Lumax Auto Technologies || Consistently Performing Stocks #63

What has led to the consistency?

Every week I analyze a company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.

This week, Let’s explore the business & fundamentals of Lumax Auto Technologies Ltd. NSE: LUMAXTECH

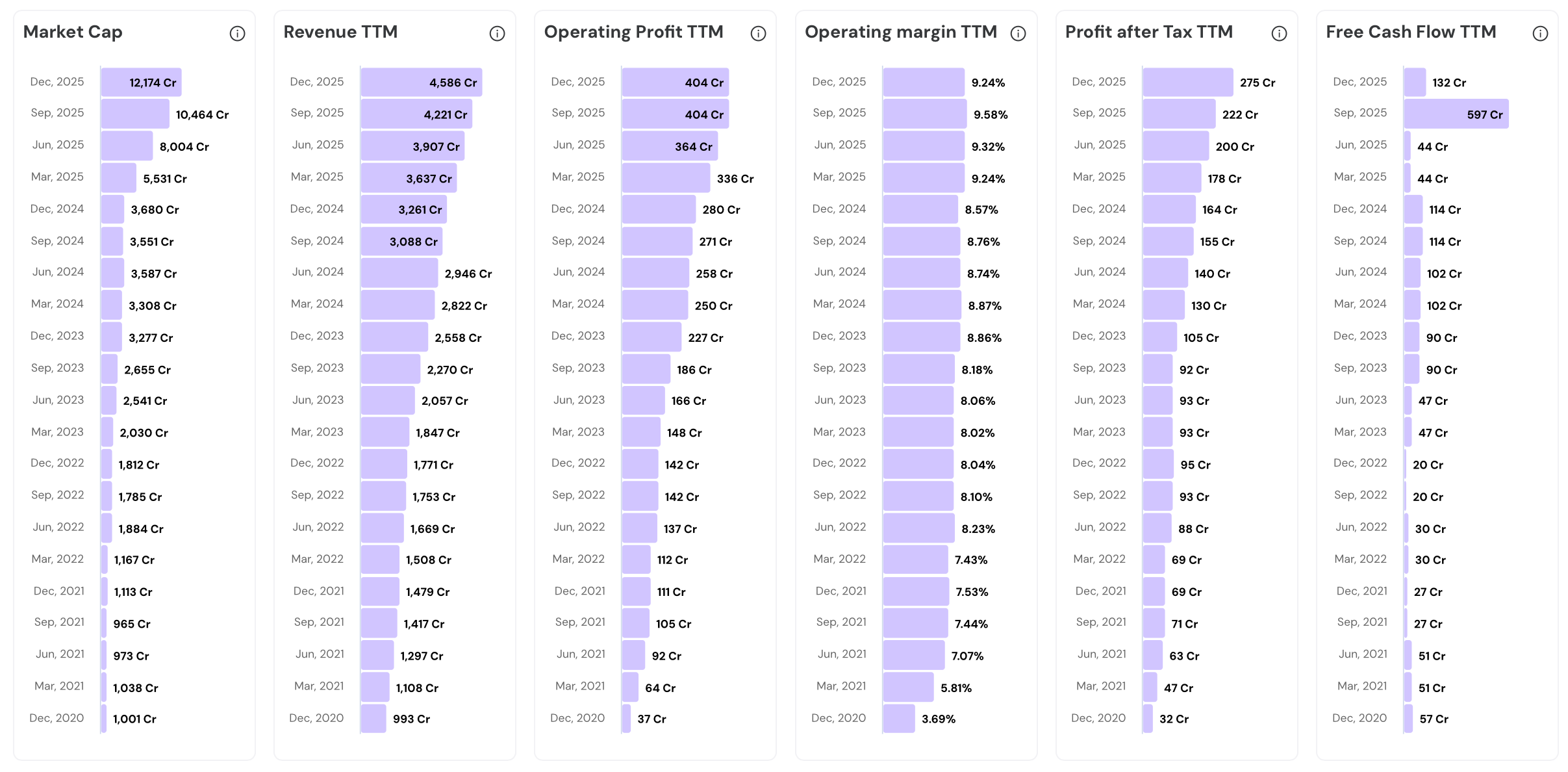

Performance Chart

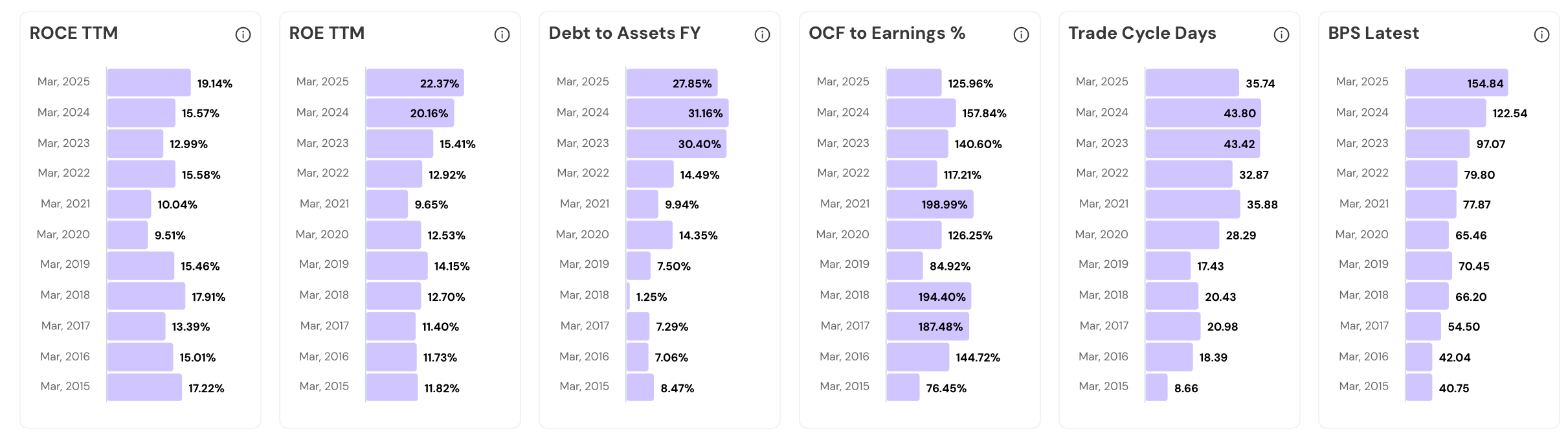

Quality Chart

Their Road to Consistency

1. Overview and Business Model

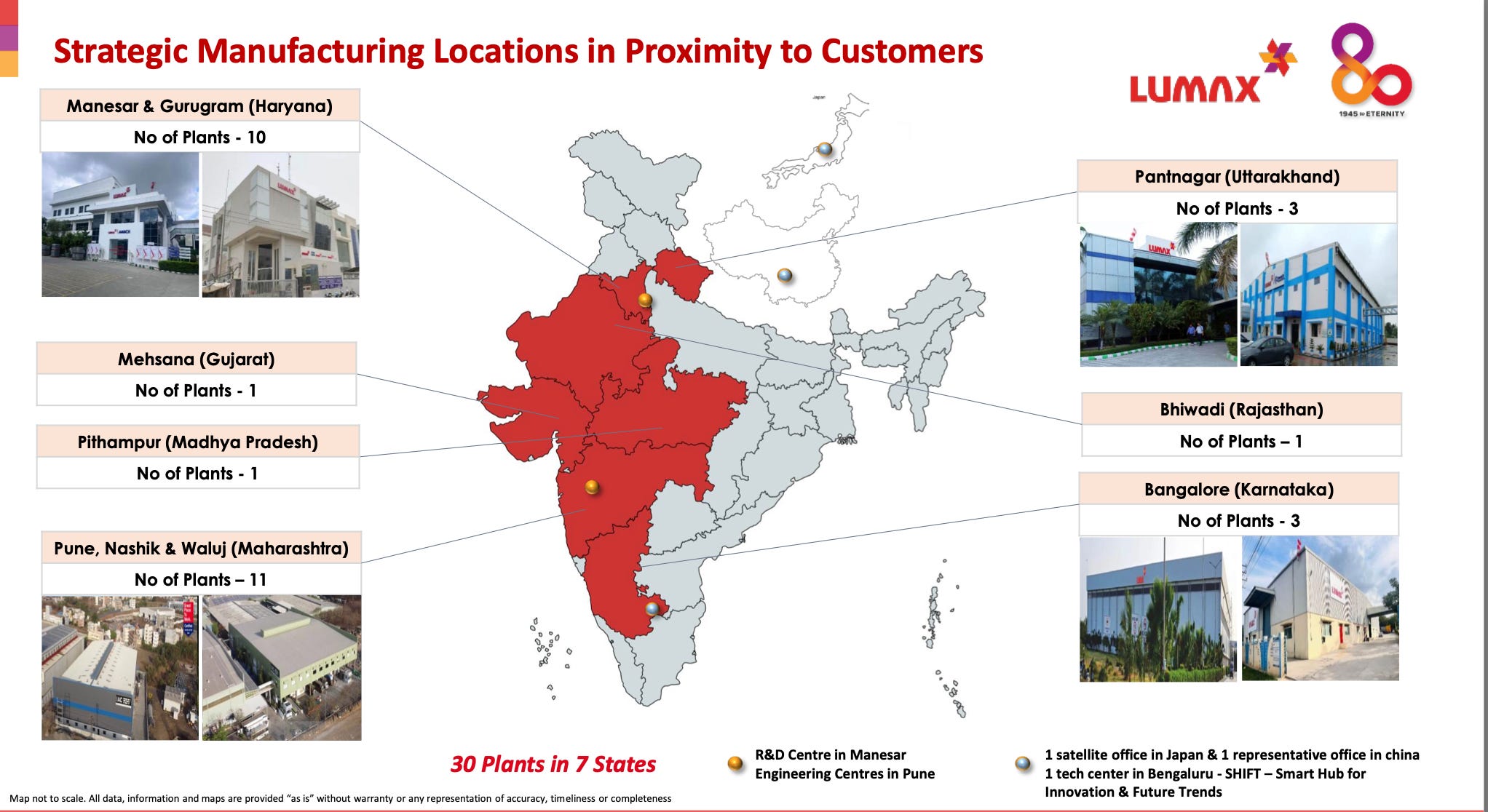

Lumax Auto Technologies, founded in 1981, has grown from a localized component maker into a diversified Tier-1 automotive systems supplier. It operates 30 manufacturing plants across 7 Indian states, serving all major Indian OEMs. In 9M FY26, revenue hit ₹3,453 crore, already ahead of FY24’s full-year number and almost equal to FY 25 revenue with one quarter remaining.

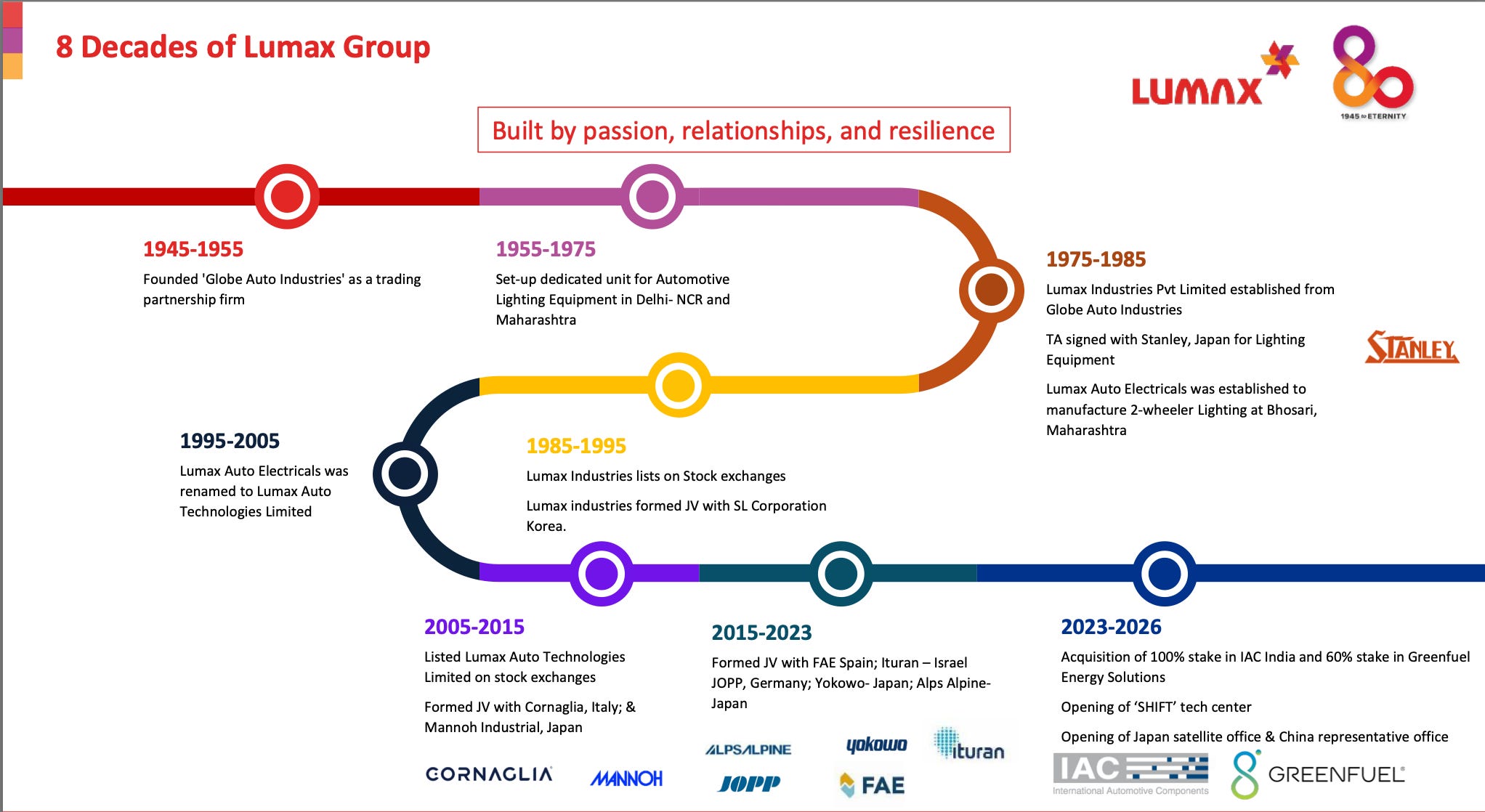

Lumax was founded in 1981. From a single lighting plant in 2005, it now operates 30 facilities across India. It is part of the Lumax group which has a 8-decade legacy.

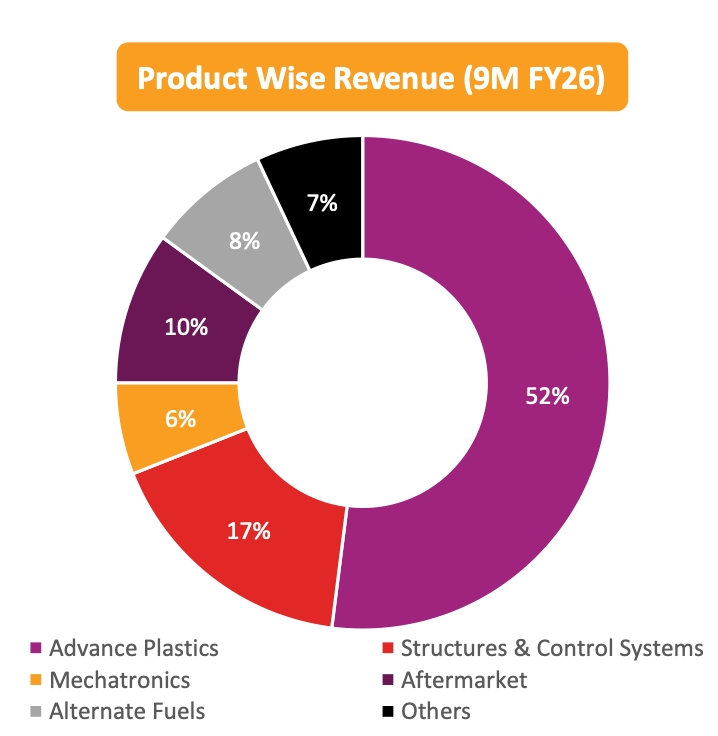

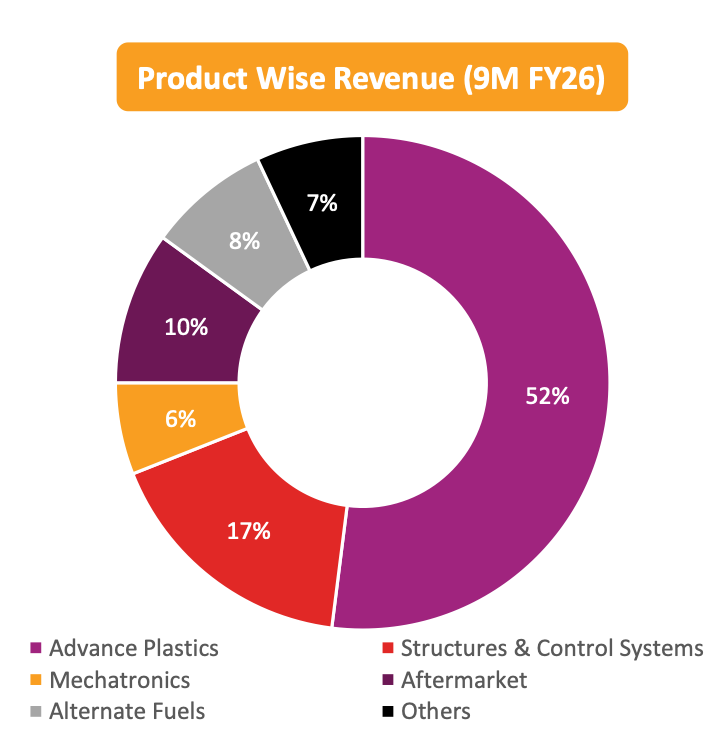

Their Products span advanced plastics, lighting, transmission mechanisms, electronics, and alternate fuel systems. The business model is built on supplying complex systems, not standalone parts. Complexity commands better margins.

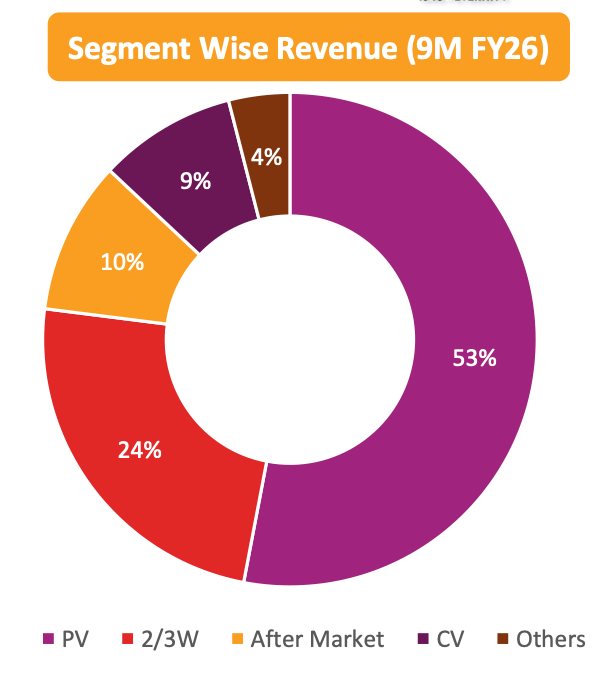

Passenger vehicles contribute 53% of 9M FY26 revenue. Two-wheelers add 24% and aftermarket 10%. Commercial vehicles contribute 9%. This spread insulates the company from category-specific slowdowns. Balance is built into the structure.

Content per vehicle for passenger cars has grown 5X in the last five years to ₹75,000 per vehicle. Two-wheelers now see ₹22,000 to ₹25,000 per vehicle, also up 5X. Premiumization is happening.

The company operates 30 plants across seven states with proximity to OEM clusters.

Operating margins expanded from 7% in FY21 to 9.5% in FY25. Scaling and margin expansion happening together. That combination is worth noting.

2. Acquisitions Fueling Expansion

Lumax has used inorganic moves to enter high-value product segments faster than organic development would allow. IAC India brought premium interior systems and EV contracts. Greenfuel opened the alternate fuels space. Both deals targeted profitable, low-debt businesses with existing OEM relationships already in place.

Lumax acquired a 75% stake in IAC International Automotive India in March 2023 for an enterprise value of ₹587 crore. The phased entry enabled controlled integration.

IAC India manufactures integrated cockpits and door panels for modern SUVs. These products raised Lumax’s content value per vehicle significantly.

The IAC deal made Lumax the exclusive interior supplier for Mahindra’s BE6 and XEV 9e electric vehicles launched in late 2024.

Lumax completed the 100% buyout of IAC India in May 2025 for ₹221 crore. Full ownership consolidates control in the interior systems segment.

IAC India generated revenue of ₹1,123 crore in 9M FY26 with EBITDA of ₹202 crore and PAT of ₹92 crore. Its order book stands at ₹500 crore.

In September 2024, Lumax acquired a 60% stake in Greenfuel Energy Solutions for ₹153 crore. Greenfuel supplies high-pressure systems for CNG and hydrogen vehicles. Entry into clean mobility.

Greenfuel generated revenue of ₹270 crore in 9M FY26 with EBITDA of ₹51 crore and PAT of ₹35 crore. The order book stands at ₹180 crore.

Greenfuel already supplied Maruti Suzuki and Tata Motors for their CNG models before the deal. Existing OEM relationships meant immediate revenue credibility.

Management filters acquisition targets for profitability and low leverage. This discipline has kept the balance sheet from stretching despite three major deals.

Lumax is pursuing a full merger of IAC India into the parent entity. The first motion is complete and the NCLT order is awaited.

3. Gear Shifter Market Control

Through its joint venture with Japan’s Mannoh, Lumax commands 80% of the Indian passenger vehicle gear shifter market. The division has evolved from mechanical levers to electronic shift-by-wire systems. Mannoh generated ₹287 crore in revenue and ₹46 crore EBITDA in 9M FY26, a stable and profitable entity providing a cash bedrock for the group.

Lumax Mannoh Allied Technologies holds an 80% market share in passenger vehicle gear shifters in India. They supply almost every major Indian car brand.

The product range covers manual, automatic, AMT, and CVT shifters with full local design and testing capabilities.

In September 2023, Lumax launched a shift-by-wire gear shifter that replaces mechanical cables with electronic actuators. Interior layouts simplify and EV compatibility improves.

The shift-by-wire system is designed specifically for electric and hybrid platforms. This keeps the shifter business relevant even as combustion engines shrink.

A joint venture with Germany’s Jopp extends shifter expertise to commercial vehicles and off-highway machinery. Heavy-duty segments need entirely different engineering.

Monostable e-shifters with haptic feedback are now the focus. These carry higher prices and attract premium car buyers.

Mannoh’s current order book stands at ₹95 crore with customers including Maruti, Mahindra, Toyota, Tata, Honda, and Daimler. A blue-chip client list.

The shifter division is a mature, profitable entity generating stable cash flows. This allows the group to fund newer bets in hydrogen storage and telematics.

4. Wide Client Base

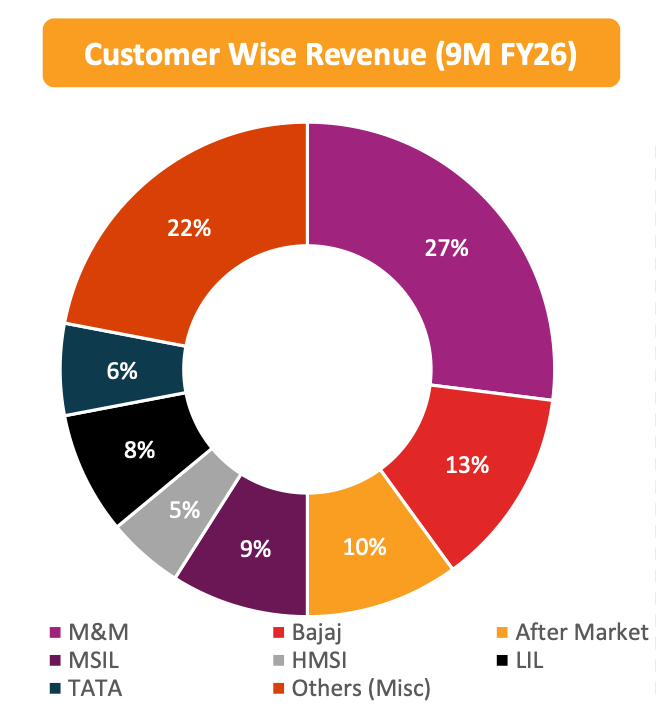

Lumax serves virtually every significant Indian OEM across vehicle segments. Mahindra, Bajaj, Maruti, Tata, Honda, and Hyundai all feature in the client roster. No single segment slowdown at one OEM can meaningfully destabilize the overall revenue mix given how broadly the business is spread.

Mahindra accounts for 27% of 9M FY26 revenue, deepened through wins in interiors and lighting. IAC India was named Business Partner of the Year at M&M Vendor Conference in February 2025.

Bajaj Auto contributes 13% of 9M FY26 consolidated revenue. Lumax is a single-source supplier for several of Bajaj’s motorcycle models. Single-source status means switching is operationally painful.

Maruti Suzuki accounts for 9% of 9M FY26 revenue. Revenue is also spread across Tata, Honda, and Hyundai.

The IAC acquisition introduced Volkswagen and Volvo Eicher into the Lumax client network. Premium and commercial vehicle relationships were previously absent from the group. Acquisition opened doors the sales team could not.

TVS Motor Company and HMSI receive critical lighting and chassis components for high-volume commuter bikes.

Management is actively diversifying IAC India’s revenue beyond Mahindra and Maruti. Discussions with other OEMs for integrated cabin solutions are underway.

Lumax supplies four-wheel gear shift assemblies to Toyota and Renault-Nissan globally. Meeting Toyota’s quality standards is an excellent credential.

Their ₹1,450 crore order book is 40% linked to future and clean mobility products. Revenue growth is coming from new contracts, not renewals. That signals genuine commercial momentum.

The order book unwinds in stages: ₹472 crore in FY27, ₹643 crore in FY28, ₹335 crore in FY29. Four-year visibility is a strong signal for auto components business.

5. Electronics and Software Push

Lumax inaugurated its SHIFT technology center in Bengaluru in October 2025 to develop software-defined vehicle capabilities. The BRIDGE strategy for FY26-31 explicitly targets a Tier-1 to Tier-0.5 transition.

SHIFT stands for Smart Hub for Innovation and Future Trends. The Bengaluru center was inaugurated in October 2025 as the group’s electronics research nucleus.

The hub develops Advanced Driver Assistance Systems, which are becoming essential as safety regulations tighten in India. Regulatory-driven demand is more predictable now.

The company now has over 500 engineers focused on innovation and IPR. Satellite offices in Japan and a representative office in China extend the research reach globally.

The center is building over-the-air update architectures that allow car features to be modified post-purchase. This is the smartphone model applied to cars.

Body Control Modules managing power windows, central locking, and other electronic functions are a dedicated strategic goal for the FY26-31 BRIDGE plan. Each addition raises unit complexity and price. Margin expansion through electronics content.

Vehicle-to-vehicle and vehicle-to-infrastructure communication is another research pillar for the SHIFT team. Connected cars are still in early innings in India.

Ambient lighting and smart digital display systems for premium cabins are also in development. SUV makers are actively seeking these differentiators. Aesthetic electronics carry strong pricing power.

Lumax is targeting a Tier-0.5 supplier role by combining hardware supply with software integration. The BRIDGE plan names this as the defining goal for the decade.

6. Aftermarket Network Strength

Lumax’s aftermarket division contributed 10% of 9M FY26 consolidated revenue. Over 575 channel partners and 27,500 retail touchpoints make this one of the widest organized aftermarket networks in its product categories.

The aftermarket segment posted 16% YoY revenue growth in Q3 FY26 and 15% for 9M FY26.

Over 575 channel partners operate across India, keeping Lumax products available in most automotive markets. Small-town mechanics can source Lumax parts.

A field force of over 200 people supports 40,000 retailers and 30,000 mechanics directly.

The product range is expanding from lighting into mechatronics, sensors, lubricants, and coolants. More categories per mechanic visit increases wallet capture.

Eight decades of brand trust allow Lumax to charge a premium over generic unorganized competitors.

Aftermarket margins are structurally higher than OEM margins because car companies do not control aftermarket pricing. This extra margin improves total group profitability.

7. Clean and Alternate Fuels

In September 2024, Lumax acquired a 60% stake in Greenfuel Energy Solutions for ₹153 crore. Greenfuel posted ₹270 crore in revenue, ₹51 crore EBITDA, and ₹35 crore PAT in just 9M FY26. Clean and future mobility contributed 6% of revenue in FY25, estimated to reach 14% in FY26, with a target of 20%+ by FY31.

Greenfuel makes high-pressure fuel delivery and storage systems for CNG vehicles. India’s CNG market is expanding as consumers seek cheaper alternatives to petrol and diesel.

Greenfuel was already supplying Maruti Suzuki and Tata Motors for their CNG models before the acquisition.

In 9M FY26, Greenfuel delivered ₹270 crore revenue, ₹51 crore EBITDA, and ₹35 crore PAT. The business is profitable and scaling faster than expected.

The Greenfuel order book stands at ₹180 crore. Content value per CNG vehicle is ₹7,000 to ₹10,000 per unit.

Greenfuel’s high-pressure storage technology applies to hydrogen platforms for trucks and buses. The company is already exploring this adjacency.

The alternate fuels business model is asset-light, requiring limited capital to scale.

Greenfuel’s fire and smoke suppression systems for public transport buses add a safety product category. Fleet operators face growing regulatory requirements.

Combining Greenfuel’s technology with Lumax’s 27,500-point aftermarket network creates a potential category-leader in organized CNG conversion.

8. TPM and Robotic Manufacturing

Lumax has received 14 JIPM TPM (Total Productive Maintenance) Awards across its plants, including a JIPM TPM Award for Consistent Commitment to the Bengaluru plant in March 2025. Indicates Manufacturing excellence.

Lumax holds 14 JIPM Awards across its plants. In March 2025, the Bengaluru plant won the JIPM TPM Award specifically for Consistent Commitment.

LCAT won the Gold award at the 50th International Convention on Quality Control Circles in Taiwan in 2025.

Kuruli alone operates 62 robots for welding and surface treatment tasks. Robotic automation ensures the dimensional consistency that global OEMs demand.

Ultrasonic welding and automatic bead laying are used for plastic module assembly. These ensure precise fitting and component longevity across vehicle lifespans.

A 100% Poka Yoke system ensures no defective part leaves any factory floor. These mistake-proofing methods eliminate human error from critical production steps.

SAP software has been deployed across all IAC India locations post-acquisition. Real-time production and inventory tracking across states is now operational.

Plants are concentrated near Pune, Manesar, and Bangalore with 10 of 30 plants in Haryana alone. Just-in-time delivery is structurally enabled by geography.

9. Global JV Alliances

Lumax maintains 9 active global joint ventures spanning Japan, Germany, Israel, Italy, and Spain. Additionally, a multi-decade technology agreement with Stanley of Japan anchors the lighting business. These alliances provide proprietary technology access without bearing the full R&D cost.

Joint ventures split technology development risk between Lumax and global partners. Lumax gets the technology. Partners get the Indian market. A win-win.

The technology agreement with Stanley of Japan has anchored the lighting business for decades. This relationship delivers the latest LED automotive lighting technologies to Indian platforms.

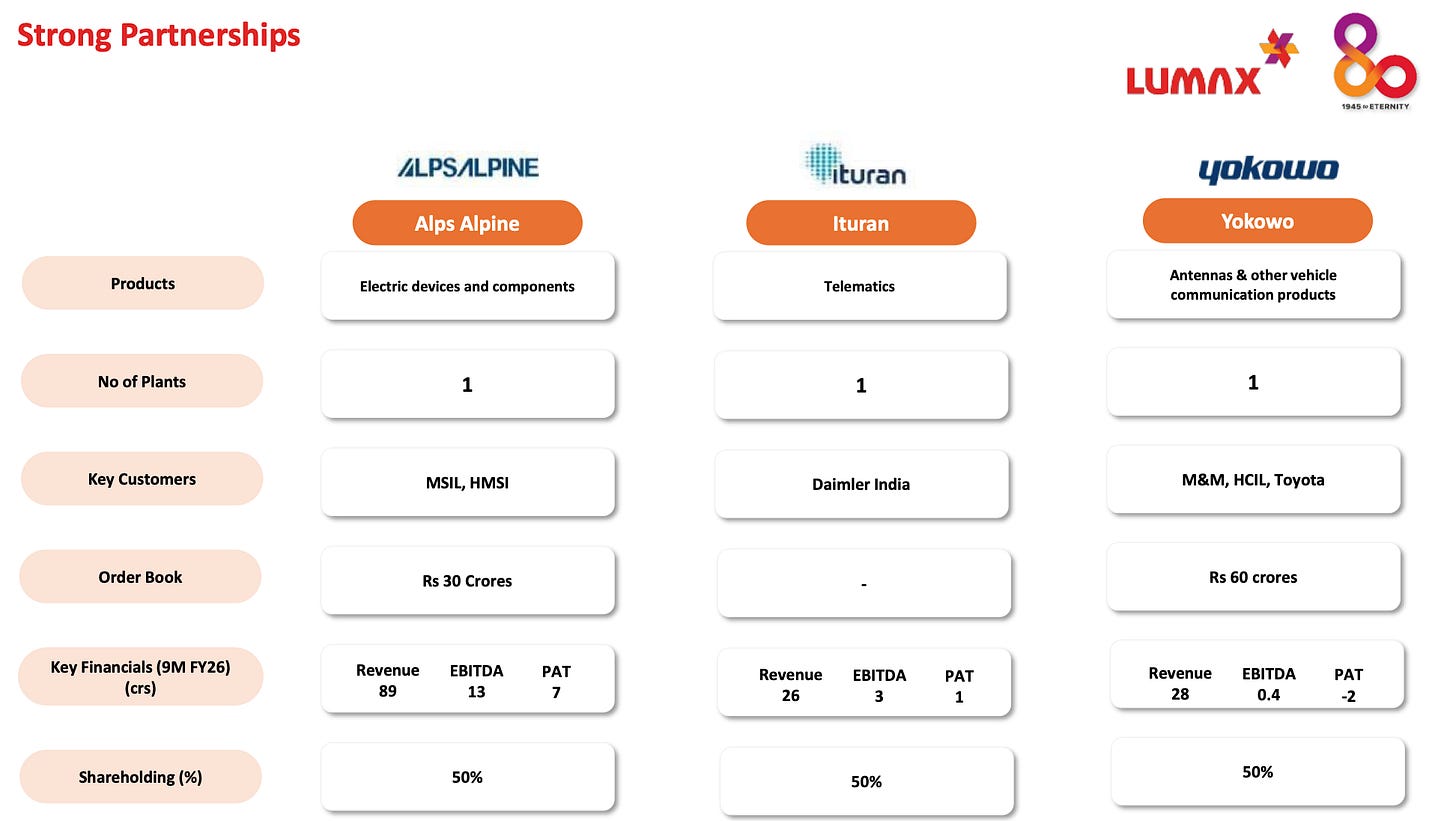

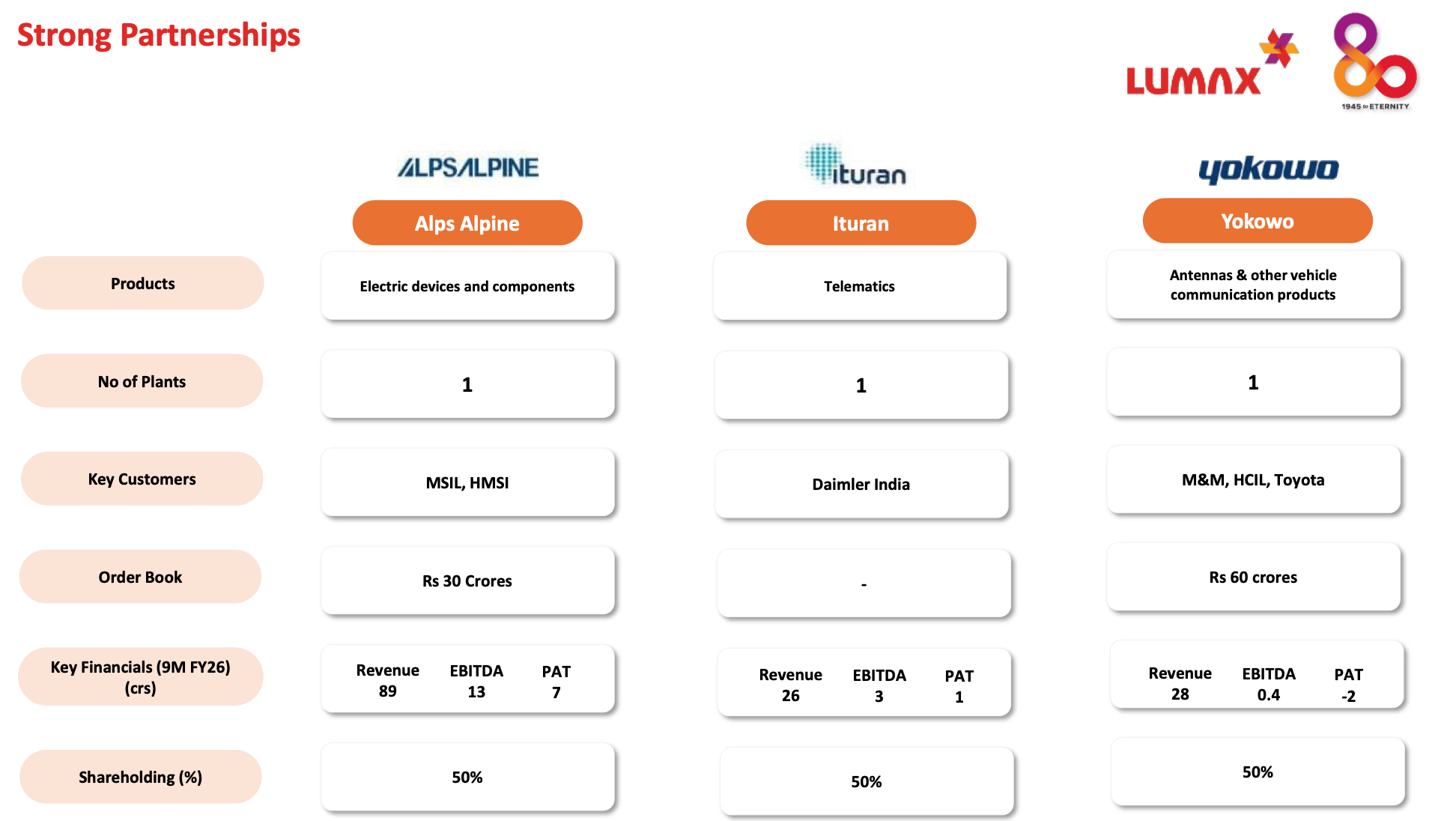

Lumax Alps Alpine India is a 50% JV with a Japanese electronics company. It generated ₹89 crore revenue and ₹13 crore EBITDA in 9M FY26.

Lumax Ituran is a 50% JV with Israel’s Ituran for telematics and connected vehicle services. It generated ₹26 crore revenue in 9M FY26 and validated tracking devices with Daimler India for over 15,000 commercial vehicles in 2024.

Cornaglia from Italy is a 50% JV for air intake and emission control systems. It generated ₹129 crore revenue and ₹30 crore EBITDA in 9M FY26.

FAE of Spain is an 84% owned subsidiary manufacturing oxygen sensors for two-wheeler fuel injection systems. Revenue was ₹54 crore in 9M FY26 with ₹5 crore EBITDA.

Lumax Yokowo develops on-board antennas and vehicle communication products.

The JV with Germany’s Jopp covers gear shift towers and sensors for commercial vehicles. It is in an investment phase with negative margins currently.

10. Risks and Red Flags

Over 50% of revenue is linked to advanced plastics, making polymer prices a direct margin lever. Crude oil spikes compress margins because OEM cost pass-through is not immediate.

Mahindra and Bajaj Auto together account for approximately 40% of consolidated 9M FY26 revenue. A major recall or sustained demand slump at either OEM delivers a measurable earnings impact.

IAC India still depends heavily on Mahindra and Maruti for interior segment revenue. The parent has a diversified base, but the subsidiary does not yet.

Total gross borrowings stand at approximately ₹961 crore as of September 2025. Net debt is only ₹153 crore after accounting for cash and liquid investments. Gross leverage is real. Net leverage is manageable.

The 50% JV with Israel’s Ituran creates geopolitical exposure. Ongoing tensions in the region could delay technology transfers or product launches.

Two early-stage JVs, Yokowo and Jopp, are currently loss-making with PAT of -₹2 crore each in 9M FY26. These are investments in future growth, but they dilute near-term profitability.

The IAC India merger with LATL is in progress with the first motion complete and order awaited. The LAL merger second motion order is also awaited. Multiple simultaneous mergers add integration overhead and management bandwidth strain.

Red Sea shipping disruptions have periodically raised logistics costs for imported electronic components. Global supply chain risks can compress margins in ways management cannot control.

The clean and future mobility target of 20% revenue by FY31 is ambitious. It requires execution across Greenfuel, ADAS, and SDV verticals simultaneously.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.