The aim of this series is to identify consistently performing businesses and understand a little bit more about how they are able to achieve this consistency.

Before we get into today’s stock, let me set some context regarding my research objectives. I do a weekly exercise to study and learn the business of one stock as part of my research activities as a SEBI registered RA. The primary objective is to understand the business in the context of its consistent performance over the last 5 years. Most of the research below is knowledge derived from the past Annual Reports and recent Quarterly Investor presentations. I am not an expert in this domain or industry. And more importantly, this is not a recommendation to buy the stock nor a thesis for a multibagger opportunity.

Let’s start ⬇️

Today, we will look at the key fundamentals & business of Krishna Institute of Medical Sciences Ltd.

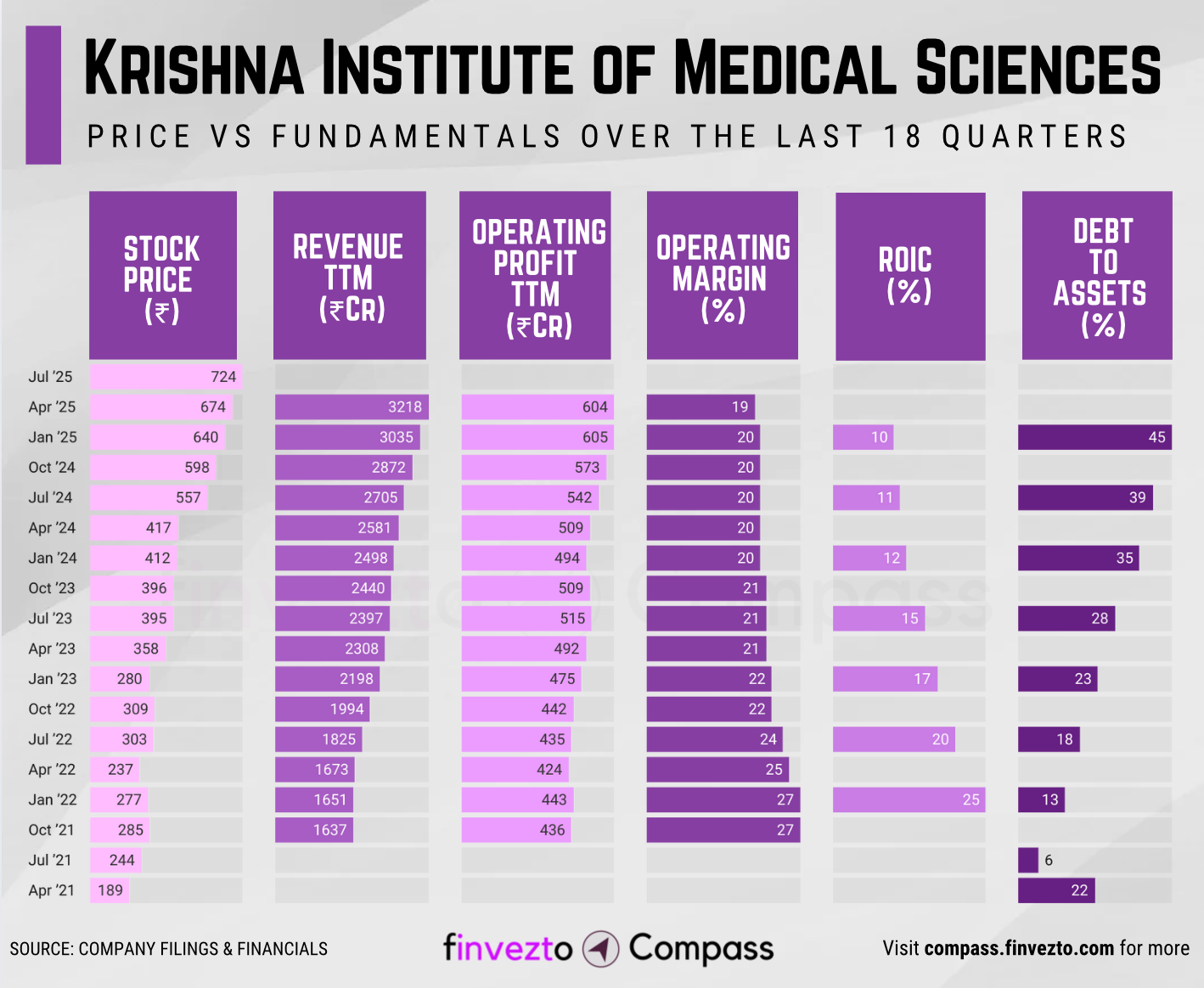

Click here to learn more about each of the parameters in the chart above.

What Has Led to This Consistency

Company Overview

Founded in 1973 as an educational institution, Krishna Institute of Medical Sciences transitioned to hospital operations in 2000 with a single 200-bed facility in Nellore, targeting South India's underserved healthcare markets.

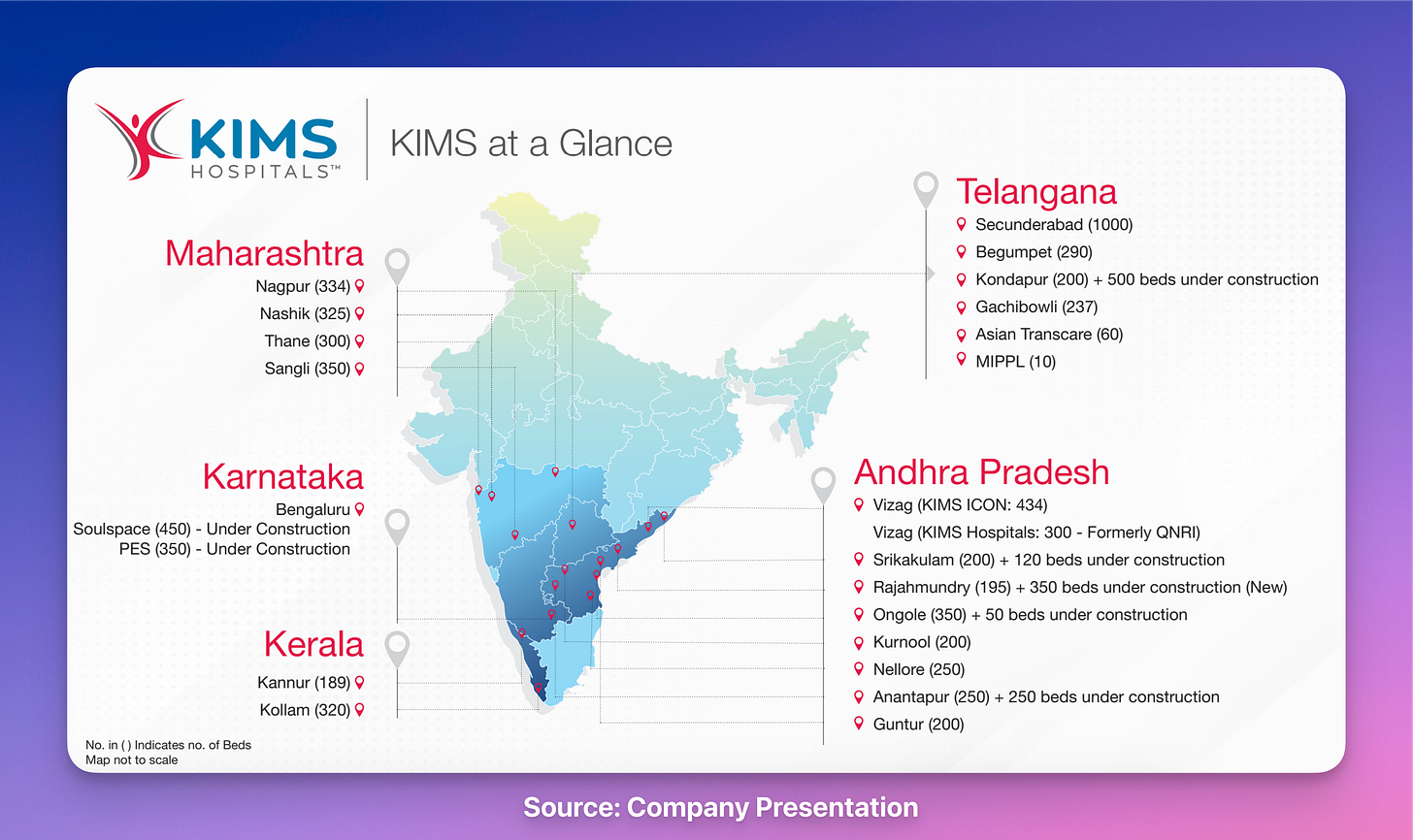

KIMS currently operates 8,300+ beds across 25 facilities.

There is a massive opportunity, as India requires an additional 2.4 million beds with current density only at 1.3 beds per 1,000 population versus 3-8 in developed countries.

Product Segments include:

Multi-specialty Healthcare - medical services across 25+ disciplines including cardiology, oncology, neurosciences

Advanced Transplantation - organ transplant programs for heart, lung, liver, kidney, and pancreas procedures

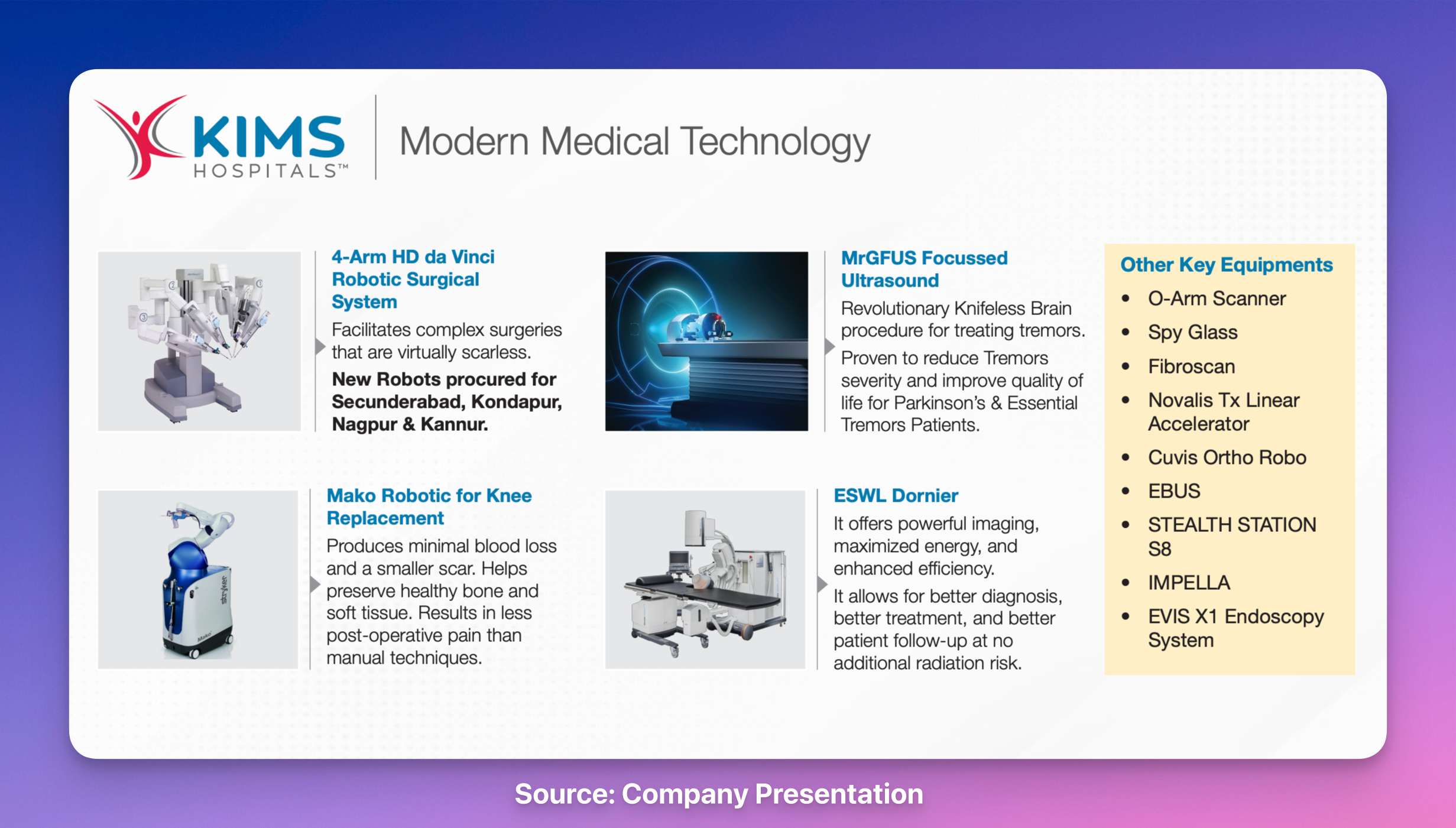

Robotic Surgery - robotic surgical services using latest da Vinci technology across multiple specialties

Medical Education - teaching programs and clinical training through affiliated medical colleges

Market Leadership

KIMS dominates its regional market through strong hospital presence and doctor relationships.

Regional focus allows KIMS to operate 2.2x more beds than Yashoda Hospitals in AP-Telangana markets → Revenue concentration

Achieves higher bed occupancy at 72% versus Apollo's 68% through better market presence → Utilization advantage

Average Revenue Per Occupied Bed (ARPOB) of ₹38,263 targets value segment + maintains superior 28.5% EBITDA margins versus competitors' 24% → Pricing efficiency

Telangana alone has 80,801 bed shortage representing massive infrastructure gap in core market → Growth potential

Transplant Excellence

Advanced organ transplant programs build medical reputation and attract premium patients.

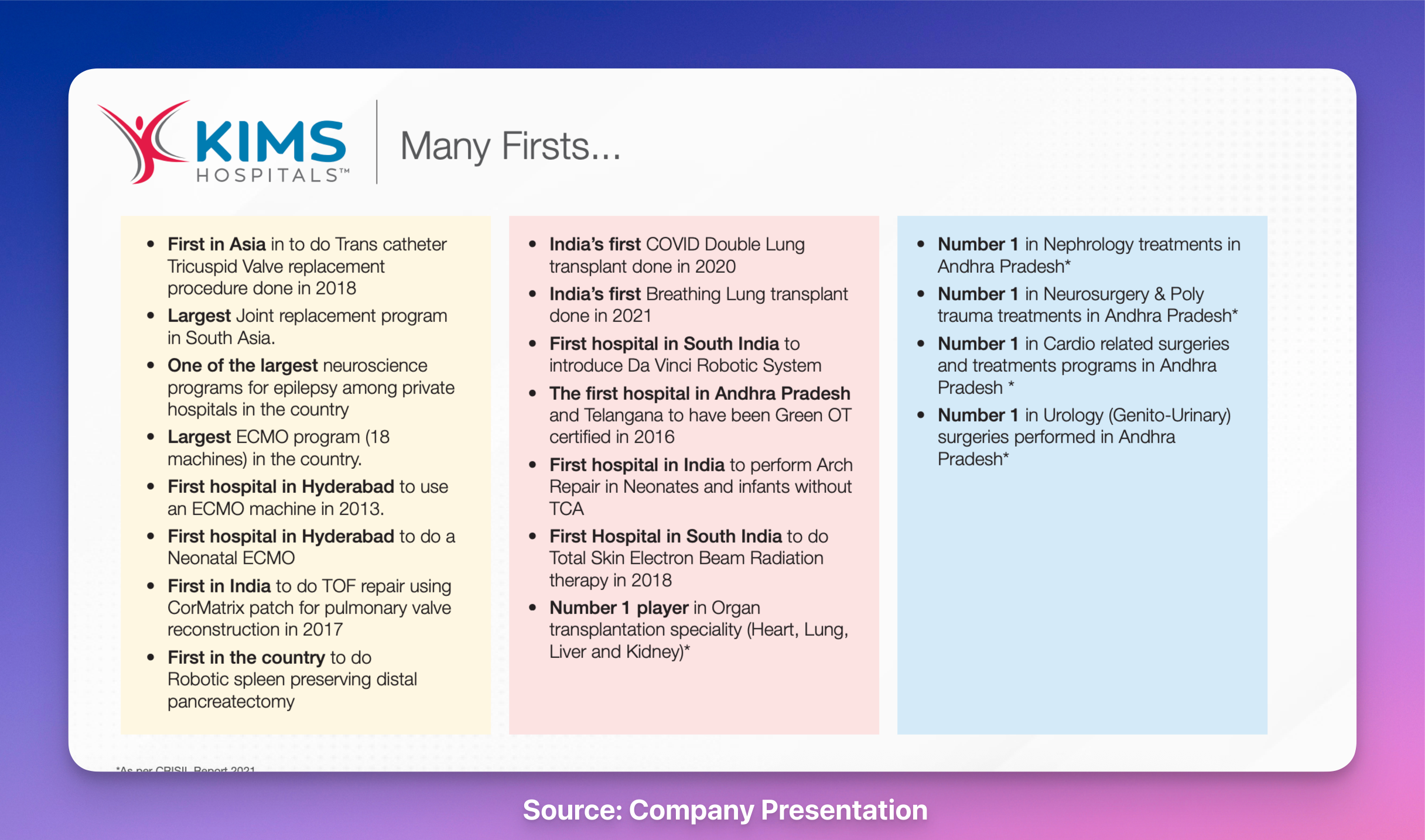

KIMS Heart and Lung Transplant team completed 22 COVID-19 double lung transplants representing Asia's highest single-institution pandemic volume → Medical reputation

Offers transplant programs across all major organs (heart, lung, liver, kidney, pancreas)

Performed first-in-Asia Transcatheter Tricuspid Valve replacement procedure creating innovation leadership in advanced cardiac interventions → Clinical leadership

Robotic Surgery

Advanced robotic surgical capabilities help KIMS charge higher prices and attract more patients.

Built South India's first robotic surgical facility providing 15-year technology head start in robotic procedures → First-mover advantage

Partnership with Intuitive Surgical launching 25 new robotic surgery programs ensures access to latest da Vinci systems → Service differentiation

Robotic procedures across oncology, gynecology, urology generate higher revenue per occupied bed versus regular approaches → Revenue benefits

Geographic Expansion

Multi-state expansion capabilities demonstrate superior integration expertise across acquired assets.

Acquisition of Queens NRI Hospital and strategic partnerships with existing facilities provide immediate market access → Revenue growth

Bengaluru and Thane metropolitan market entry positions company for higher revenue per occupied bed in premium segments → Revenue quality

Systematic integration improved acquired hospital bed occupancy rates from 71.83% to 80.49% within two years → Asset optimization

Infrastructure Scale

Network density and facility capacity create operational leverage and referral advantages.

Achieves industry-leading construction efficiency at ₹2.2-6.9 million per bed versus industry range of ₹3-15 million → Cost leadership

30-50% cost advantage in tier 2-3 cities enables faster expansion at lower capital intensity than tier 1 competitors → Economic moat

Partnership with Wipro GE Healthcare enables access to premium diagnostic equipment while competitors face ₹50-100 crore upfront investments per facility

Multi-state hospital network allows patient referrals for specialized treatments creating cross-facility revenue optimization → Network effects

Consistency Formula

Market Leadership + Transplant Excellence → Medical Reputation

Robotic Surgery + Geographic Expansion → Technology Differentiation

Infrastructure Scale + Market Leadership → Network Leverage

That’s it for today. Every week, I will pick one consistently performing stock and share a little bit more about their business for learning purposes. Do subcribe if you wish to receive it in your Inbox every Saturday.

At Finvezto Stock Research (Anand Ganapathy, SEBI Registered RA), we offer the following services. Do check out more details below.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes to understand more about the business. It does not recommend buying or selling stocks mentioned in this newsletter. Securities market investments carry market risks. Kindly review all related documents before investing.

FINVEZTO.COM | Powering Investing & Trading Research