Piccadily Agro Industries Ltd || Consistently Performing Stocks #67

What has led to the consistency?

Every week I analyze a company’s fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.

This week, Let’s explore the business & fundamentals of Piccadily Agro Industries Ltd (NSE: PICCADIL)

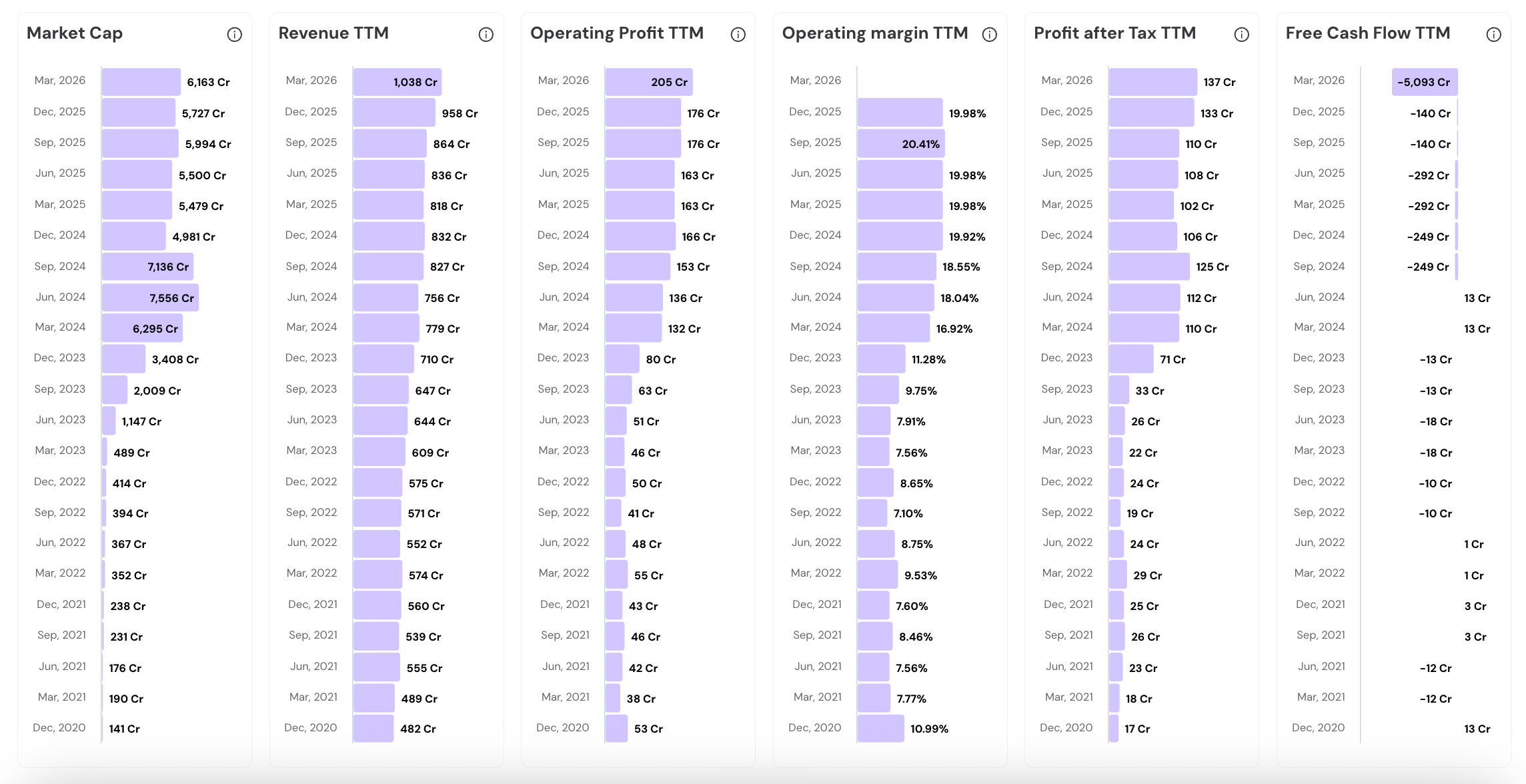

Performance Chart

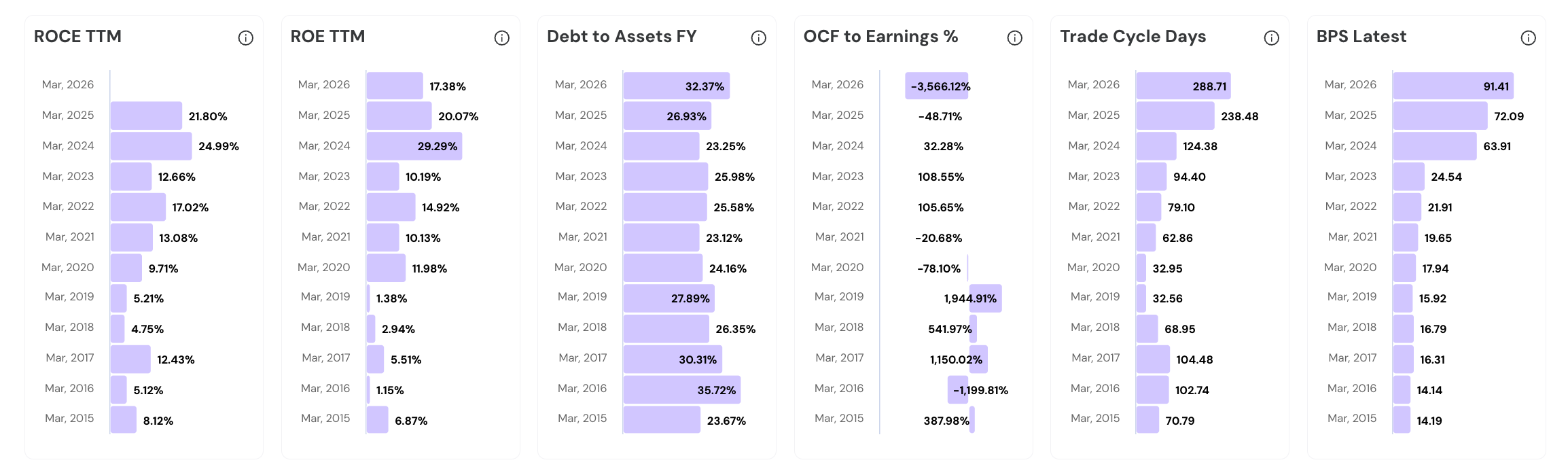

Quality Chart

Their Road to Consistency

1. Overview and Business Model

Piccadily Agro Industries Limited started as a sugar mill in Indri, Haryana, in 1994. Over three decades, it transformed into India’s fastest-growing premium spirits company. Two segments drive revenue today: the distillery (79% of revenue in FY26) and sugar (20.5%). The transformation from commodity to luxury is the core narrative here.

The company was founded in 1994 and listed on BSE the same year. It began as a pure sugar unit. Nobody, including the founders, likely imagined it would end up competing with Scotch whisky.

The first strategic pivot came in 2007. Management added a 78 KLPD distillery next to the sugar mill. Ethanol and Extra Neutral Alcohol were the original targets.

A 12 KLPD malt plant was installed in 2010. Barrels were procured for spirit maturation.

By 2014, multiple IMFL companies were buying Piccadily’s matured malt for their own products. External validation of liquid quality confirmed what management already suspected.

Indri single malt launched officially in 2022. It grew from 15,000 cases in FY23 to over 100,000 cases in FY24. A 6x jump in two years.

The portfolio today has four brands: Indri (single malt), Camikara (aged pure cane rum), Cashmir (vodka, launched May 2025), and Whistler (blended whisky). Each targets a distinct premium consumer segment.

FY26 total income reached ₹1,143 Cr versus ₹893 Cr in FY25, a 28% jump. Distillery contributed ₹902 Cr. Sugar contributed ₹233 Cr. The mix is moving further toward spirits every year.

Total distillery capacity today is 450 KLPD across Indri (220 KLPD ENA/ethanol + 30 KLPD malt) and Chhattisgarh (200 KLPD). This puts the company among India’s largest independent distillery operators.

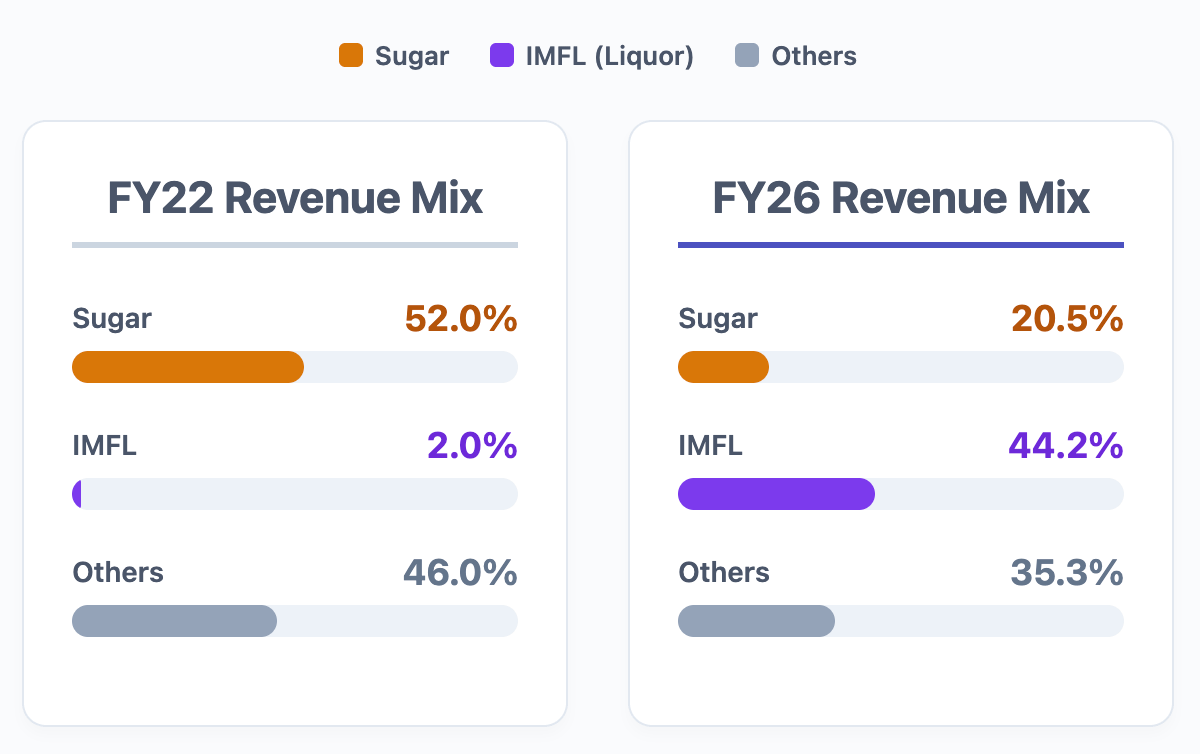

The revenue mix in FY22 was 52% sugar and just 2% IMFL. By FY26, sugar fell to 20.5% and IMFL rose to 44.2%. It is a complete structural rebuild of the business.

The company sells in 29 Indian states, 29 countries, and 30 duty-free outlets globally. From a small Haryana sugar mill to a global spirits brand in under three decades.

2. Indri Brand Power

Indri has become India’s largest-selling single malt and one of the fastest-growing premium whisky brands globally. It outsold Glenfiddich and Glenlivet in India in 2024 and entered Tesco in the UK.

Indri sold 2.04 million bottles (1,70,000 nine-liter cases) in calendar year 2024. It outsold both Glenfiddich and Glenlivet in the Indian market that year.

Indri Diwali Collector’s Edition won the World’s Best Whisky Award in both 2023 and 2025.

The IWSR ranked Indri the number one malt whisky in India in 2025. It beat global and domestic heavyweights by a clear margin. International ranking bodies rarely crown emerging-market brands.

Indri is currently among the top 15 single malt brands globally. Management targets top 10 within one to two years and top 5 within three to five years.

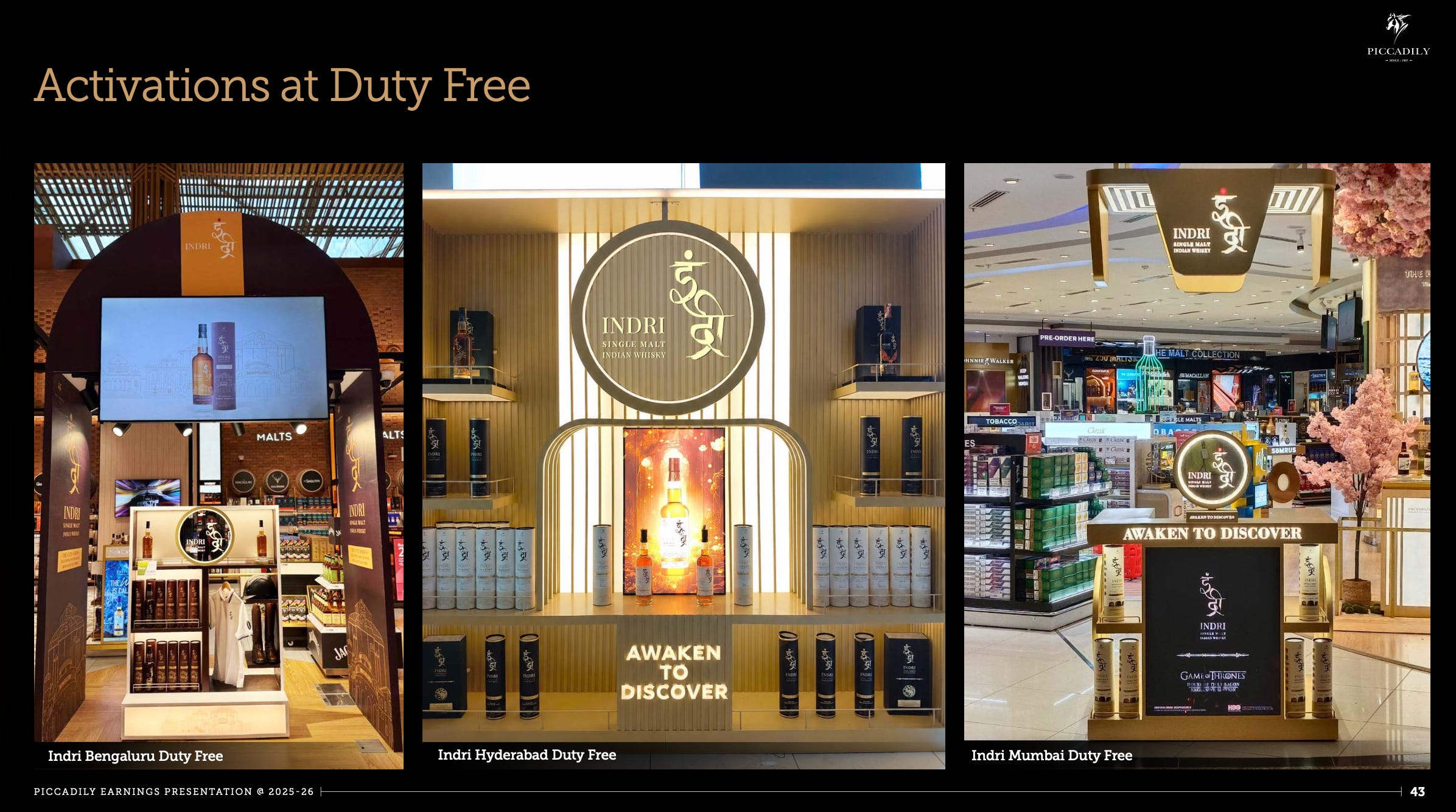

The City Series was designed as travel retail exclusives. Bengaluru came first, then Dubai and Mumbai. Each release is a collector’s item tied to a city’s identity. Scarcity and storytelling driving premium pricing.

Indri entered 79 Tesco stores in the UK in 2024, targeting mainstream British consumers, not just niche whisky enthusiasts.

The brand is available in 30+ US states with Costco and Total Wine as retail partners. Costco is the world’s largest spirits retailer.

Indri grew 16% in FY26 due to supply constraints. Management confirmed capacity has now been resolved.

3. Climate Maturation Advantage

Indri’s location in the Himalayan foothills creates a scientifically documented production edge. Temperatures swing from near-zero in winter to 50 degrees Celsius in summer. This extreme variation accelerates the interaction between spirit and wood, achieving in four to six years what takes twelve in Scotland.

The sub-tropical climate causes barrels to expand in summer heat and contract in winter cold far more violently than in Scotland. Each cycle, pulls flavor compounds from the wood faster. This is free production acceleration.

Indri Trini uses three distinct cask types simultaneously: ex-bourbon American oak, ex-French wine casks, and Pedro Ximenez sherry casks. Triple-cask maturation was an Indian first. The flavor complexity this creates is distinctive.

Barrel inventory stood at 83,800 units as of March 2026, up from 45,000 in FY24. The company is scaling to 100,000 barrels by end of FY27.

Six-row barley sourced directly from Rajasthan and Haryana farmers provides a higher protein content than four-row barley used by most Scotch distilleries. Grain selection shapes the liquid’s flavor character.

Piccadily holds the largest independent malt warehousing capacity in India as of 2025. Over 10 million liters of spirit currently ages across its warehouses.

Camikara aged rum matures 8 to 12 years in American oak with no added sugar or artificial color.

12 new warehouses were added to the Indri site recently to handle the growing barrel count.

No bulk malt is sold to any third party. Every barrel ages exclusively for own-brand bottling. This discipline ensures the company captures the full retail margin of every aged liter it produces.

4. Rapid Capacity Expansion

Piccadily committed ₹1,000 Cr over three years to nearly quadruple production and maturation capacity across multiple locations. Both plants were completed within budgeted cost estimates. The heavy capex phase is now over. FY27 is the first full year of monetizing this infrastructure.

The Indri distillery expansion was completed in October 2025. ENA and ethanol capacity grew from 78 KLPD to 220 KLPD. Malt capacity grew from 12 KLPD to 30 KLPD. Both expansions were on schedule and on budget.

The Chhattisgarh greenfield distillery in Mahasamund was commissioned in December 2025 with 200 KLPD capacity. Its first commercial sales began in May 2026. Management expects ₹300 Cr to ₹400 Cr in FY27 revenue from this plant alone.

Total distillery capacity now stands at 450 KLPD: 30 KLPD malt and 420 KLPD ENA/ethanol. This positions Piccadily as one of the largest independent distillery operators in India. Scale creates both cost and negotiation power.

The Indri expansion alone should generate ₹250 Cr to ₹300 Cr in additional FY27 revenue. Combine that with Chhattisgarh’s ₹300 Cr to ₹400 Cr. Together, that is ₹550 Cr to ₹700 Cr of incremental revenue in a single year.

FY27 capex guidance is only ₹25 Cr to ₹30 Cr. After three years of heavy investment, the company enters a low-capex, high-monetization phase. Cash generation should accelerate significantly from FY27 onward.

The Scotland distillery at Portavadie spans 58 acres. Land is purchased, licenses are in place, and UK government approvals are received. Construction is underway. This will produce Scotch-style single malt.

Barrel storage is scaling from 83,800 barrels to 100,000 barrels by FY27. The incremental capex is modest.

Management has guided 3x to 4x revenue growth over the next three to four years. The capacity to achieve this is now physically in place. Execution and distribution are the only things left.

5. Portfolio Mix Shift

Piccadily is engineering a structural shift from cyclical, low-margin sugar toward high-margin IMFL brands. The numbers make this shift visible across every year. Each percentage point of IMFL in the revenue mix is a direct lift in blended EBITDA margin.

As pointed out earlier Sugar was 52% of revenue in FY22. It is 20.5% in FY26. IMFL was 2% in FY22. It is 44.2% in FY26.

Distillery EBITDA margin was 31.5% in FY26, up 130 basis points from FY25. IMFL alone operates at 45% to 50% EBITDA margins. Sugar’s EBITDA margin was negative 4.6%. The contrast explains the profitability trend.

Overall EBITDA margin held at 23.4% in both FY25 and FY26, despite a 28% jump in revenue.

Branded IMFL revenue grew from ₹150 Cr in Q4 FY25 to ₹250 Cr in Q4 FY26, a 67% jump YoY.

Whistler blended whisky grew 98% in volume in FY26 after a full rebranding. Whistler at ₹1,500 to ₹2,500 price points opens a different mass-premium consumer segment.

IMFL’s share of distillery revenue was 38.1% in Q4 FY26 versus 26.8% in Q4 FY25. Even within the distillery segment, the premium IMFL slice keeps growing quarter on quarter.

FY27 guidance: 60% to 70% total Alco-Bev revenue growth, primarily driven by IMFL. In absolute terms, the company is guiding toward ₹1,400 Cr to ₹1,500 Cr in Alco-Bev revenue.

New premium and luxury product launches are planned across existing and new categories in FY27. Management explicitly said these launches are not included in the 60% to 70% guidance.

6. Expanding Distribution Network

Piccadily grew its domestic retail footprint from 6,700 outlets in FY23 to 25,000+ in FY26. International distribution expanded from under 20 countries to 29. This distribution infrastructure investment mirrors the production scale-up.

The company now operates across 29 Indian states and union territories including the CSD channel. Moving from 20 states in FY25 to 29 in FY26 is meaningful. Each new state adds a compounding revenue layer.

On-trade distribution through bars, restaurants, and hotels grew over 50% in FY26. On-trade visibility among younger consumers drives at-home demand.

IMFL revenue mix: CSD and paramilitary 30%, exports 25%, and domestic trade 45%. Management targets 50% export share within three to five years. At 45% to 50% EBITDA margins in IMFL, the export shift would accelerate profitability.

Indri is available in most A-category retail outlets across operating states. A-category outlets are the only relevant shelf for a single malt priced above ₹3,000 to ₹4,000.

The brand entered 79 Tesco stores across the UK in 2024. Tesco reaches mainstream British shoppers, not niche whisky collectors. Mainstream shelf in Tesco signals the brand has crossed from specialist to accessible premium globally.

Indri is now in 30+ US states with Costco and Total Wine as retail partners. Costco is the world’s largest spirits retailer. Total Wine is the largest specialty retailer. Both in one year of serious US push. Impressive.

Travel retail now spans 30 duty-free outlets globally. The City Series expressions were designed specifically for this channel. High-net-worth travelers buying ₹10,000 to ₹30,000 bottles are the highest-margin IMFL customers available.

Management is deploying experiential marketing: curated whisky dinners, tasting events, and trade education sessions in key global cities. These generate brand advocacy from industry influencers at far lower cost than traditional advertising.

The distribution target is 30,000+ domestic retail outlets and a 50% export revenue mix in three to five years. Both are directionally consistent with the brand’s current trajectory.

7. Demerger Value Unlock

The board approved the sugar business demerger into a new entity called Piccadily Food and Essential Limited in April 2026. The scheme has been filed with SEBI. Upon completion, Piccadily Agro becomes a pure-play premium alco-bev company. Shareholders receive one share of the new sugar entity for every nine shares held.

KPMG is the demerger advisor. After SEBI clearance, the scheme goes to NCLT for court approval. Management expects the entire process to be completed within FY27. A clear roadmap for a structurally cleaner balance sheet.

Sugar contributed 20.5% of total revenue in FY26 but posted a negative 4.6% EBITDA margin. Removing sugar eliminates a structural margin drag.

Pure-play consumer premium companies trade at significantly higher valuation multiples than diversified conglomerates. Post-demerger, institutional investors focused on alco-bev can enter the Piccadily story with a clean single-business lens.

Sugar is cyclical and heavily regulated. Cane prices are set by the central government. Selling prices are state-controlled. Separating sugar makes the remaining spirits business far more predictable in its earnings profile.

Post-demerger, 100% of management bandwidth, human capital, and financial resources will focus on Indri, Camikara, Cashmir, and Whistler.

The 1:9 share swap ensures no forced exit for any investor. Shareholders retain upside in both the high-growth spirits entity and the sugar company being given its own independent listed identity. Value preserved both ways.

Management described the demerger as separating a traditional heritage business to give it its own identity. This framing shows intent to list and run the sugar business as a serious standalone.

The timing of the demerger is deliberate. Spirits now dominate revenue. Executing the demerger at this inflection point maximizes the valuation extraction for both entities.

Inorganic acquisitions are also being explored, primarily on the brand side of Alco-Bev. Management confirmed they are in discussions.

8. Integrated Supply Chain and Management

Piccadily controls the supply chain from barley farm to retail bottle and has simultaneously upgraded its leadership bench from commodity industry executives to global spirits professionals.

Alok Kumar Singh was appointed VP Manufacturing and Supply Chain in FY26, joining from Pernod Ricard. Pernod manages the most complex premium spirits operations in the world. That experience now inside Piccadily is significant.

M.S. Venkatesh joined as CHRO with prior experience at Hindustan Unilever, Coca-Cola, Bharti Airtel, and Caterpillar. A cross-sector FMCG and manufacturing background for a company scaling toward thousands of employees rapidly.

SAP-based ERP systems were deployed across operations in 2025. With 85,000 aging barrels across two states and 25,000+ retail touchpoints, data integrity is non-negotiable. This system lays the governance foundation for global scale.

The co-generation plants run on bagasse from the sugar unit, generating captive electricity for the entire Indri manufacturing complex. This self-generated power reduces utility costs and grid dependence.

A PET bottle manufacturing unit in Telangana produces bottles for country liquor and blended brands. Owning packaging for high-volume products gives direct cost control and quality consistency at the lower end of the product portfolio.

Barley is sourced directly from farmers in Rajasthan and Haryana. Six-row barley from this region has higher protein content than the four-row variety used by most Scotch distilleries. Procurement specificity creates a raw material moat.

The Chhattisgarh plant was sited near grain sources to minimize logistics costs. The state offers regulatory incentives for distillery investment. Location decisions at greenfield stage compound into cost advantages for decades.

The integrated model from grain sourcing to barrel maturation to bottling to distribution gives full quality visibility at every step. Indri’s 104 awards across three years show what that full-chain control produces consistently.

Management guidance for absolute EBITDA growth tracks the 60% to 70% revenue growth guidance. The claim is that EBITDA margins will either hold or improve 50 bps as premium product mix deepens.

9. Risks and Red Flags

Promoter background is the most discussed concern. Venod Sharma, linked to the promoter family, is a politically connected Haryana figure. His son Manu Sharma was convicted in the Jessica Lal murder case. Reputational association risk is real even if operationally separate.

Short-term borrowings jumped 132% in FY26, driven by higher IMFL debtor balances and ₹100 Cr in additional malt inventory. This is growth-linked, not distress-linked. But cash cycle stretch at high-growth rates warrants ongoing monitoring.

DSO (Days Sales Outstanding) across the IMFL business is 80 to 90 days. Government and CSD channels pay slowly. As IMFL revenue scales toward ₹800 Cr to ₹1,000 Cr in FY27, debtors will grow proportionally before improving.

Glass and packaging material prices rose 40% to 50% due to supply disruptions linked to the Iran conflict. Current vendor arrangements provide short-term cover. Medium-term inflationary risk on packaging costs remains open.

Indri grew only 16% in FY26, well below the 25% to 30% market expectation. Management cited supply constraints, now resolved. But the question of whether demand can absorb much faster growth at ₹4,000+ price points deserves continued scrutiny.

The sugar demerger requires SEBI and NCLT approvals. Indian regulatory timelines are difficult to predict. Any delay pushes the pure-play valuation re-rating story into FY28. Investors pricing this in as FY27 catalyst should be careful.

A trademark dispute with Radico Khaitan over the vodka name Kashmyr resulted in an injunction in Piccadily’s favor. Future disputes could similarly distract leadership.

The Scotland distillery is still under construction with commissioning expected in FY27 or FY28. Any cost overruns or UK regulatory complications could delay the international positioning narrative.

That’s it for today.

FINVEZTO.COM | One Wealth Building System. For Life.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. We do not recommend buying or selling stocks mentioned in this newsletter. Securities market investments carry market risks. Kindly review all related documents before investing.