Every week I study the business of one stock as part of my research activities as a SEBI registered RA. The primary objective of this post is to understand the business in the context of its performance over the last 5 years and how they are able to perform consistently. Most of the research below is based on past Annual Reports and recent Quarterly Investor presentations. This is an educational post and not a recommendation to buy the stock.

Let’s start ⬇️

Today, we will look at the key fundamentals & business of Garden Reach Shipbuilders & Engineers Ltd (GRSE)

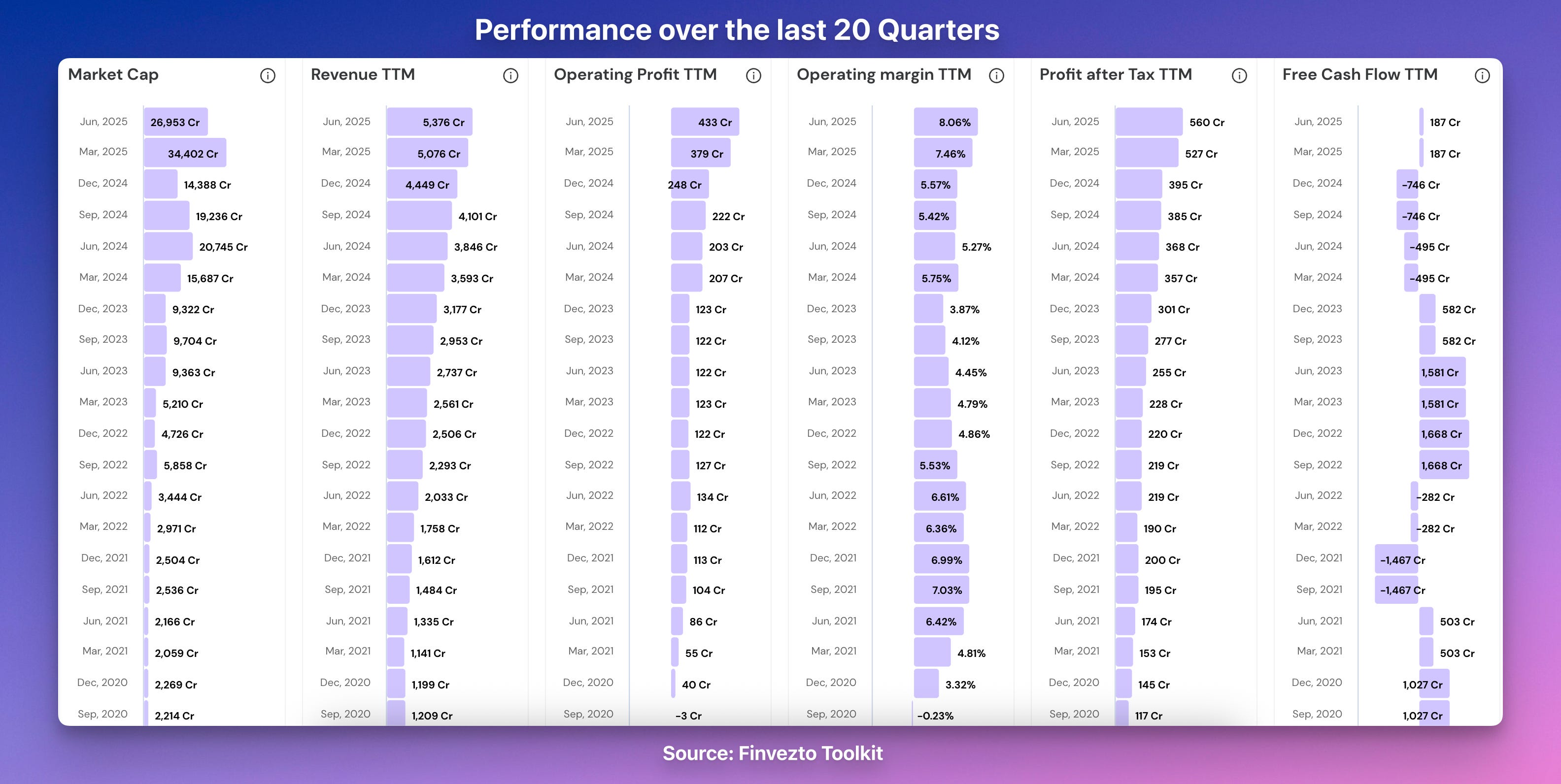

Key Fundamental Metrics of GRSE

Please find below fundamental metrics I use to visualize the consistent performance of the business. Here is a quick guide.

Over the last 5 years :

GRSE’s Revenue increased 4.5X (4.5 times), from 1200 Cr → 5376 Cr with great consistency every quarter. You can check the graph below.

Operating Profits grew 10X from 40 Cr to 433 Cr

Operating Margins increased.

Net profit grew 5X

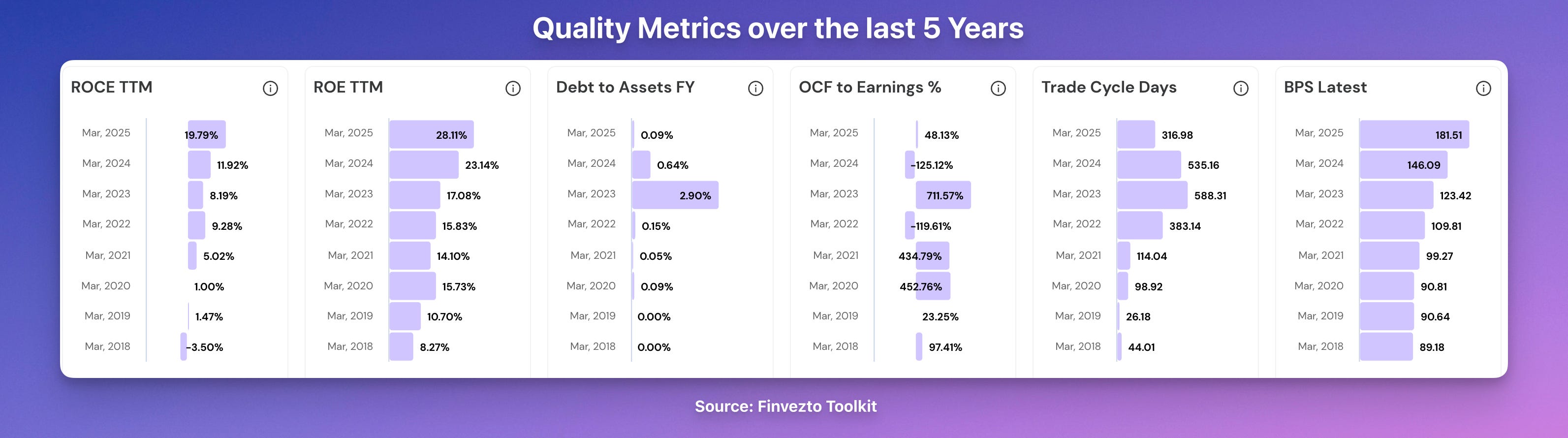

Even the Quality Metrics have consistently improved over the years.

ROCE and ROE have increased over the years

Debt levels have been low

What Has Led to This Consistency

Company Overview

Established in 1884, Garden Reach Shipbuilders & Engineers Limited transformed from a ship repair workshop into India's premier defense shipbuilder following 1960 nationalization.

The company built India's first indigenous warship INS Ajay in 1961 and became India's first warship exporter with 108+ warships delivered.

Product Segments include:

Shipbuilding Division: Naval warships, coast guard vessels, commercial ships, survey vessels

Engineering Division: Portable steel bridges, deck machinery, marine equipment, specialized components

Engine Division: MTU marine engines assembly, testing, overhauling through Rolls-Royce partnership

Export Division: International warship sales, commercial vessel exports, technology transfer projects

Revenue operates through long-term government contracts with Indian Navy and Coast Guard, supplemented by international export markets.

The company serves defense establishments requiring indigenous warship capabilities and foreign customers seeking cost-effective naval solutions.

Port Infrastructure Monopoly

Exclusive waterfront access creates operational and financial barriers for entry.

GRSE holds exclusive concession rights to three specialized dry docks at Syama Prasad Mookerjee Port capable of handling 160-meter warships with dedicated berths.

Protected harbor enables year-round ship construction and launching regardless of river water levels, providing operational consistency unavailable to land-based competitors.

Modular dry dock system enables concurrent construction of 20+ ships compared to competitors' sequential building methods requiring multiple separate facilities.

Regulatory Defense Preferences & Industry Tailwinds

Government defense contracts automatically favor Indian companies over foreign competitors, giving GRSE scoring advantages in ₹3+ lakh crore naval procurement tenders.

India’s Naval modernisation + rising defence capex imply a fatter pipeline (e.g., NGC/next-gen corvettes; future P-17 variants).

Banned imports list prohibits foreign suppliers from 310+ defense items including naval systems, creating protected domestic market for established Indian shipbuilders.

New defense contractors require 5-10 year security approval process while GRSE's government ownership provides automatic clearance for all classified naval projects.

GRSE achieves 90%+ indigenous content versus industry average of 70-80%, providing sustainable advantages under government indigenization mandates.

Technology Integration Ecosystem & Indegenization

Multi-decade partnerships creating switching costs and capability barriers.

Established relationships with 85-90 specialized West Bengal small manufacturers create integrated supply ecosystem for naval components requiring 8-12 year development cycles for new entrants.

Deep vendor base (hundreds of MSMEs) and localisation push (90%+ indigenisation target on future ships) de-risks imports and shortens lead times.

Advanced naval technologies require government-to-government deals and decades-long partnerships that private companies cannot access due to security restrictions and PSU preference policies.

Indigenous design capabilities through 200+ in-house naval architects provide complete warship development while competitors rely on foreign design partnerships and technology dependencies.

Indigenous integration of complex sensors/weapons on P-17A (MF-STAR, LRSAM, BrahMos, etc.) moves GRSE up the value curve.

3D PLM/AVEVA models across sites enable parallel work packages, clash-free outfitting, and faster design-to-production cycles.

Technology transfer agreements with Rolls-Royce MTU enable indigenous marine engine production targeting 40% local content, providing cost advantages and supply chain control.

Revenue Conversion & Diversification

Multi-Year Orderbook of ₹22,680 Cr as of Mar 31, 2025, gives multi-year execution runway and smoothing cyclicality.

Strong conversion to revenue: FY25 revenue from operations grew ~41% YoY to ₹5,076 Cr, signalling execution discipline, not just order wins.

Growing share of Lifecycle & After-market services such as refits, mid-life upgrades, ILS, spares, training etc. These have stickier margins and higher ROCE vs newbuilds.

Non-defence commercial pipeline (e.g., 7,500 DWT multi-purpose vessels for a German principal) diversifies cycles and proves yard versatility.

Consistency Formula

Port Infrastructure Monopoly → Revenue Predictability

Regulatory Defense Preferences + Technology Integration Ecosystem → Market Access Control

Strong Revenue Conversion + Diversification → Consistent Revenue across cycles

FINVEZTO.COM | Actionable Investing & Trading Ideas

At Finvezto Stock Research (Anand Ganapathy, SEBI Registered RA), we offer the following services. Do check out more details below.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes to understand more about the business. It does not recommend buying or selling stocks mentioned in this newsletter. Securities market investments carry market risks. Kindly review all related documents before investing.