Shakti Pumps (India) Ltd || Consistently Performing Stocks #61

What has led to the consistency?

Every week I analyze a company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.This week, Let’s explore the business & fundamentals of Shakti Pumps (India) Ltd

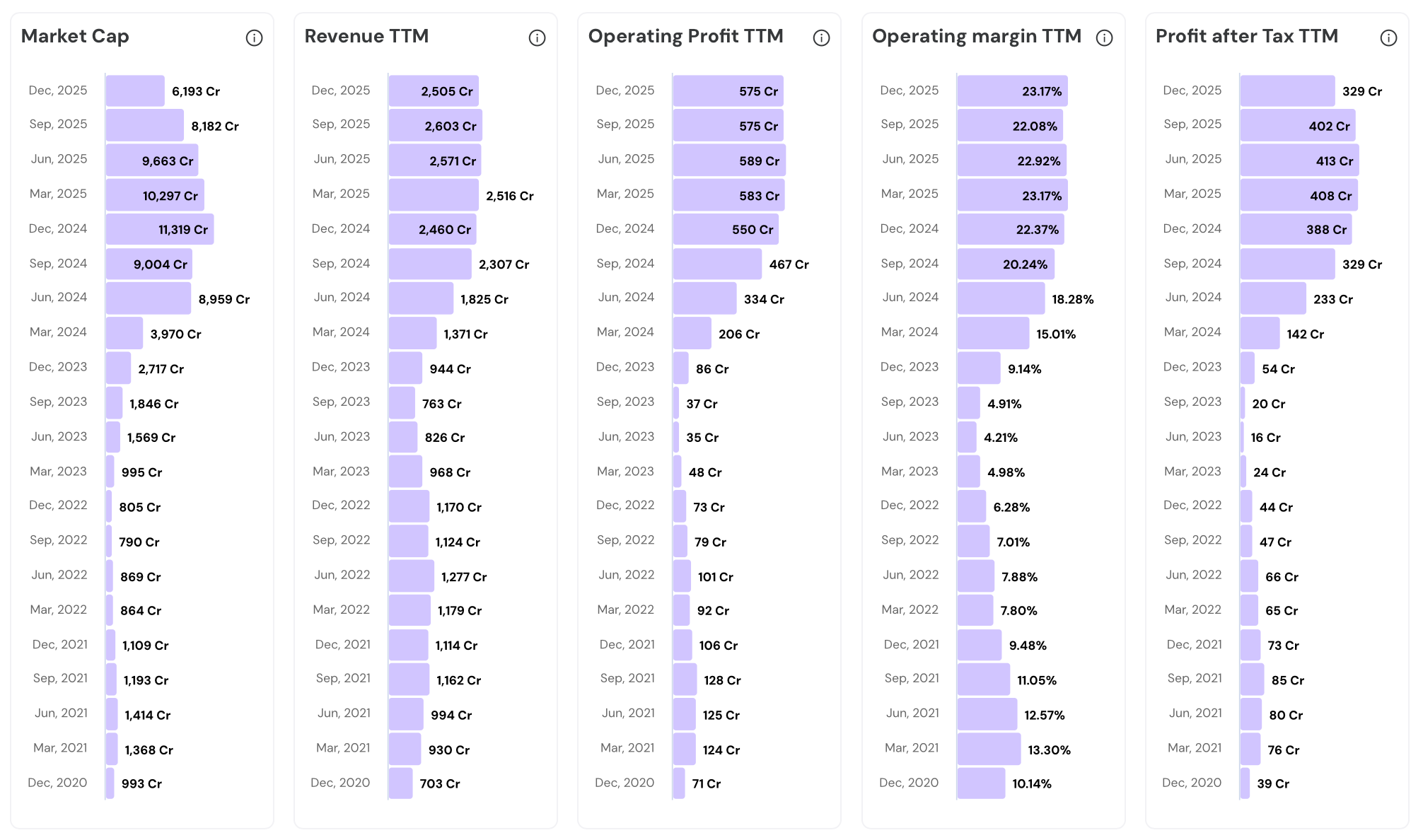

Performance Chart

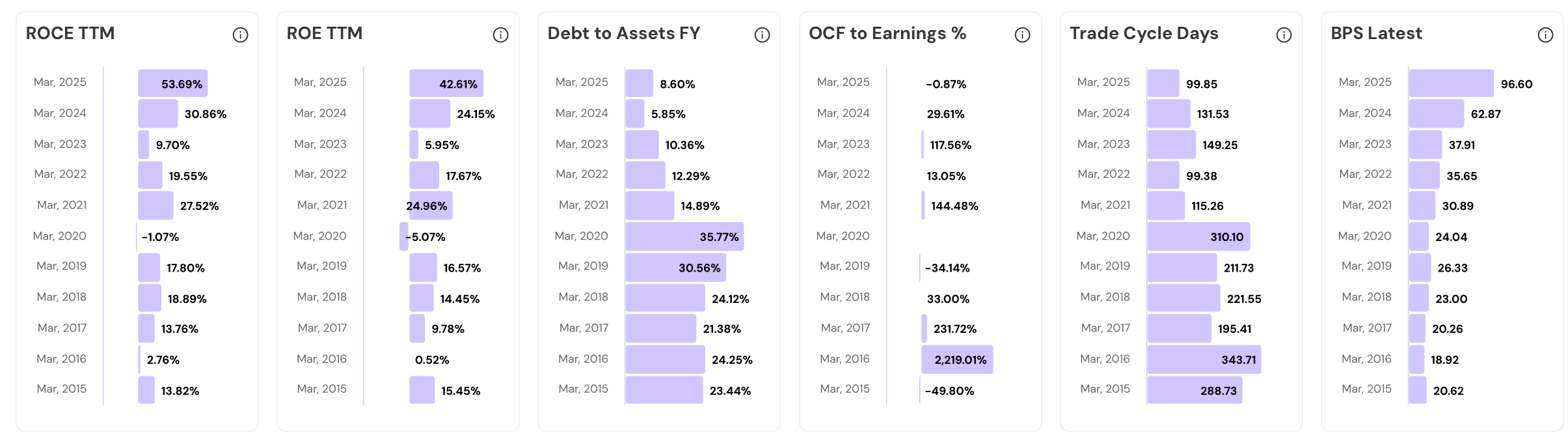

Quality Chart

Their Road to Consistency

1. Overview & Business Model

Shakti Pumps started in 1982 as a small pump workshop in Pithampur, Madhya Pradesh. Today it is India’s largest solar pump manufacturer. Revenue grew from ₹930 crore in FY21 to ₹2,516 crore in FY25, a 37% 5-year CAGR. The company holds 25-30% of PM-KUSUM solar pump installations and exports to 100+ countries.

Founded in 1982 by Manohar Lal Patidar, a farmer from village Rangwasa near Indore. His son Dinesh Patidar took charge in 1986.

In 1996, Shakti launched India’s first 100% stainless steel submersible pumps, solving the corrosion problem that plagued rural irrigation hardware.

The solar pump pivot came in 2013, 6 years before PM-KUSUM scheme launched.

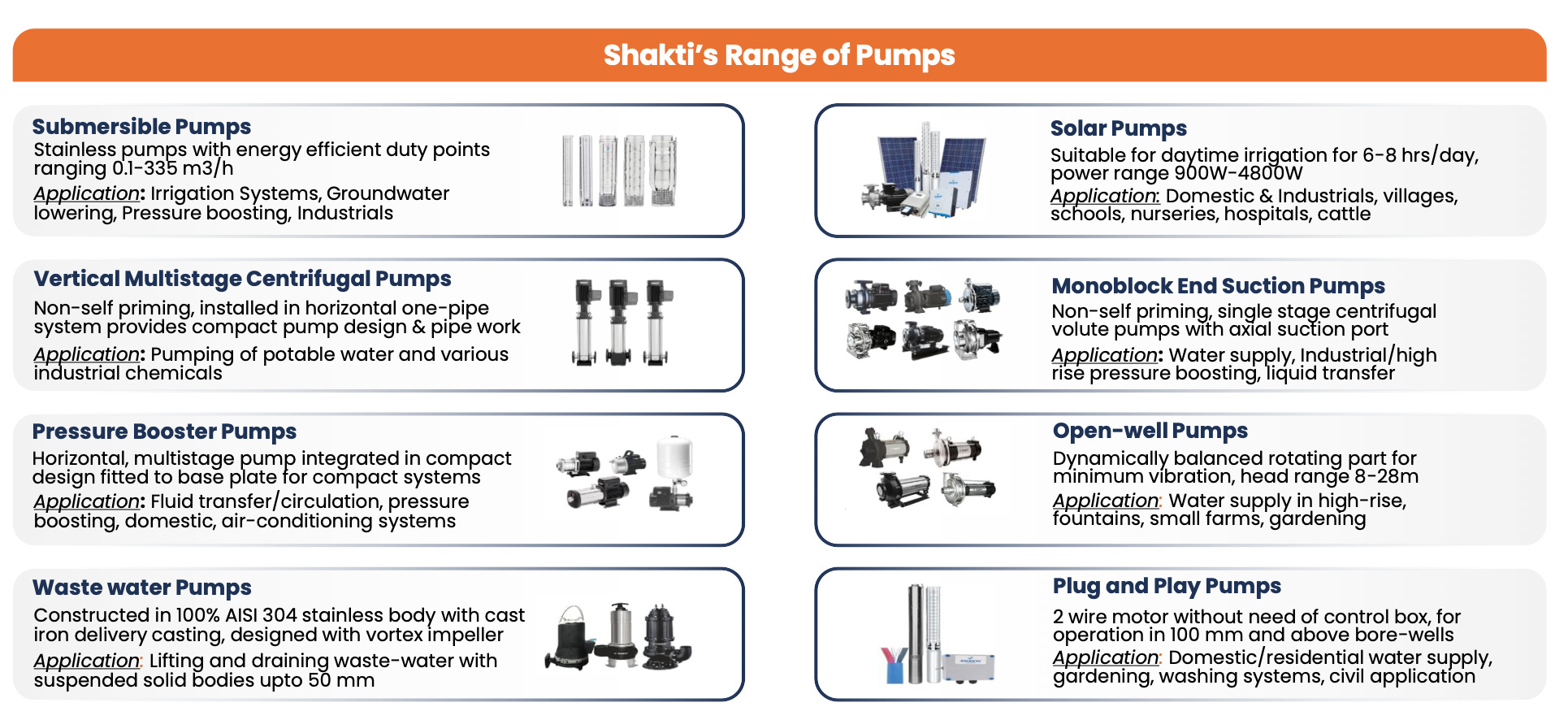

Today the company makes 1,200+ product variants:

submersible pumps from 3” to 12”,

solar systems from 1 HP to 100 HP,

sewage pumps, and

industrial pumps.

Two manufacturing complexes operate in Pithampur. The SEZ unit serves export production, established in 2007. The DTA unit runs multiple specialized sub-plants. Pithampur is the operational spine of the business.

Government projects account for 77% of FY25 revenue, up from 58% in FY21. PM-KUSUM scheme, that we will talk about later, has completely reshaped the revenue mix. This concentration is both the engine and the risk.

Shakti operates through 5 subsidiaries. Shakti Pumps USA LLC, Shakti Pumps FZE Dubai, Shakti Pumps Bangladesh, Shakti Energy Solutions, and Shakti EV Mobility.

The company recently opened 100+ exclusive retail outlets in India as part of its cash sales push.

2. PM-KUSUM Growth Engine

PM-KUSUM is the single largest external catalyst in Shakti’s business. Launched in March 2019 with ₹34,422 crore in central government support, it targets 49 lakh solar pump installations. Shakti holds 25-30% of installations. The order book stands at ₹2,100 crore. And roughly 29 lakh pumps still remain to be installed nationally. The runway is long.

PM-KUSUM Component B funds standalone off-grid solar agricultural pumps. The central government covers 30%, states contribute 30%, and farmers pay 10-40%.

A 5 HP solar pump costs ₹2.5 to ₹4 lakh before subsidies. The farmer pays ₹65,000 to ₹1 lakh after support. Annual diesel savings are ₹40,000 to ₹80,000. Payback arrives in 1-3 years.

Component B has achieved 9.75 lakh installations against a 14 lakh target as of Q3 FY26. FY25 alone saw a 4.2x surge in annual installations. Execution is accelerating.

Roughly 29 lakh pumps remain to be installed nationally across both Component B and C.

FY27 budget allocation is ₹5,000 crore, nearly double the ₹2,600 crore in FY26. PM-KUSUM 2.0 is being planned with an estimated ₹50,000 crore outlay.

Shakti’s state footprint spans Maharashtra, MP, UP, Rajasthan, Haryana, Jharkhand, and now Karnataka.

The Karnataka order in January 2026 was worth ₹654 crore for 16,780 solar pumps. It was Shakti’s maiden entry into southern India.

Dec 2025 alone brought ₹1,152 crore in fresh orders. The order book stood at ₹2,100 crore as of Q3 FY26.

Combined with Component C, around 20.4 lakh farmers have benefited so far against a 49 lakh target. The scheme is still only 50% complete. There is more growth ahead.

3. Manufacturing Depth

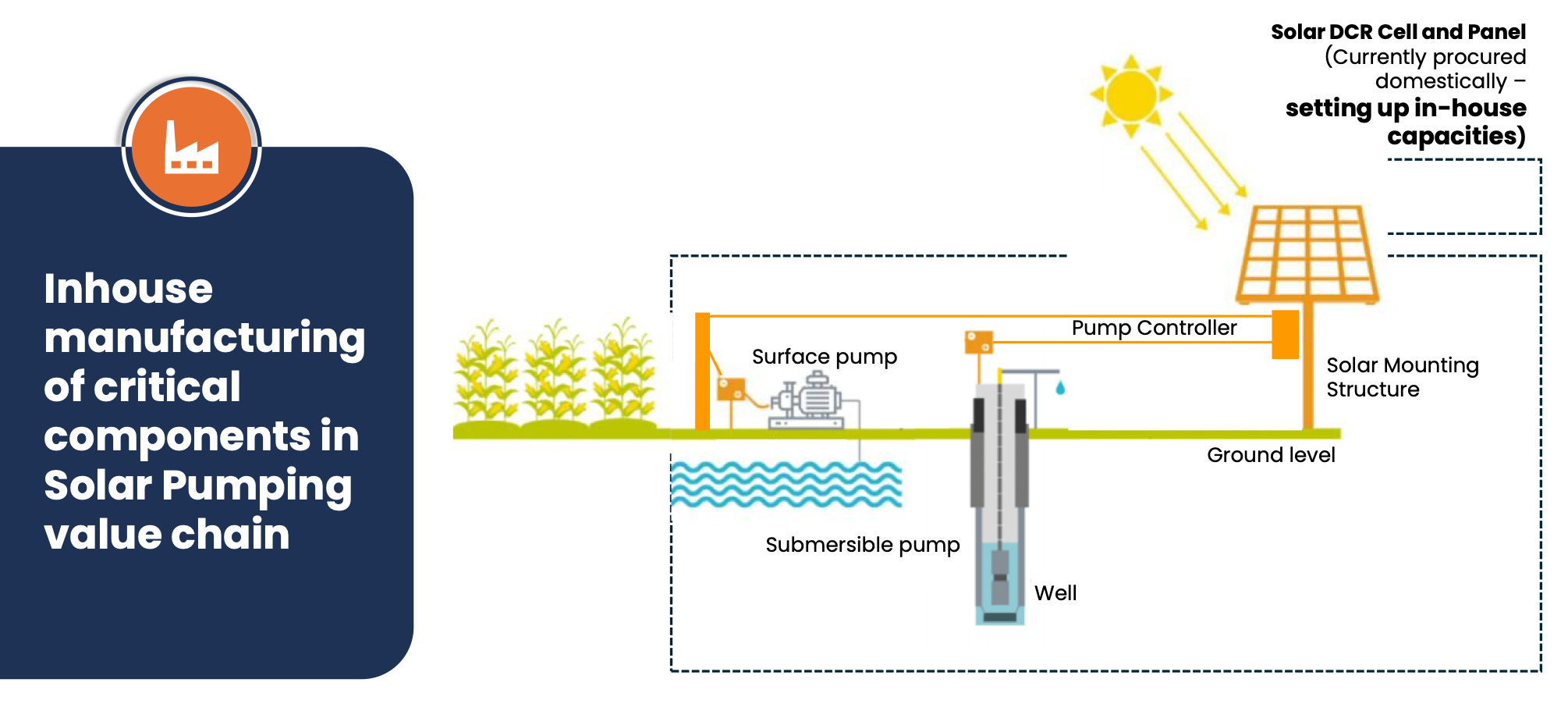

Shakti is the only Indian solar pump manufacturer producing every critical component in-house: pumps, motors, VFDs, solar controllers, and mounting structures. This vertical integration creates an advantageous cost structure. In PM-KUSUM tenders where price is decisive, this integration is Shakti’s most durable competitive weapon.

Most Indian solar pump companies are system aggregators buying components from multiple suppliers. Shakti manufactures the entire system internally.

The Electronics and Control division launched in 2018 to produce VFDs and inverters in-house. These are the most technically complex and the most expensive components in a solar pump system.

In-house VFD production improves margins by 3-4% over third-party procurement. At ₹2,516 crore in revenue, even 3% margin improvement adds roughly ₹75 crore to absolute profits.

Annual production capacity covers 5 lakh pumps and motors, 4 lakh VFDs, and 2 lakh solar mounting structures.

Material costs as a percentage of revenue dropped from 67.1% in 9M FY25 to 62.3% in 9M FY26. Cost reduction due to vertical integration is reflecting in the income statement.

Robotic assembly lines and Mazak-imported machinery run production. Automation reduces dependence on skilled labor and improves output consistency. Less variability in process means fewer defects.

Government tenders are won on price. Shakti’s integrated cost base gives it a structural pricing advantage over CRI Pumps, Lubi Solar, and others relying on third-party component supply.

The integration logic is now extending to solar panels. The 2.2 GW solar cell manufacturing plant will bring module production in-house by Q1 FY27. Panels are 40-50% of total pump system cost.

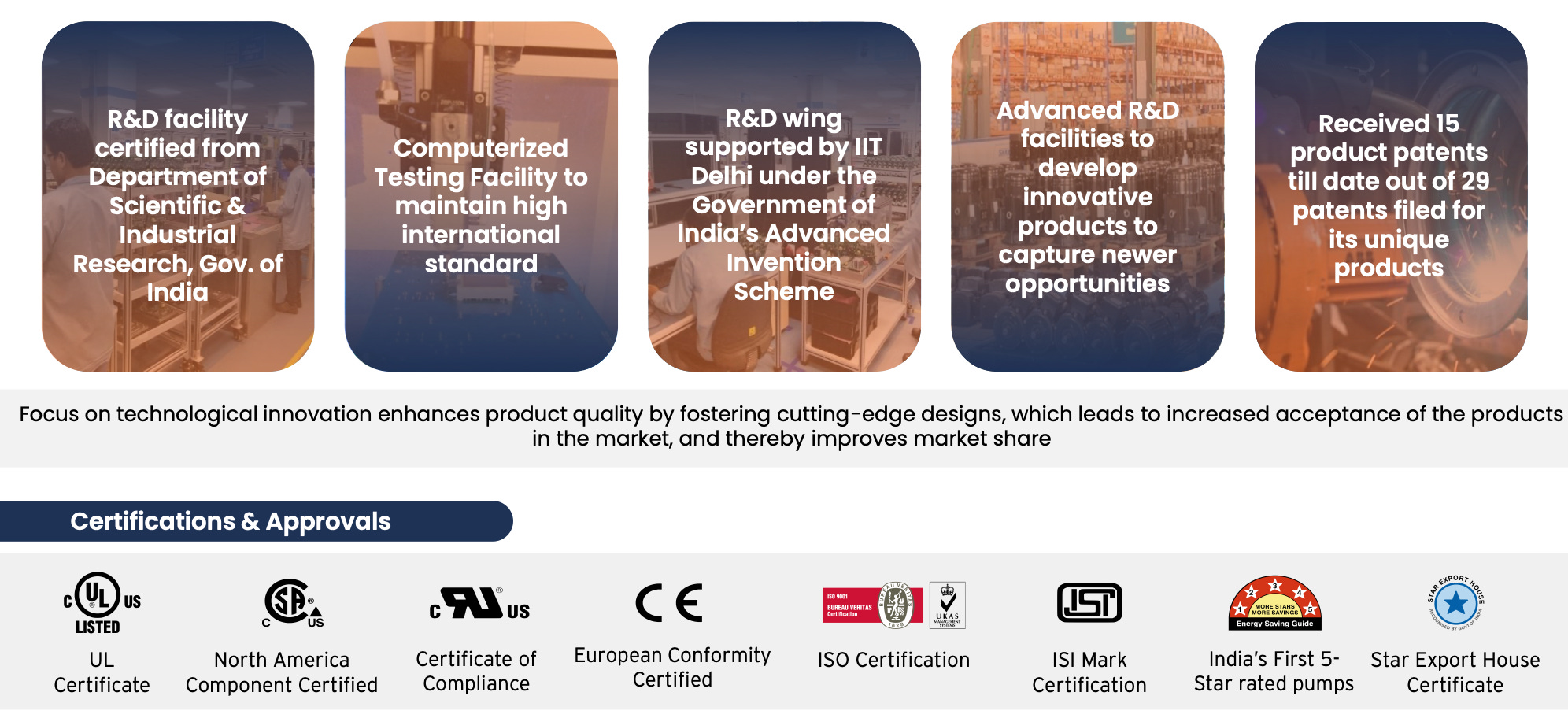

4. Research & Patents

Shakti holds 16 granted patents, with 14 more applications still pending. 7 patents were granted in 2024 alone. The company invests 5-6% of annual revenue in R&D, employs 150+ engineers, and runs active collaborations with IIT Delhi. This IP depth supports competitive differentiation in government tenders, export markets, and premium product pricing.

The Motor Soft Start and Stop patent gradually ramps motor speed, reducing mechanical stress and preventing voltage dips in weak rural grid infrastructure. A practical engineering solution built around real farmer problems.

The Surface Helical Pump patent maintains consistent water flow in reverse osmosis systems even with partially blocked membranes. It targets the industrial water treatment segment, expanding Shakti beyond agriculture.

The Grid-Independent Solar Pump ensures continuous irrigation without any stable grid connection. This directly solves a critical pain point for farmers in remote and off-grid locations.

260+ pump models carry BEE 5-Star energy efficiency ratings, claiming 30-40% lower energy consumption and 40% higher water discharge versus cast iron alternatives.

Chief Technical Officer Dr. Chinmay Jain holds an ME from IISc Bangalore and a PhD in Electrical Engineering from IIT Delhi. He has published close to 20 research papers in IEEE/IET journals and holds 9 patents personally.

MNRE has awarded Shakti its highest 1A performance rating as a channel partner. For PM-KUSUM tenders, this rating is the mandatory entry ticket.

Certifications span ISO 9001, ISO 14001, ISO 45001, CE Mark, UL, and BIS. DSIR recognition is also in place. Each certification strengthens an existing tender bid.

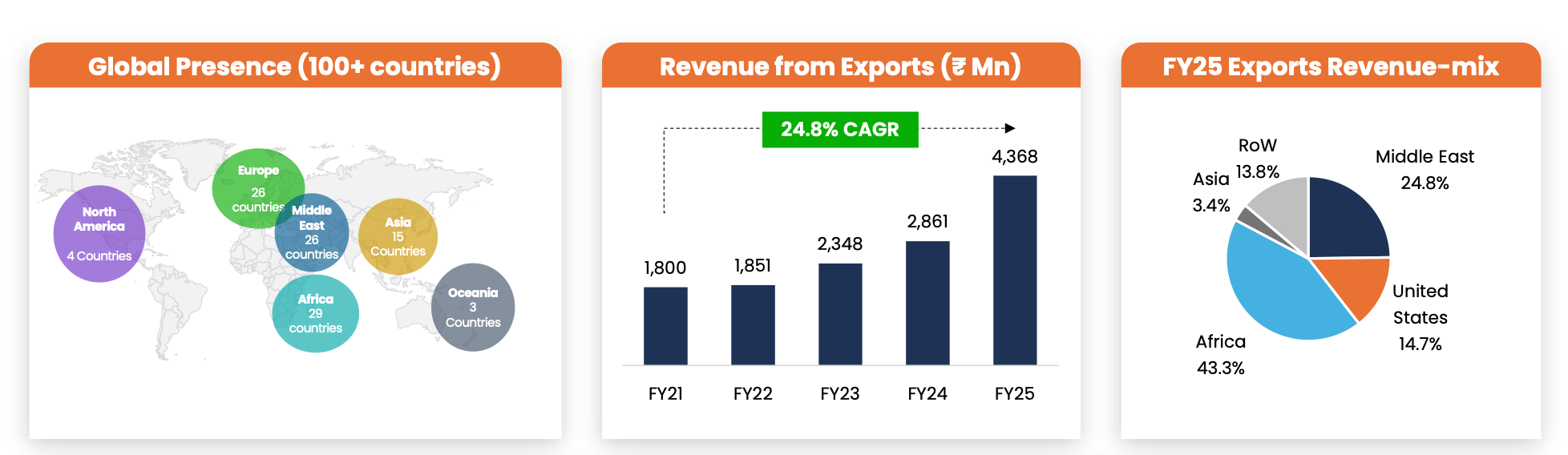

5. Global Export Reach

Export revenue grew 53% in FY25 to ₹437 crore, reaching customers across 100+ countries.

In 9M FY26, exports reached ₹307 crore. Management targets ₹500 crore for the full FY26 year.

Africa contributes 43% of export revenue. Middle East adds 25%. Americas contribute 15%. Asia adds 3%. Geographically diversified.

The Uganda project is Shakti’s most impressive international reference. Valued at $35.3 million and funded by India’s Exim Bank, it supplies drinking water to 500,000 people across 20 rural districts. This is a full EPC project, not just product supply. Engineering, procurement, and construction were all managed by Shakti.

The retail export segment grew over 25% YoY in 9M FY26. Retail exports carry higher margins than government or institutional supply.

Subsidiaries in the USA, Dubai, and Bangladesh enable local market presence and direct customer relationships.

Management has guided 20-25% annual export growth. Exports are being positioned as a counter-cyclical hedge against domestic PM-KUSUM policy risk.

Shakti is a member of the International Solar Alliance (ISA), which has aggregated demand for 2,70,000+ solar pumps across 22 countries, 1 GW of solar rooftop across 11 countries, and 10 GW of solar mini-grids across 9 countries. Pipeline is good.

Marquee international projects include de-watering at Burj Khalifa and One Za’abeel Tower in Dubai.

6. Solar Cell Factory Bet

Shakti is investing ₹1,200 crore through subsidiary Shakti Energy Solutions to build a 2.2 GW solar DCR cell and PV module manufacturing plant on 113 acres in Pithampur.

PM-KUSUM mandates the use of domestically manufactured solar cells in all installations. Shakti currently sources panels from Premier Energies and Adani Mundra Solar. The new plant is aiming to reduce this dependency.

The 2.2 GW plant sits on 113 acres in Pithampur, being built through subsidiary Shakti Energy Solutions Limited.

Solar cell production using solar wafers began in March 2025. Full-scale module manufacturing is targeted for Q1 FY27.

The total capex plan is ₹1,700 crore. ₹1,200 crore for the solar plant, ₹250 crore for doubling pump capacity from 5 to 10 lakh units per year, and ₹250 crore for the EV facility.

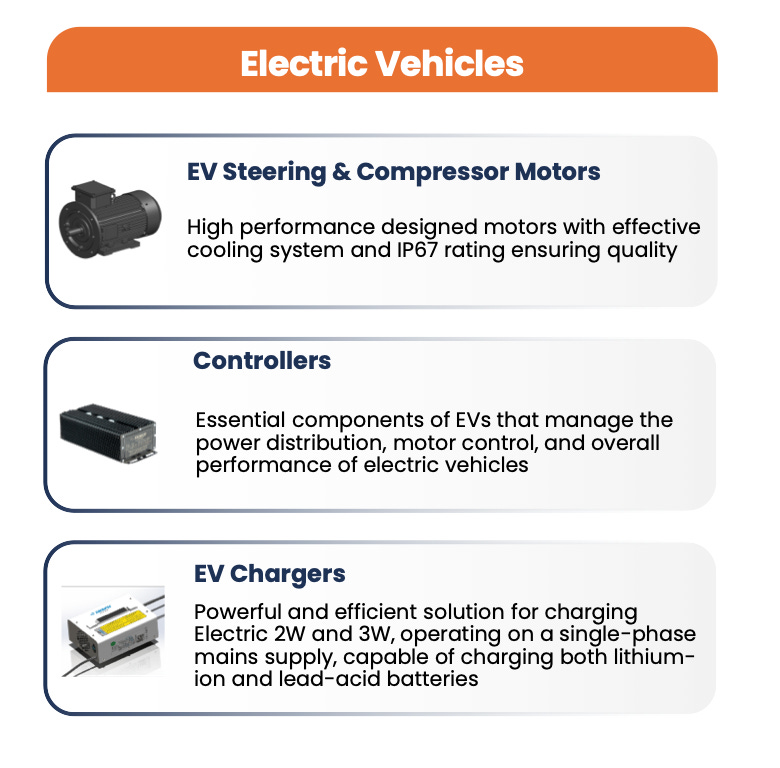

7. EV Mobility Entry

Shakti EV Mobility is manufacturing electric motors, controllers, and chargers for two- and three-wheelers. Annual capacity is set at 2 lakh units for each component. The Indian EV industry is projected to grow at 49% annually through 2030.

Emerging business revenues, which include EV components, grew from ₹39.6 Cr in 9M FY25 to ₹66.6 Cr in 9M FY26, a 68% YoY increase. Early numbers, but the direction is clear.

The EV plant capacity is 2 lakh motors, 2 lakh controllers, and 2 lakh chargers per year. All the 3 product lines are technical extensions of manufacturing capabilities Shakti already runs at scale for solar pumps.

Shakti’s motor and VFD manufacturing expertise also transfers directly to EV powertrains.

Shakti has already supplied initial electric motor orders to JBM, one of India’s leading EV bus and commercial vehicle manufacturers. Trials are ongoing with multiple additional OEMs beyond JBM.

The EV capex requirement is ₹250 crore. Compared to the ₹1,200 crore solar plant, this is a smaller and more measured bet.

India’s two- and three-wheeler EV segment is leading national adoption. Component demand from domestic OEMs will grow proportionally. The timing of Shakti’s entry aligns with the steepest part of that adoption curve.

This segment does not replace PM-KUSUM revenue. It creates a second revenue stream on a different policy and demand cycle. If PM-KUSUM slows, EV revenue offers a partial but meaningful structural buffer.

8. Competition

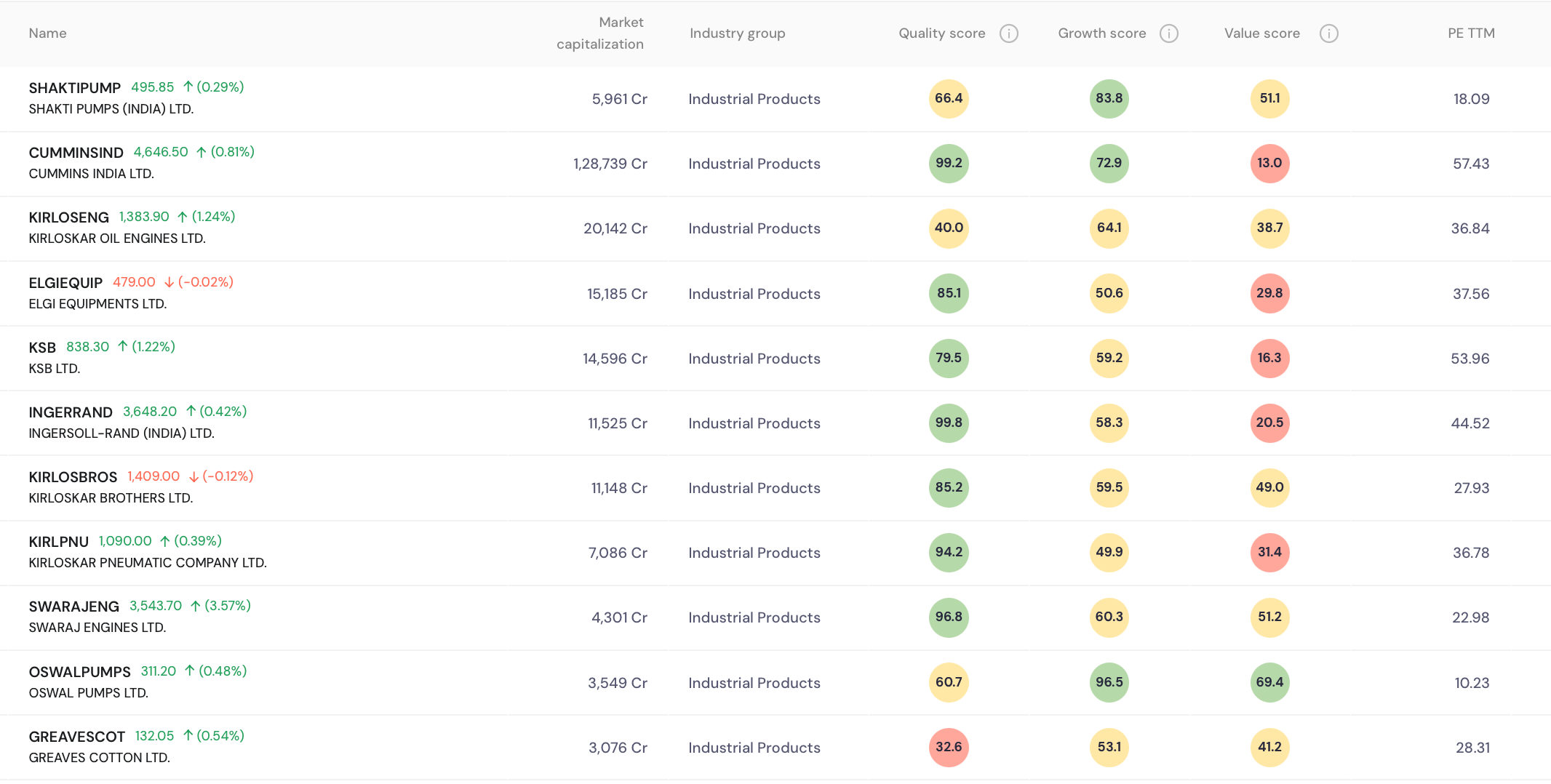

The Indian pump market is valued at $3 billion and grows at 5-7% annually. The solar sub-segment is projected to expand from $600 million in 2024 to USD 2.4 billion by 2029. Shakti competes with Kirloskar Brothers, KSB India, CRI Pumps, Tata Power Solar, and Lubi Solar. In the PM-KUSUM solar segment specifically, it leads the field by a visible margin.

India has 4% of global freshwater for 18% of the global population. Water scarcity is real. Solar pumps replacing diesel irrigation it is becoming a necessity.

Kirloskar Brothers has ₹4,404 crore in revenue versus Shakti’s ₹2,516 crore. But Kirloskar’s 5-year revenue CAGR is 7.5%. Shakti’s is 37.3%.

KSB India operates at EBITDA margins of 14-15%. Shakti’s FY25 margin is 24%. The gap is explained by solar pump product mix and backward integration.

CRI Pumps, Tata Power Solar, Lubi Solar, and Ravindra Energy all participate in PM-KUSUM. None of them combine Shakti’s integration depth with its MNRE 1A certification status.

In retail and export markets, Grundfos and Kirloskar carry stronger institutional brand equity. Shakti’s competitive moat is only concentrated in the government solar pump procurement channel.

The solar pump market is expected to reach USD 2.4 billion by 2029 from USD 600 million in 2024. Four times growth in five years. Abhi, opportunity ahead.

9. Risks and Red Flags

Government projects account for 77% of FY25 revenue. Any PM-KUSUM budget cut, subsidy reduction, or policy reversal would hit Shakti directly and hard.

Despite ₹408 crore in reported PAT for FY25, operating cash flow was negative. Accounting profits and actual cash generation are dangerously disconnected.

Receivables stood at ₹1,049 Cr by FY25. Debtor days is at 152. Over 22% of receivables have aged beyond 180 days. Mainly because the company deals with government and state agencies.

Working capital loans surged to ₹570 crore by September 2025, up from ₹132 crore in FY24. The company is financing government payment cycles using its own balance sheet.

Q3 FY26 saw PAT fall 70% YoY to ₹32 crore. EBITDA margins compressed to 10.7% from 23.8% a year earlier.

SEBI fined 8 entities linked to the Patidar family ₹22 lakh in December 2022 for insider trading. Designated employees traded without pre-clearance and made contra trades.

Promoter holding has declined from 55.9% in 2022 to 50.3% today due to QIP dilution. Further QIPs to fund capex could push holdings below the psychologically significant 50% threshold.

Raw material costs, specifically copper, steel, and solar panels, rose 2-4% in FY26. Input inflation makes margin defense harder.

The 2.2 GW solar plant enters a globally oversupplied panel market. If module prices continue falling by Q1 FY27, the projected 3-4% margin gain from in-house production may prove less than expected.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.