The Market Is Structured Against Retail Traders. Here Is How to Overcome It.

Your strategy looks great and profitable. But, your live account keeps losing. The reason is not your strategy. It is market structure.

Have you ever wondered why a strategy that looks profitable on paper keeps bleeding money in live markets?

Or why trading more to recover losses only makes things worse?

Or how Props and FIIs make a profit to the tune of ₹60,000 crore in the same market that you are trading while your account keeps losing?

These are not random outcomes. There is one concept that connects all the 3 questions above.

Once you understand it, you will never look at your trades, your backtest, or your capital the same way again.

If you prefer watching over reading, I have covered this article in much more detail in the video below. Else, keep reading.

Let us look at some data before getting into the concept.

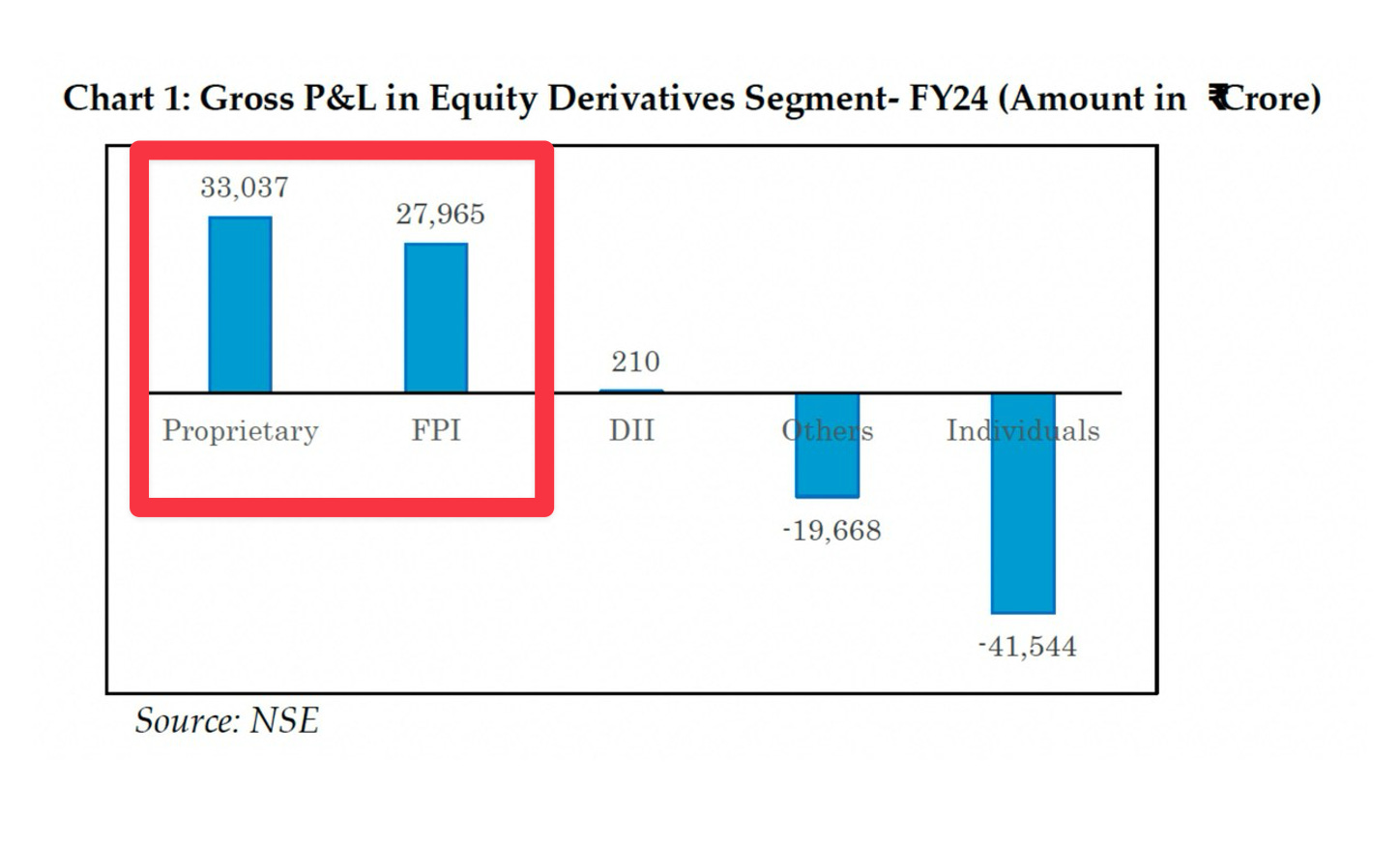

Who Is Actually Making Money in F&O Trading?

SEBI released the following data in 2025.

Proprietary traders earned ₹33,037 crore gross in FY24. FPIs earned ₹27,965 crore. Individuals and others collectively lost ₹61,212 crore in the same year.

This is not one bad year for retail traders. It has happened every time in the past, and it will happen every time in the future also. This is the structural reality of the market.

The natural question is: What exactly are props and FPIs doing that retail traders are not?

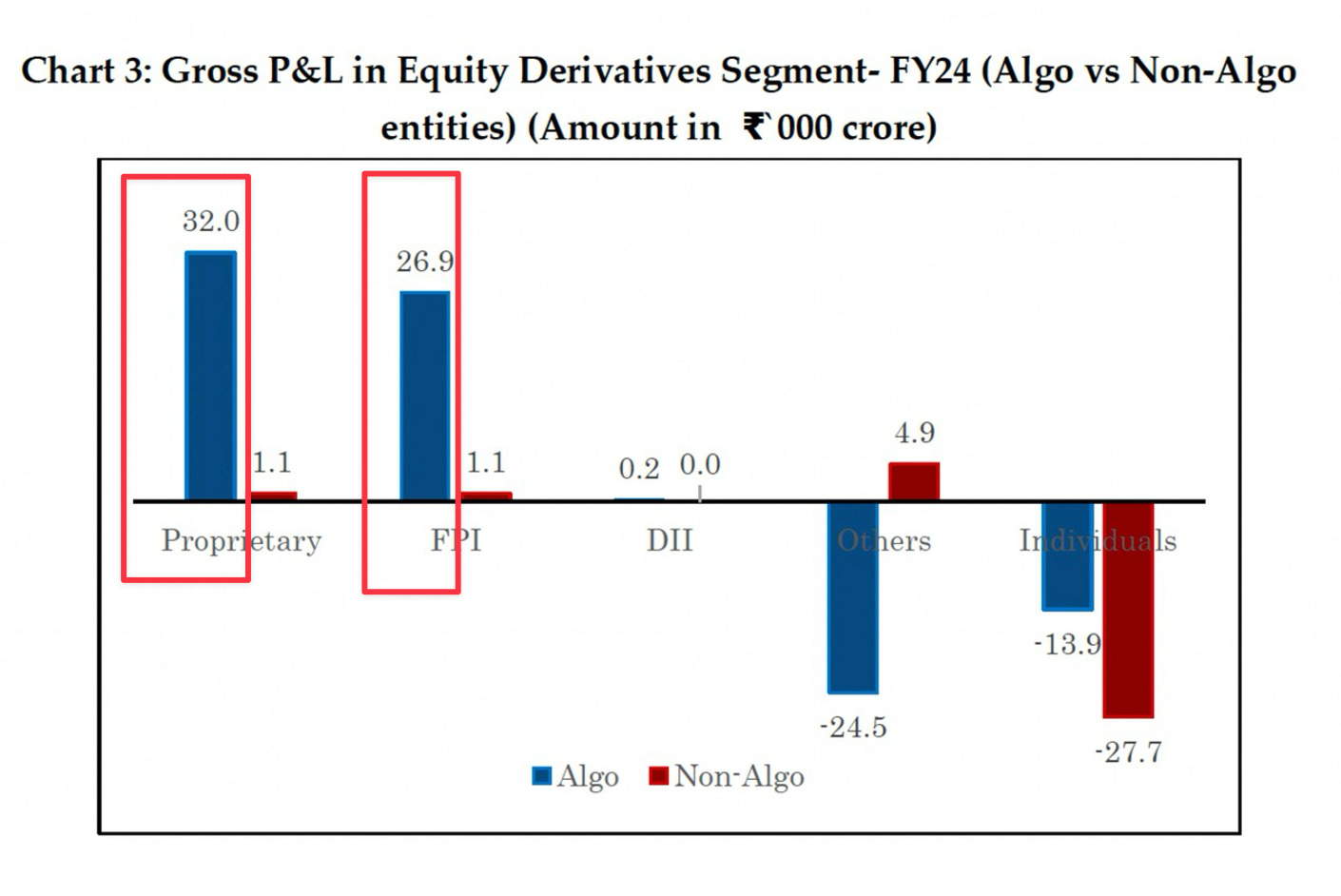

Almost All of It Comes from Algos

96% of proprietary trader profits in FY24 came from algo trading. For FPIs, that number was 97%. Non-algo profits were marginal for both categories.

This tells you something important. The edge these institutions hold is not gut feel or discretionary trading. It is systematic, algorithmic execution at a very large scale.

The next logical question is: What are these algos actually doing?

Are these Algos Directional or Non-Directional?

There are ~1,000 prop and FII entities in total. On the other side, there are crores of retail traders.

Each retail trader averages ₹11,824 per transaction and makes roughly 875 transactions per year (Source: NSE & SEBI)

Think about what this means structurally.

Retail traders collectively generate few crores of transactions every single day. Props and FPIs are mostly the counterparty to these crores of transactions. That is, they are on the opposite side.

Effectively, Props are making small profits per trade across crores of trades. This business model is only possible with a non-directional strategy.

A directional strategy, on the other hand, works by taking fewer, larger bets. You hold them long enough for the thesis to play out. Profit per trade is high. Trade count is low. So, Props are not doing this.

The Prop model is the exact opposite. High trade count. Very small profit per trade.

That structure can only mean one thing. That is Market Making.

What are Market Making Algos

Market makers do not predict where the market is going. They are not long or short based on a view.

They sit on both sides of the order book continuously. They place limit orders to buy and sell simultaneously.

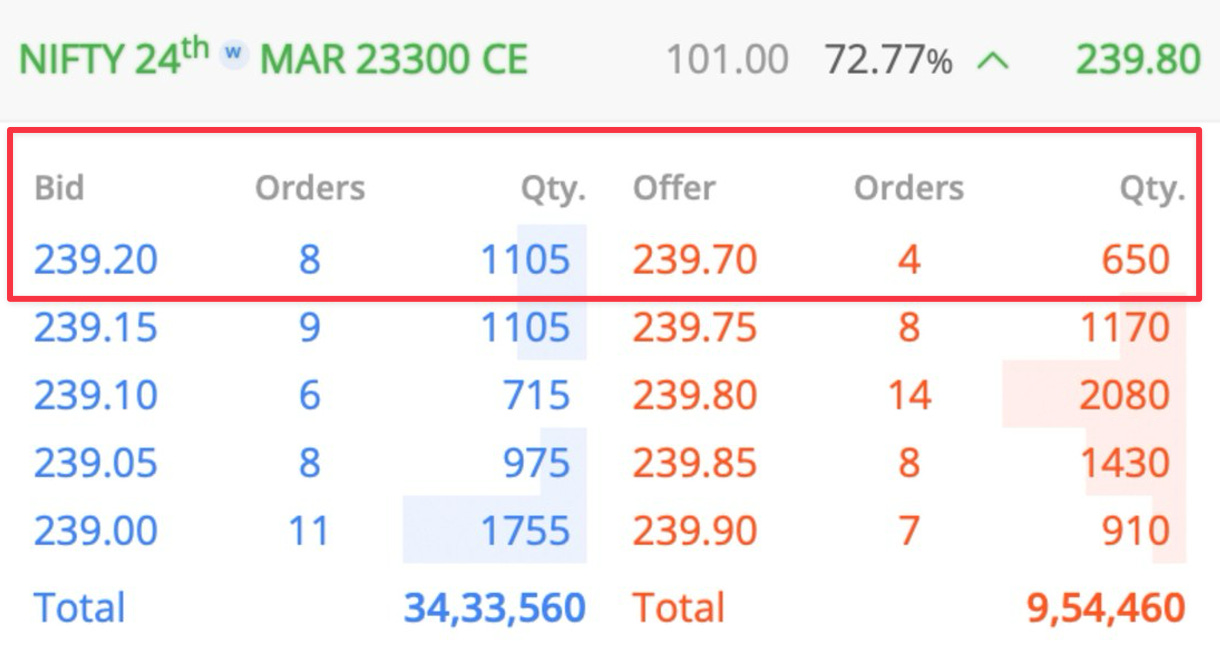

Look at the market depth of the Nifty options below. All these orders that you see are limit orders and are mostly placed by the market makers (Props).

Every time a retail traders sends a market order, a market maker’s (PROP) limit order is on the other side of that transaction.

They enable your transaction. In return, they collect a small fee on every single trade.

To understand this better, you need to know the concept of bid ask spread.

What Is Bid-Ask Spread?

Open any options contract. I have loaded the NIFTY 23,300 call option below. You will see two prices in the market depth. Bid and Offer.

The bid is the highest price a buyer is willing to pay.

The ask (or offer) is the lowest price a seller is willing to accept.

The bid is ₹239.2 and the ask is ₹239.7 as in the above pic.

If you buy at market price, you pay ₹239.7. If you immediately sell at market price, you receive ₹239.2. That gap of ₹0.50 is the fee you paid to the market maker. That is, you paid it to the PROP Traders.

That spread as a percentage is almost 0.21% of the Premium. That is a hidden cost that you dont see.

It does not sound like much. But every single trade you take, on both the buy and the sell, carries this cost. It adds up fast. I will show you a detailed calculation later in the article.

This is one of the reasons why Props are making thousands of crores every year. Almost guaranteed.

Here is a simple way to understand this.

Have you gone to Airport Money Exchange Counter?

USD/INR trades around ₹93.9 in the open market. Walk up to an airport forex counter and ask to buy $1. You will pay around ₹95. Come back from your trip and try to sell that dollar back. You will get only ₹89.

You buy above the market rate. You sell below the market rate. The ₹6 difference is pocketed by the exchange counter. That is their bid-ask spread.

Now ask yourself: would you go to that counter 10 times in a day to transact dollars?

Of course not. One transaction costs you ₹6. Ten transactions cost you ₹60.

You would go once when you need dollars and once when you return. That is it.

But in the markets, most traders do exactly this. They believe more trades means more opportunity. It does not.

More trades means more spread paid to market makers, more brokerage paid to brokers, and more taxes paid to the government.

Market Making Is Everywhere

Market making is not unique to Indian options. It happens across every asset class and every market in the world. Equities, bonds, currencies, commodities.

Wherever there is a buyer and a seller, there is almost always a market maker sitting in between, collecting the spread on every transaction.

It is also one of the most consistently profitable trading activities in the world. Not because market makers are smarter. But because the structure of the market guarantees them a fee on every single trade, regardless of direction.

This is what you need to understand before you trade any instrument. Is market making prevalent in this instrument? If the answer is yes, then making consistent intraday profits becomes extremely difficult.

You are essentially fighting an entity that gets paid whether the market goes up or down, and gets paid every single time you transact. Props are doing exactly this.

In liquid options like Nifty and BankNifty, market making activity is very high. The market maker’s edge compounds across millions of trades every day.

This is also the reason why scalping, intraday options buying and overtrading in Nifty and BankNifty are almost always losing strategies for retail traders.

Every time you enter and exit quickly, you are paying the spread twice. Once on the entry and once on the exit. Do this ten times a day and the spread alone will erase whatever small profit your strategy was trying to capture.

Why Your Profitable Strategy still loses

Whenever I backtest or forward test a strategy, I simulate the total market cost of the strategy using the calculator below. You can access the calculator here.

On the left-hand side of the calculator, the inputs, and on the right-hand side, you will see the output. You can enter the details of your strategy on the left-hand side to get an estimate of the total market cost.

Assume you have ₹2 lakh capital.

You risk 1% per day, which is ₹2,000. Your risk-reward is 2:1, so you target ₹4,000 on winning days. You win 60% of the days. Your strategy deploys 10 trades per day.

I have entered the details above in the calculator, and I got the total market costs on the right hand side.

On paper, the gross profit of this strategy is ₹4 lakh per year. The strategy looks excellent before the costs.

Let us now deduct the costs. Here is the actual cost structure of this strategy:

Regulatory costs (brokerage, STT, transaction charges, GST, stamp duty) come to approximately ₹1,59,000 per year. Most traders know this and account for it in their brokerage calculator.

Bid-ask spread at 0.21% per trade comes to approximately ₹75,000 per year. Most traders never account for this.

Slippage at 0.5% per trade comes to approximately ₹1,87,000 per year. This is the difference between the price you expect and the price you actually get. We will cover slippage in detail separately in another article. For now, just understand that there will always be slippage.

Total market cost is ₹4,21,000.

Your gross profit was ₹4,00,000. Your total costs are ₹4,21,000. The strategy is now a loss-making one.

An extraordinary strategy on paper becomes a loss-making strategy in practice. The reason is not bad entries or bad exits. The reason is bid-ask spread, slippage, and cost.

Why ₹1-2 Lakh Capital Is Not Enough for Trading

With ₹1-2 lakh trading capital, the math simply does not work.

The fixed costs alone are significant relative to the capital base. Regulatory costs, bid-ask spread, and slippage eat into a disproportionately large portion of your profits.

If you trade with ₹1-2 lakh in F&O, you will not be profitable even if your strategy is genuinely good. The market structure does not allow it.

Action Points for you

You should implement these things immediately.

Every backtest you do hides bid-ask spread, slippage, and regulatory costs. Always add these three before concluding that a strategy is profitable. After accounting for all three, very few strategies retain a genuine edge.

₹1-2 lakh capital for F&O trading is not enough. Some good strategies start returning real profits only above ₹5 Lakh. That too, you should first invest for the long term and then pledge those holdings and only trade in F&O.

More trades is not more opportunity. Every additional trade is a donation to market makers, to brokers, and to the government. Traders who survive long enough take fewer trades. Aim for a maximum of one to two adjustments per day. If your strategy is still in a loss after two adjustments, close the trade for the day. Avoid scalping, intraday options buying, and over-trading.

Avoid F&O trading till you build at least 15 lakhs in capital. Once you build a capital of 15 lakhs, you can use F&O for hedging and income generation. You can do both Hedging and Income Generation by pledging your investments. Do not trade in F&O for speculation. The only people who win are the Brokers, Props, Exchange, SEBI and the Government.

A Mental Model for Survival

Most traders spend their time changing their rules. A new indicator. A new entry signal. A new stop loss level.

The ones who survive understand something deeper. There is a structure to markets that cannot be changed. And there are principles that must never be broken.

Think of it in 3 layers.

Structure includes bid-ask spread, taxes, and slippage. These costs exist. They will always exist. In trading, you should always know who is on the other side. Understanding structure tells you the minimum edge your strategy needs to have before it can be profitable.

Principles include risk management and position sizing. These must not be broken. Never ever.

Rules include your charts, your indicators, your specific entry and exit criteria. These can be different for different people. And they keep changing.

The ones who survive understand the structure and never break the principles.

The Devil is in the Details

The bid-ask spread is not a small detail. It is the mechanism through which bulk of the ₹61,000 crore flows from retail traders to market makers (Props) every single year.

Understanding it does not mean you should stop trading. It means you should trade less, trade smart, and always know the true cost of every transaction before you enter a position.

In the upcoming weeks, I will be covering more topics around market structure and other key areas.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

Regulatory cost and spread cost was eye opener when put on black and white.kudos for bringing it to the forum

Guys like Susquehanna understood this decades ago and quietly make billions of dollars of profit on the sidelines.