This Company builds the Electronics inside Trains, Aircraft & Solar Farms and ships them Worldwide

Consistently Performing Stocks #71 || What has led to the consistency?

The full report of this stock including qualitative analysis, quantitative analysis, valuation, risk and red-flag checks is available here: https://finvezto.com/reports/avalon-machines-you-never-see

The following is the qualitative analysis.

Let’s Begin.

The control panel in an aircraft cockpit.

The system that brings a train to a stop.

The power box humming inside a solar farm.

The diagnostic unit in a hospital.

Different industries, different brand names on the outside. Underneath, a single Chennai company has built all of them.

You will almost never see the company's name on the machine, because the name on the box belongs to the customer. That company is Avalon Technologies.

It runs an Electronic Manufacturing Services business, EMS for short, and it has quietly become one of the largest pure-play EMS players in India.

The interesting part is its consistency. Revenue has compounded through a brutal industry downturn, the order book keeps climbing, and the balance sheet has stayed clean while the company doubled its output. This report walks through how that consistency is built.

This week, Let’s explore the business & fundamentals of Avalon Technologies Ltd. NSE: AVALON

Performance Chart

Their Road to Consistency

1. Overview and Business Model

Avalon Technologies builds complete electronic machines that other companies sell under their own brand. This is called Electronic Manufacturing Services, or EMS. Avalon makes complex, low-volume equipment for industries: the unit that brakes a train, the power box in a solar farm, a cockpit panel in an aircraft, a hospital diagnostic machine. Founded in 1999 in Chennai, with United States roots from 1995, it serves global industrial customers across two continents.

Think of building a car where one supplier delivers the wiring, body and dashboard fully assembled. Avalon does that for industrial electronics. This complete-machine delivery is its core edge.

Avalon makes nearly every part itself: circuit boards, cables, metal casing, plastic parts and magnetics. It then assembles them into one working machine. The client just adds its brand.

Avalon builds small batches of intricate, costly equipment. This low-volume, high-complexity focus shapes the entire business.

Avalon operates 12 manufacturing units. Two sit in the United States at Atlanta and Fremont, and ten across Chennai, Kanchipuram and Bengaluru. Genuine two-continent scale.

Its plants run 65 production lines: 10 surface-mount, 12 through-hole, 43 assembly. Surface-mount and through-hole are two ways to fix parts onto boards.

Promoters Kunhamed Bicha, the Chairman and Managing Director, and Bhaskar Srinivasan, the President, have run the business since inception.

The group runs the listed parent plus three subsidiaries. One sister company supplies critical parts captively, making up roughly 20 to 25 percent of consolidated revenue. Smart internal sourcing.

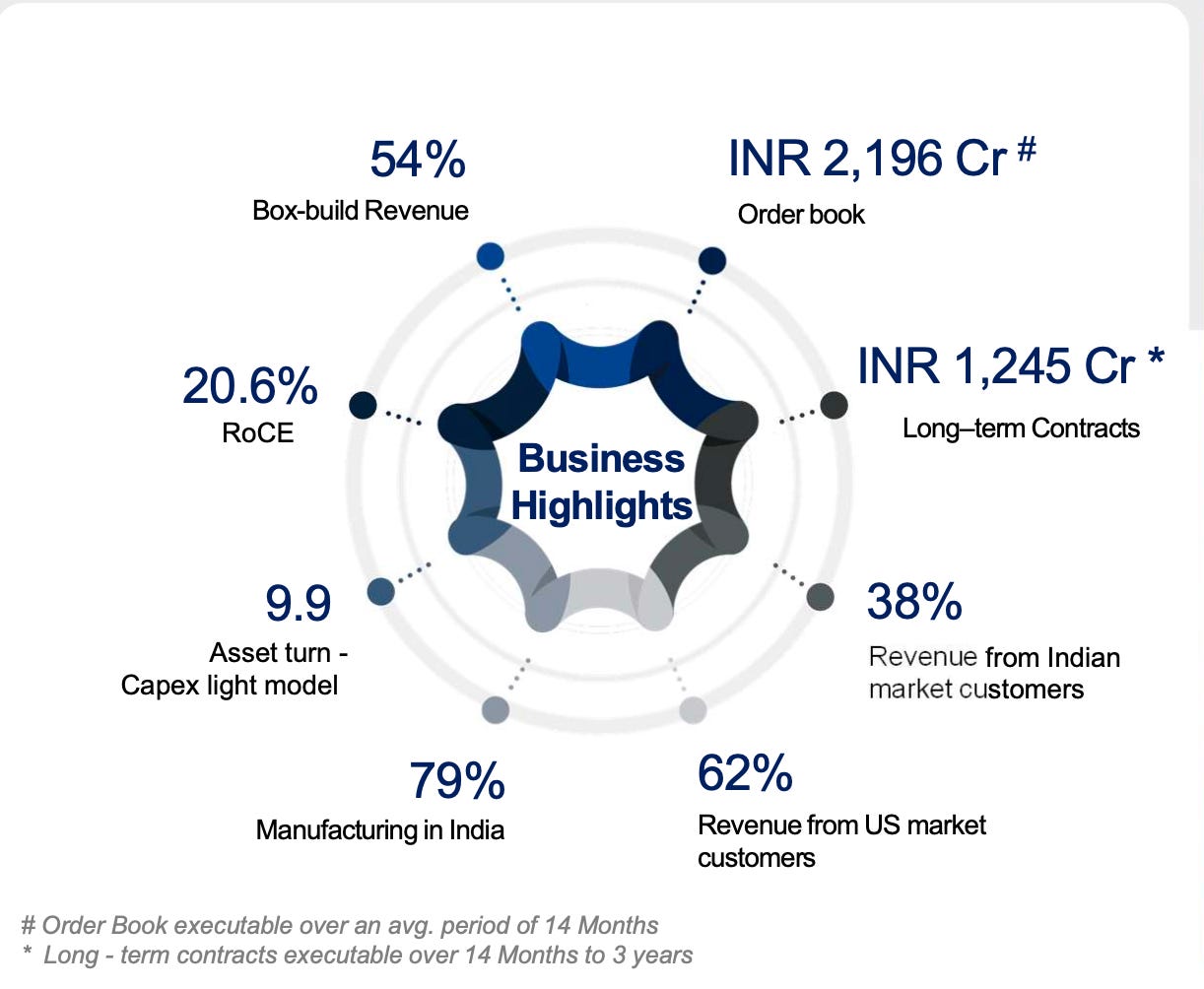

By manufacturing location in FY26, India produced roughly 79 to 81 percent and the United States 19 to 21 percent. The base stays firmly Indian.

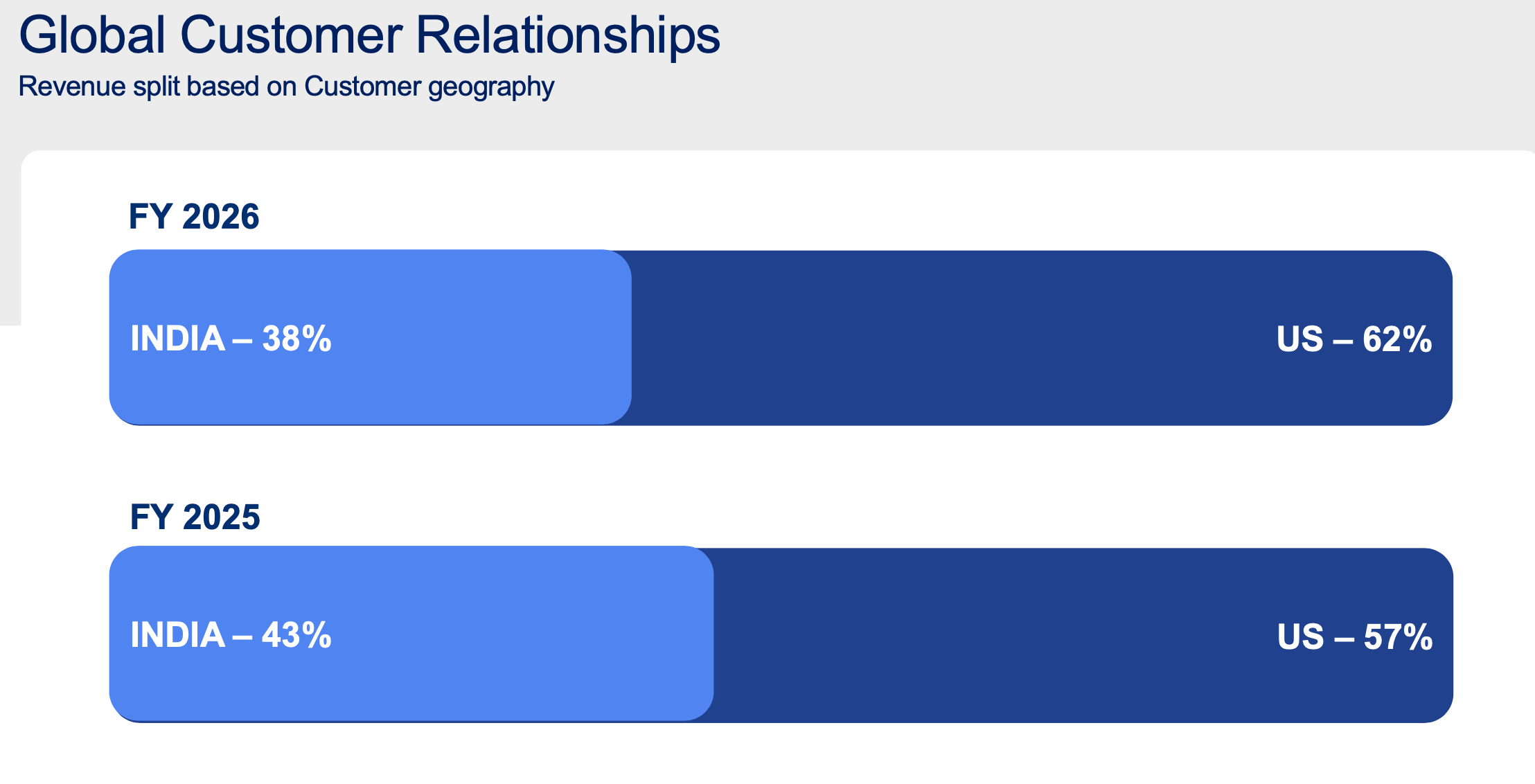

By billing geography in nine months of FY26, the United States gave about 62 percent of sales and India 38 percent.

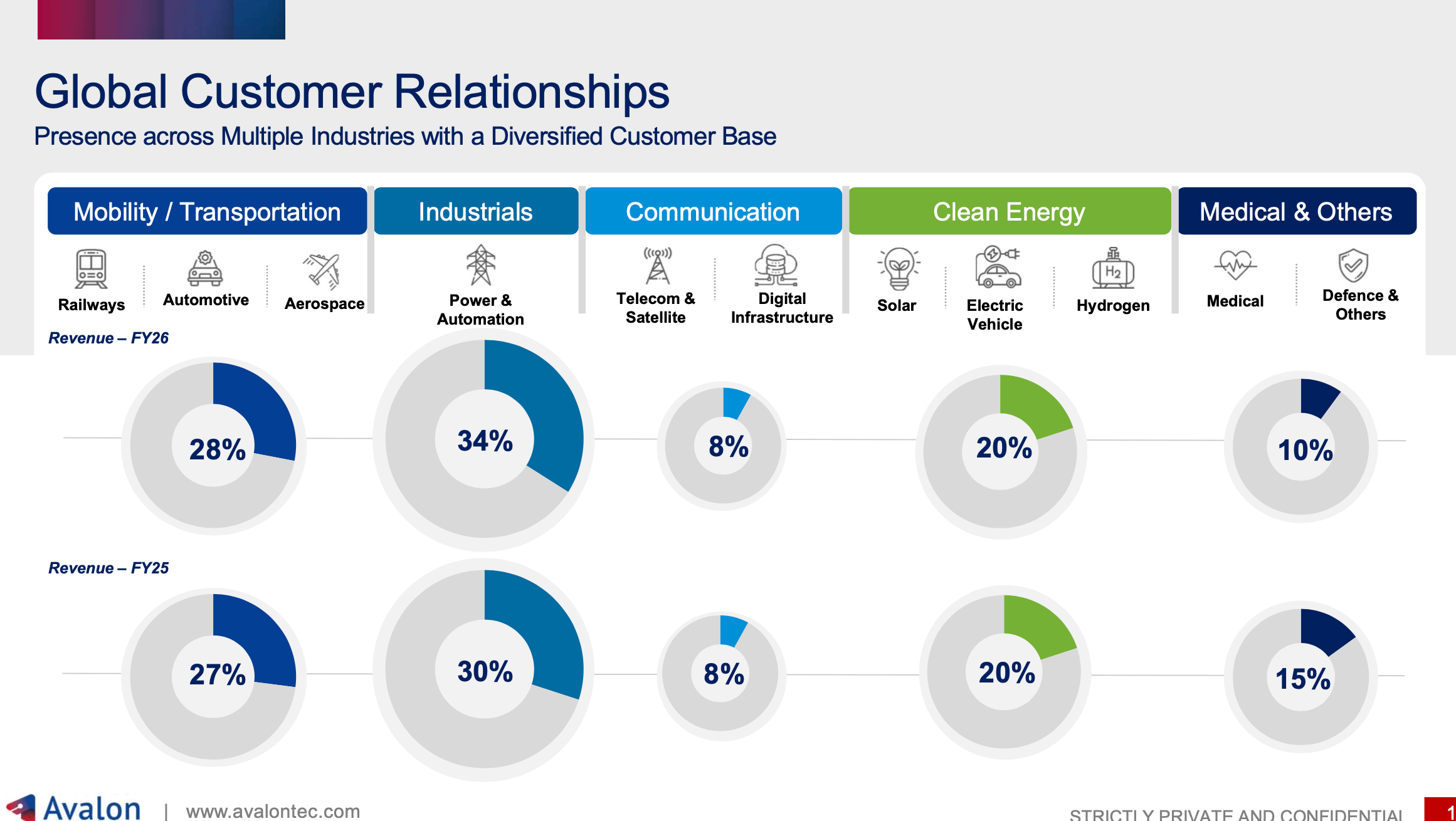

The FY26 vertical mix was Industrials 35 percent, Mobility 27 percent, Clean Energy 19 percent, Medical and others 10 percent, Communication 9 percent.

Certifications span aerospace, automotive, telecom and medical standards like AS9100 and ISO 13485. These let Avalon serve regulated, high-trust sectors.

2. Climbing The Value Chain

Avalon escaped the low-margin trap of basic assembly by moving into box-build. Box-build means delivering a complete, working machine instead of loose parts. This shift up the value chain protects margins, deepens customer ties, and explains why the company avoids brutal electronics price wars.

Box-build revenue reached 54 percent of total sales in FY26, up from about 44 percent in early FY25. Climbing the value chain steadily.

Integrated box-build revenue surged 106 percent year on year in the first quarter of FY26. Customers now buy whole systems, not components.

Complete systems carry richer economics than bare boards. Avalon held gross margins near 35.8 percent in FY25.

Building whole machines locks clients in for longer. Avalon secures commitments stretching up to 36 months. Switching suppliers mid-program becomes painful for customers.

Its aerospace certification lets it build cabins and regulated medical hardware.

Avalon designs custom plastics and metal sheets in-house. This mechanical control improved turnaround time. It wins time-sensitive contracts.

The box-build push helped EBITDA reach ₹114.9 crore in FY25 and ₹173 crore in FY26.

3. The Dual Shore Engine

Avalon builds early product samples at its US plants, close to American design teams and customers. Once the design is final, it moves mass production to low-cost India. This footprint expands margins, hedges tariffs, and keeps giant customers comfortable.

Atlanta and Fremont handle rapid prototyping next to American design engineers. Closeness wins early design slots.

Once designs stabilise, high-volume work shifts to Chennai. India’s lower costs lift profitability. A clean handoff between two shores.

The dual-shore setup let Avalon pass on 99 percent of tariff impacts in FY26. Trade wars barely dent margins. Flexibility is its tariff shield.

EBITDA margin climbed from 7.2 percent in FY24 to 10.8 percent in FY26. Indian operations alone delivered 14.8 percent in Q4 FY25.

Management targets a long-term 80 to 20 India-to-United-States manufacturing split. Keeping 20 percent local reassures American clients.

In FY26, the United States subsidiary drove most incremental growth, lifting US manufacturing share to 19 to 21 percent.

That US subsidiary, ABV Electronics, contributed ₹758 crore of FY26 consolidated revenue. American demand is doing the heavy lifting now.

The US unit still posted a small EBITDA loss of ₹7 crore in Q3 FY26. Losses are narrowing toward breakeven.

Global firms are diversifying supply chains beyond China, a shift called China plus one. This trend steers fresh contracts to Avalon.

4. Sticky Embedded Customers

Consistency starts with customers who cannot easily leave. Avalon embeds itself early in a client’s product design, then builds the components and the full system. These relationships run 15 to 20 years. Deep integration, regulated approvals and marquee names make switching slow, costly, and risky.

Avalon engages at the component design stage, not just assembly. This embeds it inside the customer’s engineering cycle. Early entry builds durable lock-in.

Many flagship relationships exceed seven years. Product lifecycles often stretch 15 to 20 years. Long programs mean repeating revenue.

Marquee customers include Collins Aerospace, Meggitt, Bloom Energy, ABB, GE and Bharat Electronics and Faiveley Transport, a Wabtec company.

Its customer count grew from 54 in 2020 to 89 by late 2022. New logos keep arriving. The base is widening, not just deepening.

Top three clients form less than 25 percent of open orders. No single exit can sink the backlog. Diversification reduces dependence risk.

Regulated approvals create high barriers. Once qualified for aerospace or medical work, suppliers are rarely replaced. Qualification itself becomes a moat.

Avalon’s quality systems run identically across India and the United States. This unified control lets work move shores seamlessly. Customers feel no quality drop.

Once a client transfers a line to Chennai, costs fall for them too. Lower prices plus proven quality keep retention high. A win-win that locks loyalty.

5. Five Vertical Resilience

Avalon spreads revenue across five sectors: industrials, mobility, clean energy, communication and medical. When one cools, another surges. This structural spread is exactly why a brutal FY24 customer destocking did not permanently break the company’s growth path.

The five verticals are industrials, mobility, clean energy, communication and medical devices. Each cycles differently. Weakness in one is offset elsewhere.

Industrials led FY26 at 35 percent of revenue and grew about 67 percent year on year in Q3. Heavy machinery demand stayed strong.

Mobility contributed 27 percent of revenue. Railway signaling and braking grew roughly 70 percent year on year. Rail modernisation budgets are flowing to Avalon.

Aerospace, inside mobility, grew about 64 percent year on year in late FY26. Long program recoveries add high-margin revenue.

Communication revenue jumped 102.6 percent year on year in the first quarter of FY26. 5G and satellite deployment drove it.

In FY25 every vertical expanded. Clean energy rose 66 percent, mobility 113 percent, industrials 35 percent and communication 53 percent.

Shared component sourcing across sectors boosts bargaining power. Avalon squeezes better volume discounts from chip suppliers. Many verticals with 1 efficient supply chain.

6. The Clean Energy Engine

Clean energy turned into a major growth driver. Avalon builds solar inverters, hydrogen fuel cell parts, electric vehicle chargers and battery storage systems. A United States tax deadline has pulled demand forward sharply. This green alignment opens a large, multi-year commercial runway for the company.

Clean energy formed about 19 percent of FY26 revenue and grew roughly 35 percent year on year in Q3. Decarbonisation spending is finding Avalon.

It designs solar hybrid power inverters for global energy brands. These repeat orders keep its production lines running steadily, not idle. Busy lines spread fixed costs and protect margins.

Avalon also builds parts for hydrogen fuel cells and electric vehicle chargers. This shows engineering range beyond solar inverters. The same factories handle several green products.

A United States law, the One Big Beautiful Bill, sets solar tax-credit deadlines. Developers must finish construction by December 2027 as per the policy.

To claim credits, developers must start building by July 2026. This triggered a rush of orders, spiking the backlog and lifting guidance.

Its dual-shore setup lets it shift solar production between countries. Trade-law changes cause minimal long-term harm. Flexibility protects this growth engine too.

The United States energy storage market is growing 60 to 70 percent. Developers are ordering battery systems aggressively.

Avalon plans to migrate clean energy lines to India over time. Lower assembly costs should expand gross margins.

7. A Visible Order Book

Investor confidence in a manufacturer comes from visibility. Avalon’s order book delivers exactly that. A large, diversified and multi-year backlog keeps factories busy and earnings predictable. Consistent inflows let management plan inventory tightly and raise guidance, signalling that demand is compounding rather than fluctuating quarter to quarter.

The short-term order book reached ₹2,196 crore by March 2026, up about 24.7 percent year on year. Execution runs over the next 12 to 14 months. Strong near-term visibility.

On top sit long-term contracts worth roughly ₹1,245 crore, spanning 15 to 36 months. These stabilise factory utilisation. Long contracts smooth out the lumps.

Letters of intent, which are preliminary commitments, add about ₹949 crore. Avalon plans expansion against them proactively. Demand visibility ahead of spending.

The total pipeline peaked near ₹3,190 crore in late FY26. This cushion improves bargaining power with chip suppliers. Scale begets supply security.

Order inflows grew 29 percent year on year in Q4 FY26. Global brands increasingly pick Avalon over unorganised regional players.

Top three clients hold under 25 percent of open orders. No single client dominates the backlog. The pipeline is structurally insulated.

This visibility let management raise FY26 revenue growth guidance to 40 percent mid-year. Confidence backed by signed orders.

For FY27, management conservatively guided 24 to 27 percent revenue growth. They prefer under-promising. A refreshing habit in a hype-prone sector.

8. Asset Light Balance Sheet

Avalon doubled output without piling on debt. It expands through cheap brownfield additions, not costly new factories. This keeps the balance sheet clean, asset turns high, and interest costs minimal. Tight working capital then converts profits into real cash, funding growth without expensive borrowing or share dilution.

Avalon built a new export-focused Chennai plant for just ₹15 crore. Capacity grew without heavy borrowing.

Annual capital spending runs only ₹50 to 60 crore. Gross fixed asset turnover hit 9.5x in Q3 FY26.

The debt-to-equity ratio sat at a tiny 0.08x in December 2025. Net debt is near zero.

Gross debt fell to ₹163 crore in the first half of FY26. The company pays down loans while expanding.

Almost all remaining debt is short-term working capital, with no long-term obligations. Interest costs stay minimal.

Interest coverage improved from 6.9x in FY25 to 8.7x by the first half of FY26. Profits comfortably cover interest. The financial cushion is thickening.

The net working capital cycle shortened from 161 days in March 2024 to 112 days in March 2026. Cash is being freed up.

Receivable days fell to 72 and inventory days to 86 in late FY26. Faster collection, leaner stock. The cash engine is improving.

Operating cash flow turned positive at ₹57 crore in FY26, against ₹25 crore earlier. Profits are becoming cash.

Avalon held ₹100 crore of unencumbered cash in December 2025. The current ratio was a comfortable 2.22x.

9. New Growth Verticals

Avalon is seeding tomorrow’s revenue today. It is entering semiconductor equipment, railway safety electronics, drone power systems and satellite communication. Each leverages existing in-house capabilities, so new vectors open without heavy fresh debt. These premium, sticky niches could lift margins and reduce dependence on any single mature segment.

Avalon partnered with a global semiconductor equipment maker to build Industry 4.0-compliant boxes. Industry 4.0 means smart, connected factory systems. A high-tech leap.

Prototype development and technical readiness are done, with production approval pending. Meaningful semiconductor revenue is expected from FY27.

These complex systems need advanced mechanical and electronic engineering. Simple assemblers cannot compete. Once qualified, suppliers stay for years.

Avalon uses its in-house sheet metal and machining for this work. Internal sourcing controls cost, helping it price against Chinese suppliers. Vertical integration pays off.

It is building Kavach, the Indian Railways anti-collision safety system. Commercial production is expected in the second half of FY27. Riding rail modernisation directly.

Avalon took a roughly 4.05 percent stake in Zepco for drone motors and power electronics, priced near ₹306.55 per security. Betting early on drones.

It is also expanding into aerospace cabins, locomotive engine subsystems, energy storage and satellite communication. Adjacent, high-engineering work.

Semiconductor and defence niches carry premium margins and long lifecycles. They reduce reliance on cyclical consumer demand. A deliberate climb toward resilient, high-value revenue.

That’s it for today. Read the full deep-dive report on finvezto.com → https://finvezto.com/reports/avalon-machines-you-never-see

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.