrastructure long before it became fashionable for logistics companies to talk about it. The Logistics Control Tower, AI-enabled sorting hubs, and SCADA-based monitoring systems are now operational, not aspirational. These tools reduce costs, accelerate delivery speeds, and give enterprise clients the data visibility they require before signing multi-year contracts.

TCI’s Logistics Control Tower monitors 12,000+ trucks simultaneously across India using GPS, FASTag data, and driver mobile signals. Dynamic alerts notify teams instantly when a truck deviates from its route. Intervention speed prevents delays before clients even notice them.

The control tower integrates with the government’s Unified Logistics Interface Platform. ULIP connects 30+ digital systems with 160+ crore digital transactions. TCI’s integration reduces paperwork delays at state borders and highway checkpoints.

AI-enabled cross-belt mechanical sorters were installed at major hubs in Pune and Taj Nagar. The Pune automated sorting center alone cut physical turnaround time by 40%. Faster sorting means faster truck departures and better delivery commitments to clients.

AI-driven predictive analytics now forecast complex demand patterns for network planning. Bot-based customer service operations were also introduced to reduce response times.

RFID technology and custom mobile applications now power rapid yard audits. Every vehicle can be located within minutes. Previously, yard searches wasted hours of productive time.

The company built the Transportation Emissions Measurement Tool in partnership with IIM Bangalore. It is India’s first ISO 14083 certified emissions calculation platform. Enterprise clients can now accurately measure and report their logistics carbon footprint.

Digitizing operations directly protected thin margins when diesel prices fluctuated. Route optimization and reduced truck idle time cut unnecessary fuel consumption. In a business where EBIT margins in freight run at 1-3%, fuel efficiency is critical.

9. India Logistics Tailwinds

TCI operates in one of India’s most powerful structural growth stories. The organized logistics segment is growing at 12% CAGR, significantly faster than the 8-10% overall market growth. Regulatory formalization, infrastructure investment, and policy support are systematically eliminating the advantages of informal players.

Only 10-15% of India’s ₹230-320 billion logistics market is organized today. The remaining 85-90% is controlled by smaller fleet operators owning fewer than 5-10 trucks each. As compliance costs rise, these players face consolidation or exit.

E-way bills and mandatory e-invoicing with a ₹5 crore threshold are forcing unorganized players into compliance or forcing them out of the market entirely. Each compliance tightening enlarges TCI’s addressable market.

The National Logistics Policy targets reducing logistics costs from 13-14% of GDP to 8% by 2030. India has climbed from 44th to 38th on the World Bank Logistics Performance Index..

Cold chain logistics represents a $12.8 billion market growing at nearly 10% CAGR. India’s massive agricultural output and rapidly evolving pharmaceutical sector drive this. With 80% of cold chain currently unorganized, the opportunity for disciplined operators is multi-decade in scale.

The government’s Maritime Amrit Kaal Vision 2047 targets expanding port capacity from 2,700 MTPA to 10,000 MTPA. Coastal shipping cargo has already grown 118% over the past decade. Government policy is directly expanding the market that TCI Seaways serves.

TCI has already built a presence in Nepal, Bangladesh, Singapore, and the Middle East. As India’s trade volumes grow under new free trade agreements, cross-border freight becomes larger.

10. Risks and Red Flags

TCI’s core operations are fundamentally sound, but several external and internal vulnerabilities exist.

TCI Finance Limited, a separate NBFC within the same promoter group, reported a 91% drop in income in Q2 FY26. It posted consecutive net losses. A catastrophic default at TCI Finance could create negative group sentiment. TCI Finance is a legally separate entity with no operational connection to the logistics business.

Freight division EBIT margins dipped to 1.9% in Q3 FY26. Intense competition from MSME truckers and weak SME sector demand are structural pressures. Management believes margins have bottomed, but there is no guaranteed timeline for recovery.

The original shipbuilding order was canceled by a Japanese shipyard at the last minute. New vessels have since been ordered from Nakanishi Shipbuilding, but any further delay would cap Seaways’ capacity growth.

TCI Seaways is heavily dependent on the Port Blair island route. Any changes to cabotage laws allowing foreign ships on Indian coastal routes would immediately compress margins.

Supply Chain Solutions derives approximately 80% of revenue from the automotive sector. A sustained downturn in domestic passenger vehicle sales would directly damage the highest-margin segment in TCI’s portfolio. Sector concentration is a risk.

Fraudulent packers and movers operate illegally under the Agarwal and TCI brand names. Angry customer complaints from scam victims accumulate online, tarnishing the legitimate corporate reputation.

Truck driver shortages are inflating fixed costs by 15-20%. An aging driver workforce and poor social perception of the profession create a structural labor supply problem.

That’s it for today.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

FINVEZTO.COM | Build Wealth. With Clarity.

Amazing Analysis. Thank you.

Apart from all the threats - the shortage of drivers is the biggest RED FLAG, until the Auto pilots come in to India. Which may take at least a decade because of our Indians poor civic sense, lack of self discipline and reckless driving.

The biggest problem that India and Indian businesses gonna face is the next decade is the same.

No self discipline

No patriotism

No responsibility

No civic sense

Not even thinking of leaving a better place to the next generation.