Shivalik Bimetal Controls Ltd (SBCL)|| Consistently Performing Stocks #65

What has led to the consistency?

Every week I analyze a company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.

This week, Let’s explore the business & fundamentals of Shivalik Bimetal Controls Ltd (SBCL).

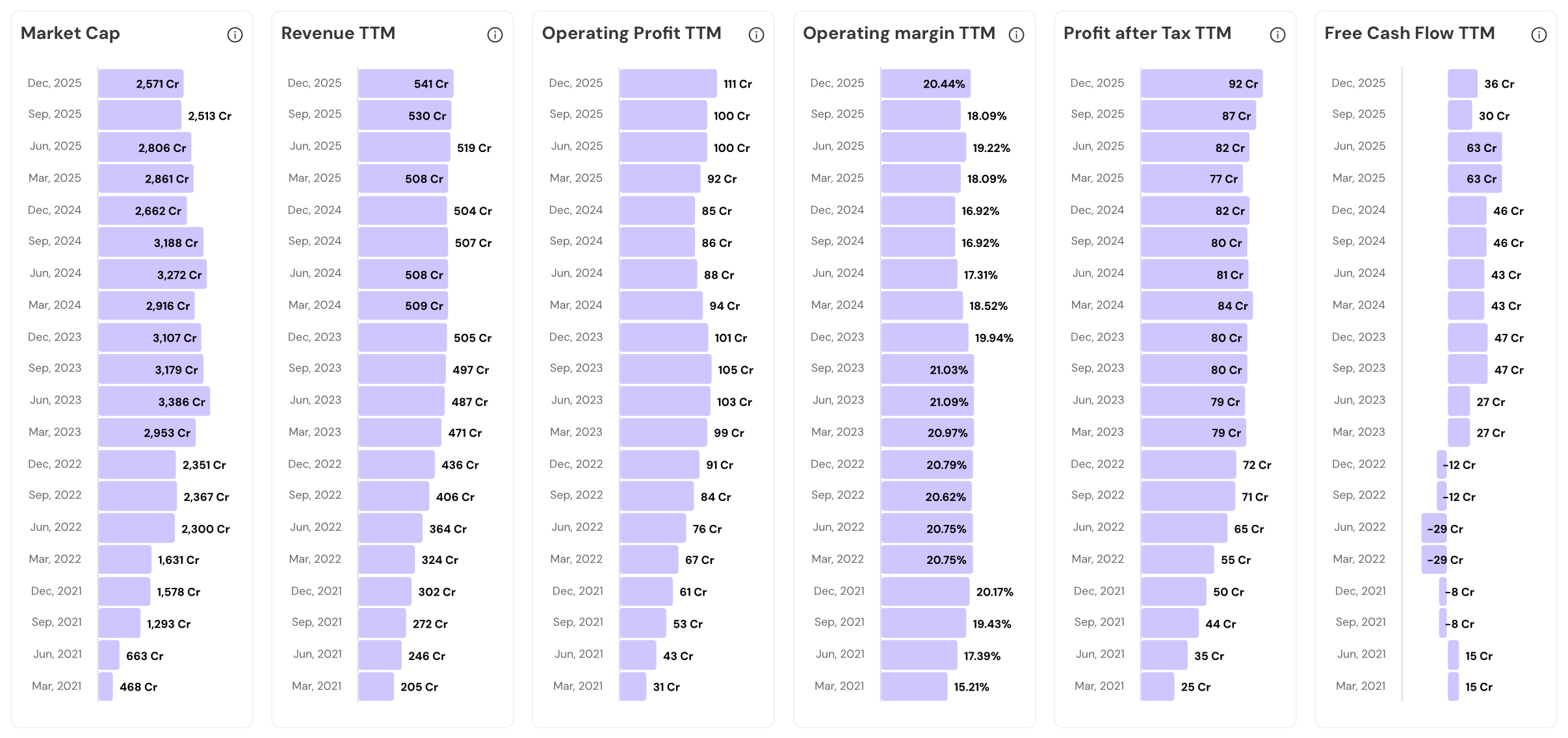

Performance Chart

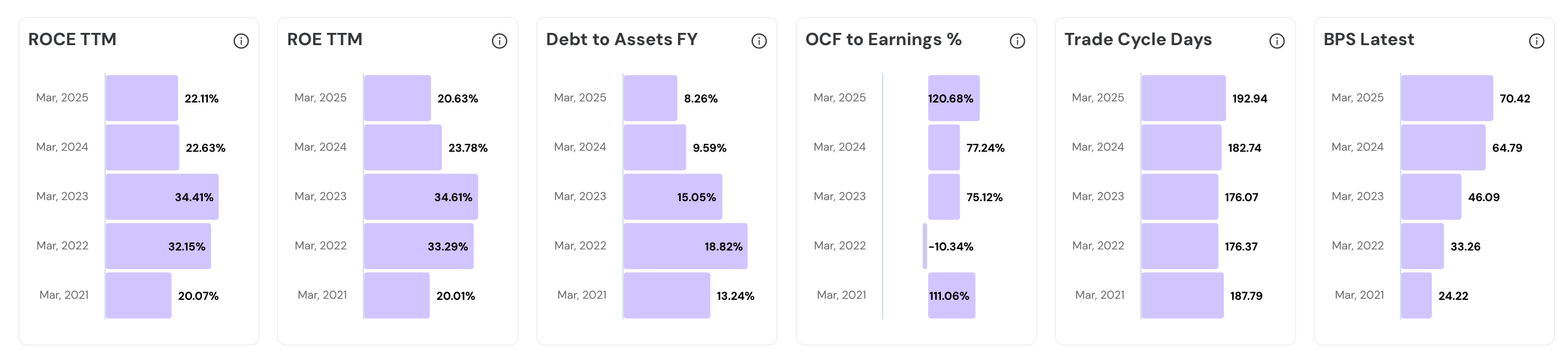

Quality Chart

Their Road to Consistency

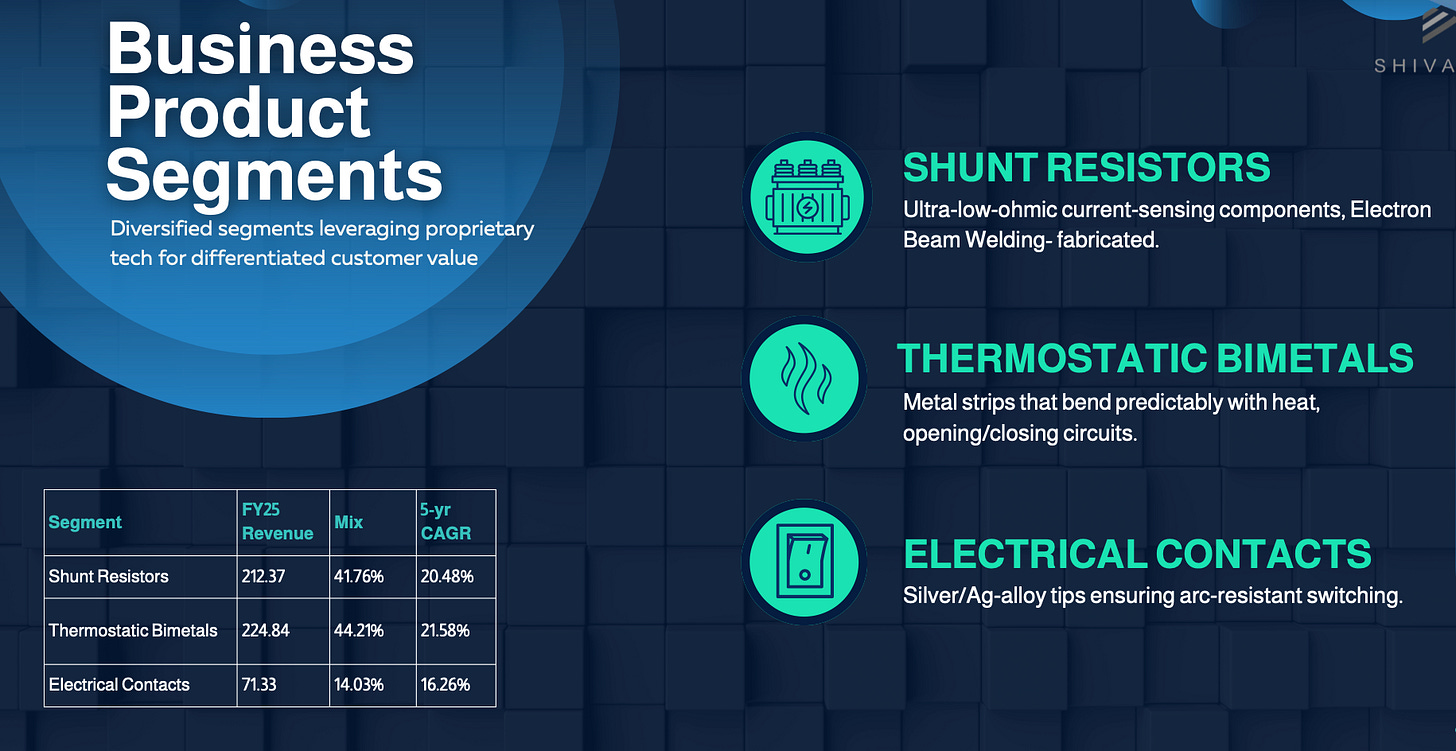

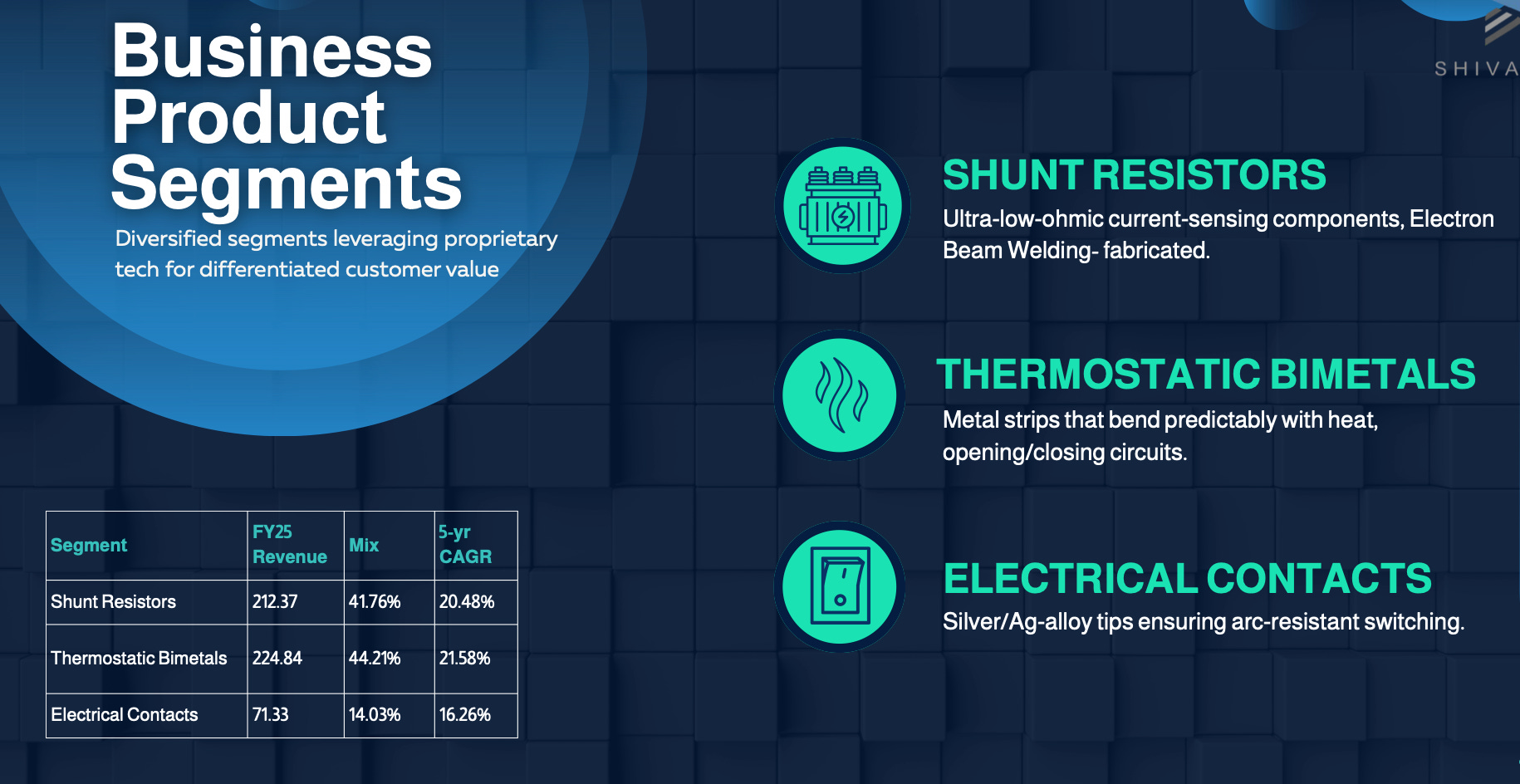

1. Overview and Business Model

Shivalik Bimetal Controls Limited (SBCL), founded in 1984, is India’s only fully integrated manufacturer of thermostatic bimetals, low-ohmic shunt resistors, and electrical contacts. These tiny precision components enable accurate current sensing, thermal switching, and circuit protection across electric vehicles, smart meters, and industrial switchgear.

Imagine your circuit breaker at home. When electricity overloads, a tiny metal strip bends from heat and cuts the power before a fire starts. Shivalik makes that metal strip. They also make the tiny sensors inside EV batteries that prevent them from exploding, and inside smart electricity meters that measure your bill.

SBCL operates 3 manufacturing campuses in Solan, Himachal Pradesh. It partners with 300+ OEM and Tier-1 customers across 38 countries.

Three product segments drive revenue.

Thermostatic bimetals contribute 44.21% (₹224.84 crore),

shunt resistors 41.76% (₹212.37 crore), and

electrical contacts 14.03% (₹71.33 crore).

Exports account for 56.22% of FY25 revenue.

2. Bimetal Monopoly

Shivalik controls approximately 90% of India’s thermostatic bimetal market and holds a 16% share globally. With 77 proprietary diffusion-bonded grades, the company has built an almost impenetrable domestic position in a safety-critical segment. Even in FY26, no serious Indian challenger has emerged.

Shivalik controls roughly 90% of India’s thermostatic bimetal market. Almost every switchgear manufacturer here depends on them.

The company offers 77 proprietary bimetal grades. The global median for competitors is around 10 grades.

Diffusion bonding fuses metals at the atomic level under high heat and pressure. Each grade gets a unique metal recipe involving nickel, copper, and manganese.

The global bimetal market is projected to grow from ₹1,600 crore to ₹2,800 crore by FY30. Shivalik holds 16% today and is targeting 22%. Growing in an expanding market is relatively easier.

In the switchgear application, bimetals are the heat-sensing element that trips circuit breakers. Switchgear accounts for roughly 80% of bimetal supplies, per the Q3 FY26 earnings call.

Household appliances contribute 15-20% of bimetal segment revenue. Irons, geysers, and coffee makers generate repeat orders that are demand-inelastic.

In 9M FY26, bimetal Europe revenue grew 47.95% year-on-year to ₹36.81 crore. This happened when European industrial demand was broadly weak.

Bimetal capacity utilisation is only 38-39% currently. The company can more than double output without new factory construction.

3. Electron Beam Welding Edge

Shivalik is one of a handful of companies globally that can produce electron beam welded shunt resistors at commercial scale. In India, it is the only such manufacturer.

Electron beam welding fires electrons at high velocity in a vacuum to fuse dissimilar metals. The joint is exceptionally clean and does not disturb electrical conductivity. Precision here is non-negotiable for battery sensing.

Shivalik is India’s only EBW shunt resistor manufacturer. Every domestic competitor must import these parts.

Globally, the primary competitor is Isabellenhütte of Germany. Being the only credible alternative to a German leader gives global OEMs a politically important second source. The China-plus-one and Germany-plus-one logic both benefit Shivalik.

Shivalik commands 12-13% of the global shunt market and is targeting 18%. The segment grew at a 5-year CAGR of 20.48% through FY25. This is the fastest-growing segment in the portfolio.

The shunt manufacturing process involves 14-15 sequential in-house steps after the initial weld. Each step adds to the defensibility. Replicating this entire chain takes years and substantial capital.

By 9M FY26, shunt revenue reached ₹171.45 crore, up 9.28% year-on-year. India shunts grew 21.18% in the same period. The domestic smart meter rollout and recovering exports are driving this acceleration together.

In EV Battery Management Systems, shunts measure cell-level current in real time. Incorrect measurement means battery fire risk or premature degradation. Tier-1 automotive qualifications for these parts take 1-2 years to obtain.

About 60% of shunt revenue goes to automotive and 35% to energy meters, per the Q3 FY26 call. This split means Shivalik benefits whether you buy a new car or a smarter electricity meter. Two independent demand drivers.

Shivalik operates Asia’s largest EBW strip facility. Scale enables large supply agreements with global giants.

4. In-House Machine Advantage

Shivalik designs and builds its own EBW machines at roughly half the cost of global procurement. A machine that takes two years to import globally is ready in six months when built internally. This capability compresses capex, protects intellectual property, and lets the company expand capacity on demand.

Building an EBW (Electronic Beam Welding) machine in-house costs Shivalik approximately 50% less than buying from a global supplier.

A machine ready in six months versus two years. It lets management respond to demand signals immediately. In a market growing at 20%, six months of lost capacity is meaningful lost revenue.

Shivalik operates 8-9 specialized EBW machines, each a custom build. Every new machine is better than the last.

No external technician accesses the core welding machinery. Intellectual property stays entirely within the factory walls.

In-house machine building directly supports the EBITDA margin profile. Royalties and service fees to external vendors are eliminated.

FY25 capex was ₹29 crore while operating cash flow was ₹92 crore. This is one of the cleanest capital efficiency ratios in Indian small-cap manufacturing.

The new Pune bus bar facility, approved in Q3 FY26, required only ₹20 crore capex. The expensive EBW equipment already exists in Solan. Pune is incremental assembly infrastructure riding existing technology.

MD Kabir Ghumman said it directly: “Our dual-process fortress of EBW and diffusion bonding is unique globally. Competitors face euro-denominated inflation and 24-month lead times.”

5. Smart Meter Tailwind

India’s plan to replace 250 million electricity meters with smart ones is creating a structural demand wave for Shivalik’s shunt resistors. Their components account for roughly 70% of the bill of materials inside smart meter relays.

The Indian government sanctioned 250 million smart meters under the RDSS programme, targeting completion by 2025-27. This is one of the world’s largest electrical infrastructure rollouts. Shivalik is directly embedded in the supply chain.

A smart meter’s shunt resistor converts electricity flow into a measurable signal for billing. Without it, the meter cannot work. Shivalik components represent about 70% of relay bill-of-materials.

The global smart meter market is projected to grow from $250.7 million in 2023 to $763.2 million by 2031 at roughly 15% CAGR.

In 9M FY26, India shunt revenue grew 21.18% year-on-year to ₹62.37 crore. This is the strongest geographic growth for the shunt segment.

HPL Electric, one of India’s largest meter manufacturers with a 20% domestic market share, uses Shivalik components.

The RDSS programme includes localisation clauses, giving Indian component makers a structural edge. Foreign suppliers face additional compliance cost.

Shivalik has applied under the ECMS scheme, the successor to PLI, per the Q3 FY26 call. Approval is pending. Qualifying would provide direct financial incentives linked to revenue growth.

Smart meter latching relays also use Shivalik’s electrical contacts. The same government rollout that drives shunt demand simultaneously drives contacts segment demand. Two product lines benefit from one policy.

Smart meter shunts barely existed as a revenue line in FY22. They now contribute roughly 35% of total shunt revenue. A market created almost from scratch within 5 years.

6. EV Electrification Bet

Electric vehicles require 8 to 16 times more shunt resistors than conventional internal combustion cars, and each EV carries three times the shunt value. Shivalik is already in the global automotive supply chain and has now announced a forward-integration play into EV bus bars and assembly components.

An EV battery pack needs a shunt at every cell group to monitor current in real time. This is a safety and performance requirement. The shunt content value per EV is 3x higher than per petrol car.

Shivalik supplies Tier-1 names like Bosch, Continental, and Denso. These companies build systems that go into vehicles from Tesla, BMW, and Ford.

Vishay, which buys approximately 40% of Shivalik’s shunts, has developed components for the top two global EV manufacturers. Per the Q3 FY26 call, this business is already in regular supply.

The global EV shunt market stood at $2.98 billion in 2024 and is projected to reach $4.09 billion by 2029. Shivalik is targeting 17-18% of this market. Current global share is 12-13%.

The board in Q3 FY26 approved a new Pune facility for automotive bus bars, EBW-welded connectors, and assemblies. Revenue guidance for the forward integration initiative: ₹70-75 crore in FY27, ₹150-200 crore in FY28, ₹250-300 crore by FY29.

Bus bar assemblies for two-wheelers carry a value of ₹2,000-3,000 per vehicle. Shivalik previously supplied components worth ₹100-400 per vehicle.

The two EV two-wheeler development partners are India’s number-one and number-two two-wheeler manufacturers overall, per Q3 FY26 call. Their scale means small adoption percentages translate into large order volumes.

Hybrid cars also use Shivalik shunts, just like pure EVs. Even if full EV adoption takes longer, the hybrid transition alone provides demand growth.

The EV shunt market is projected to grow at a 32.5% CAGR through 2030 globally. Shivalik entered the shunt business in 2015. Ten years of accumulated knowhow in the fastest-growing segment of precision electronics. Well-timed entry.

7. Global Export Strength

Shivalik earns 56.22% of its revenue from 38 countries outside India. Export share has been steadily rising since FY18. The company established a wholly owned subsidiary in Italy during FY25 to serve European customers directly and navigate geopolitical trade complexity.

Export share grew from 52% in FY18 to 56.22% in FY25.

Sales offices operate in Brazil, the USA, Italy/EU, Russia, Japan, Taiwan, South Korea, and China. These offices track OEM needs before they become competitive tenders.

Shivalik Bimetals Europe SRL was established in Italy during FY25 as a wholly owned subsidiary. Local presence reduces response time and trade friction for EU customers.

In Q3 FY26, shunt revenue from Europe surged 98.64% year-on-year. Bimetal Europe grew 42.04%. Two product segments are gaining EU market share simultaneously.

The US Americas market, hit by tariff uncertainty, is recovering.

Management confirmed on the Q3 FY26 call that Vishay’s US-facing business is in regular supply and expected to return to peak levels in FY27.

Western OEMs are diversifying supply chains away from China under dual-source policies. Shivalik, as India’s only EBW shunt house, is the natural beneficiary.

Export revenue also naturally hedges input costs. Nickel, copper, and manganese are imported and priced in dollars. Dollar export earnings offset this input cost exposure.

Asia (others) shunt revenue in 9M FY26 grew 36.65% year-on-year to ₹45.96 crore. New industrial projects in Vietnam, Thailand, and South Korea are driving this.

8. Swiss Alliance Play

In November 2023, Shivalik signed an MOU with Metalor Technologies of Switzerland to manufacture high-performance electrical contacts in India. Metalor belongs to the Tanaka Group of Japan, one of the world’s foremost materials science firms. This alliance aims to build a third independent revenue pillar alongside bimetals and shunts.

Metalor Technologies is a global leader in precious metal refining and processing. Being part of the Tanaka Group, it sits at the top of the global materials science hierarchy.

Electrical contacts are silver-alloy tips inside switches and relays that enable and interrupt current flow. Shivalik manufactures them via brazing, welding, and cladding.

The contacts segment delivered ₹71.33 crore in FY25 at a 5-year CAGR of 16.26%. It is growing, but the Swiss partnership is designed to accelerate it into a genuinely large segment over the next few years.

Shivalik already acquired full ownership of Checon Corporation (USA) in FY23. Checon was a previous JV partner in contacts technology.

Plant 3 in Solan is dedicated to electrical contacts and carries a stated revenue capacity of ₹300 crore. Current contacts revenue is ₹71 crore.

The PCBA pilot line was initiated in FY25. Per Q3 FY26, PCB assembly development is ongoing alongside the bus bar initiative. Together, these represent Shivalik’s ascent from component maker to sub-assembly provider.

9. Risks and Red Flags

Raw material prices for nickel, copper, and manganese fluctuate with global commodity cycles. Shivalik has pass-through contract clauses, but with a quarterly lag.

Vishay accounts for approximately 40% of shunt resistor revenue. Any slowdown in Vishay’s programmes directly hits Shivalik’s top line. FY25 and 9M FY26 demonstrated this vulnerability when US tariff disruptions cut Vishay’s order volumes.

All three manufacturing plants are located in Solan, Himachal Pradesh. One major landslide, prolonged strike, or power disruption could halt all production simultaneously. No backup facility exists in another Indian geography. A single-site concentration risk.

Thermostatic bimetal technology faces long-term displacement risk from digital temperature sensors and solid-state switches. As digital alternatives become cheaper and more precise, mechanical bimetal switches may gradually lose volume in newer device designs.

The German competitor Isabellenhütte is substantially larger and better-resourced. Shivalik must innovate continuously to maintain its position as the primary global alternative.

Working capital days rose to 265 in 9M FY26 versus 247 in 9M FY25. Receivable days increased by approximately 12 days. If this trend continues, it will compress free cash flow even as profits grow.

The busbar assembly business carries EBITDA margins 8-10 percentage points below core products. At ₹250-300 crore scale, this could dilute consolidated margins unless core product margins simultaneously expand. Investors should track this mix shift quarterly.

US tariff policy remains unpredictable. Americas revenue declined in both bimetals and shunts in Q3 FY26. Any re-escalation of tariffs post the current 90-day pause would stall the US recovery that management is counting on for FY27 growth.

India’s domestic bimetal switchgear revenue declined 6.67% in 9M FY26 and 11.66% in Q3 FY26. The domestic switchgear market has been broadly flat for multiple years.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

This covered almost every aspect! Great work.

thank you for posting such deatiled and key pointers article on shivalik. i was about to analyse it you made my job easier