Gravita India Ltd || Consistently Performing Stocks #69

What has led to the consistency?

Every week I analyze a company’s fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.

This week, Let’s explore the business & fundamentals of Gravita India Ltd. NSE: GRAVITA

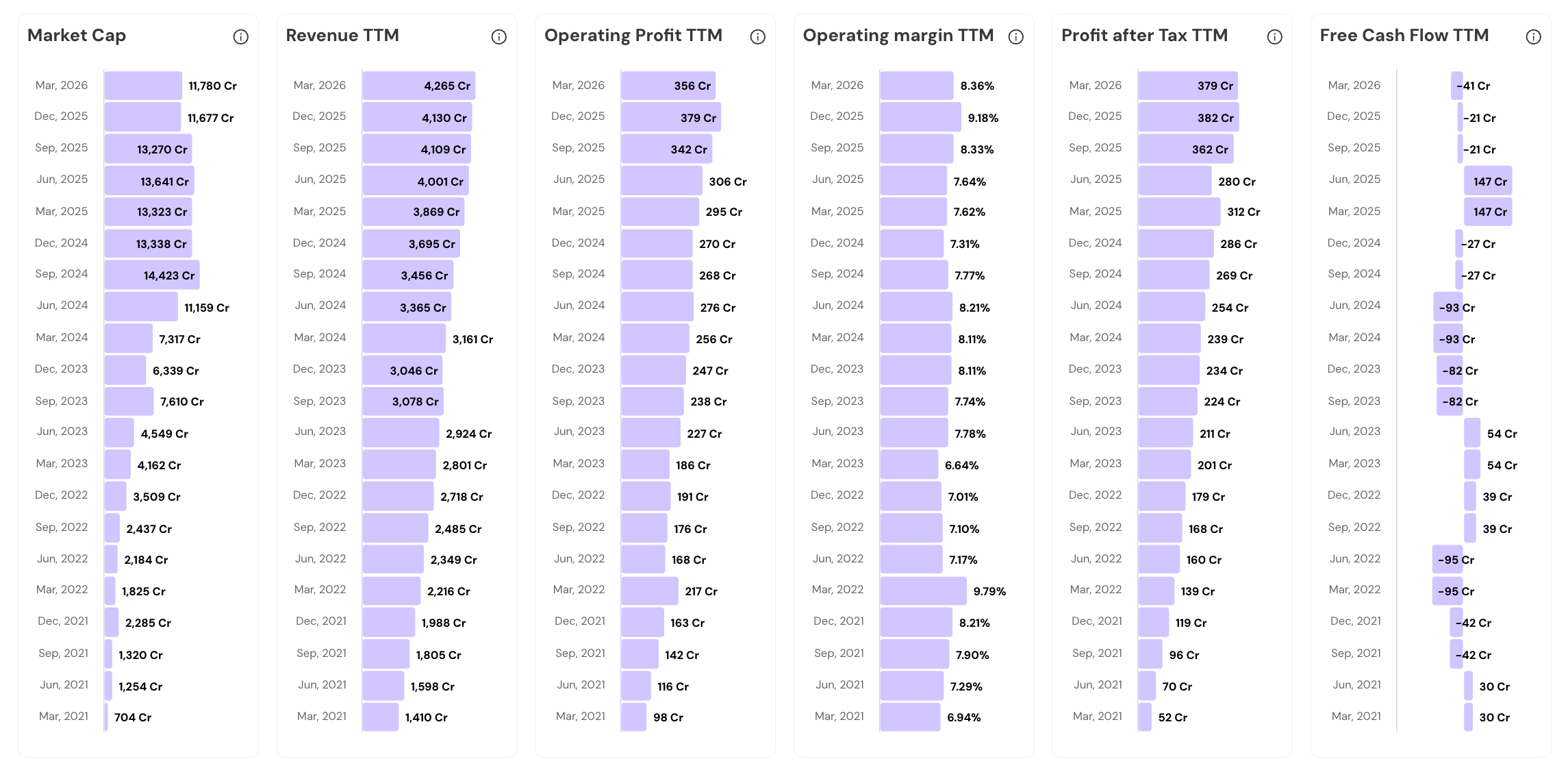

Performance Chart

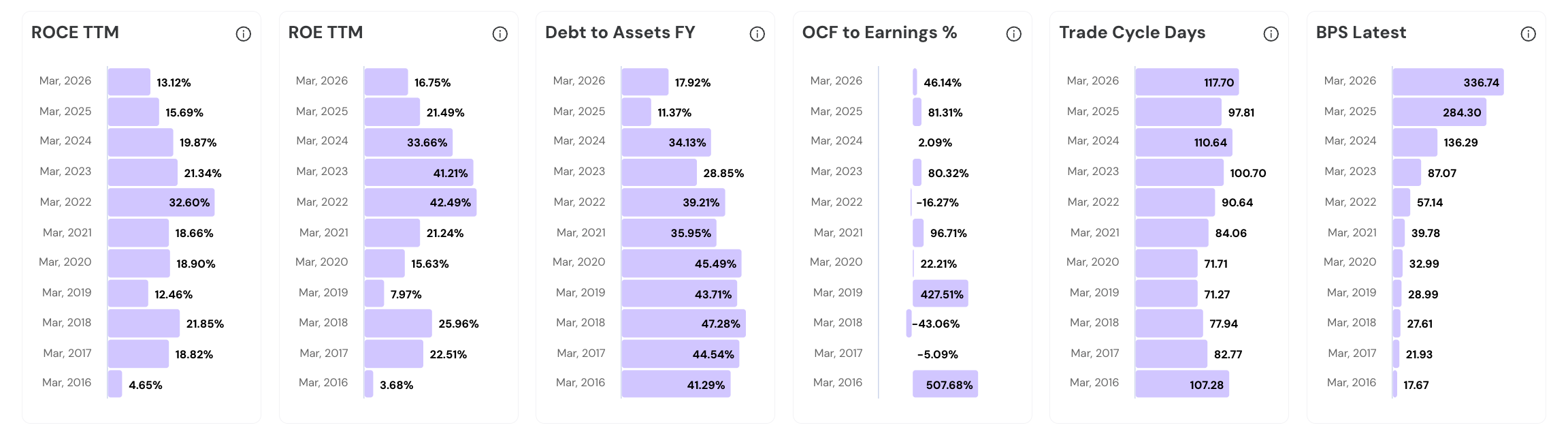

Quality Chart

Their Road to Consistency

1. Overview and Business Model

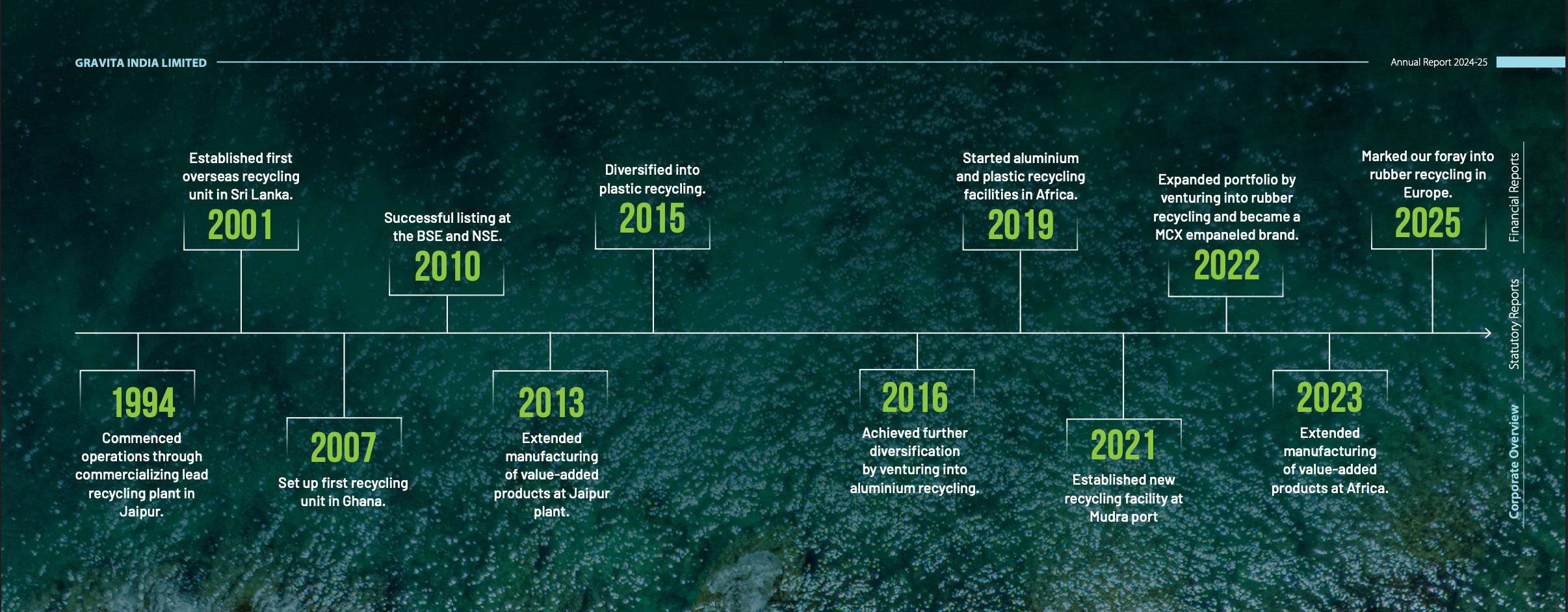

Gravita India Limited, founded in 1992 by Rajat Agrawal in Jaipur, converts discarded batteries, aluminium, plastic, rubber, and copper scrap into high-purity industrial materials. The raw material that feeds its smelters and processing plants is called feedstock. In Gravita's world, that feedstock is the stuff most people throw away: used car batteries from a roadside mechanic, crushed plastic bottles from a municipal collector, old copper wiring pulled out of demolished buildings etc.

Gravita operates across six recycling verticals: Lead, Aluminium, Plastic, Rubber, Copper, and Lithium.

Lead recycling dominates the revenue mix, contributing approximately 87% of total sales volumes. Automotive battery replacement demand is predictable and non-discretionary.

The business model earns a processing spread: cheap unorganized scrap goes in, premium customized industrial materials come out.

Overseas revenues contributed 72% of FY26 total, with India at 28%. A Rajasthan-headquartered company with genuinely global revenue. The split is increasingly international.

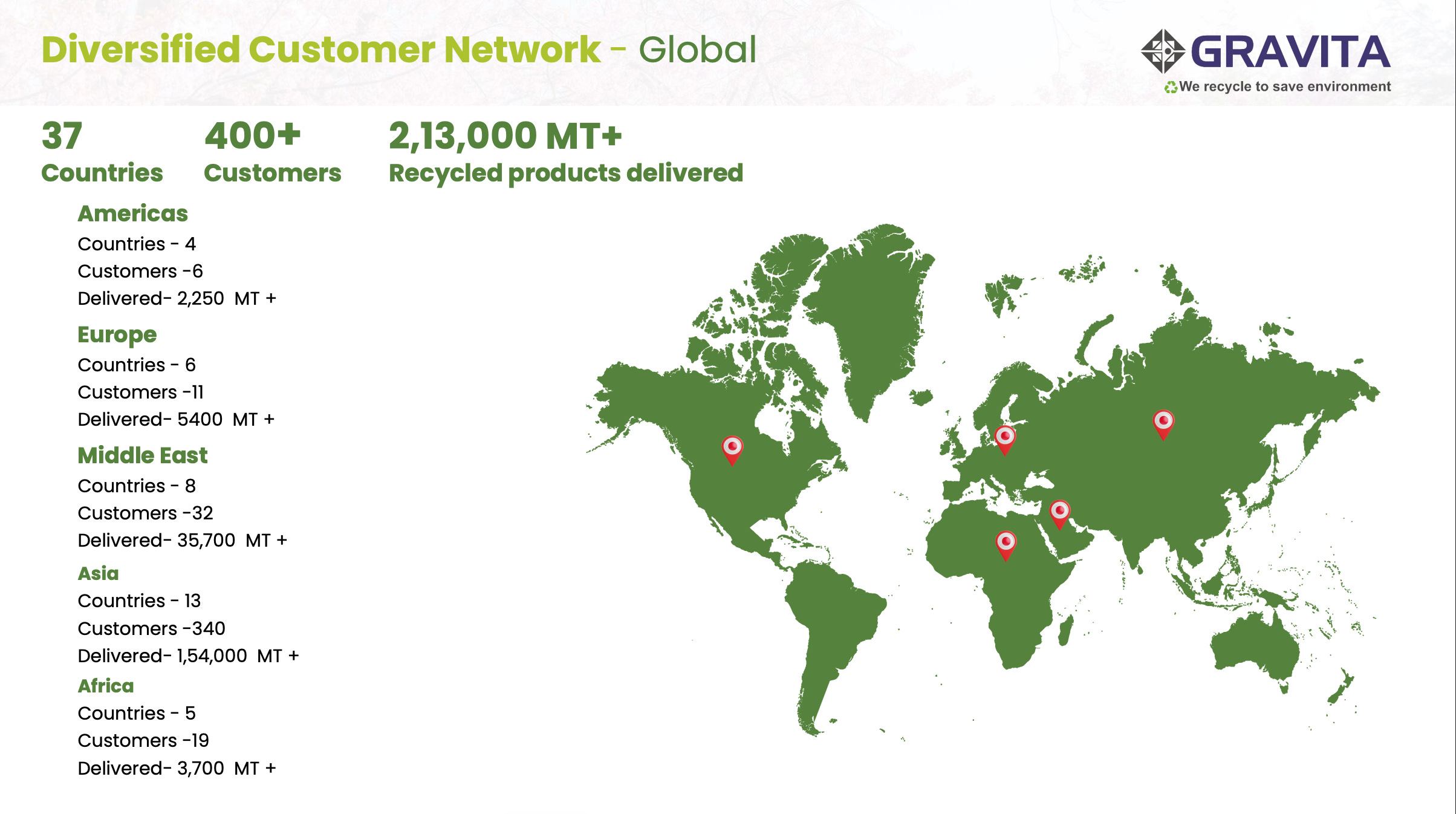

The company serves 400+ customers across 37 countries. Partners include blue-chip names such as Amara Raja, Exide, Tata Batteries, Glencore, Siemens, and Polycab.

2. Margins Locked In

Gravita uses a back-to-back hedging mechanism that locks in processing spreads the moment scrap is purchased. This protects EBITDA from London Metal Exchange price swings. EBITDA margins have held between 9-10% for five consecutive years despite sharp commodity cycles.

Every scrap purchase is placed only after a corresponding binding customer sales order is confirmed first. Zero unhedged inventory exists at any point. Risk is engineered out.

70-75% of raw material inventory is hedged back-to-back with customers at pricing tied to LME cash rates. Processing spreads are captured at the point of purchase.

The remaining 25% of metal inventory is hedged directly on the London Metal Exchange through standard derivative contracts. Two layers of hedging leave no meaningful commodity risk in the business.

In Q3 FY26, raw material costs rose sharply. Hedging gains of ₹9.8 crore offset higher scrap procurement expenses. EBITDA margins held stable.

MCX empanelment for domestic aluminium hedging was secured, closing a structural vulnerability in India margin protection.

Hedging gains are reported under other income. Derivative losses under other expenses. The accounting is clean, transparent, and trackable.

EBITDA margins stayed between 9% and 10.5% across five consecutive fiscal years, through multiple commodity cycles.

Smaller regional recyclers cannot access LME hedging platforms at their scale. This capability gap creates a durable operational moat.

3. Feedstock Network Edge

In recycling, the player with the cheapest, most secure raw material supply wins structurally. Gravita operates 39 owned scrap yards and 2,200+ touchpoints globally, collecting 3,30,000+ MT annually. This procurement network, built over 30 years, is the most durable competitive moat in the business.

Gravita runs 39 owned scrap yards and 2,200+ global touchpoints across five continents. Annual scrap collection exceeds 3,30,000 MT. No Indian recycler comes close to this procurement depth.

Asia operations include 6 owned yards, 1,200+ touchpoints, and 1,92,250+ MT collected annually. India drives the bulk.

Africa has 32 owned yards and 900+ touchpoints collecting 74,250+ MT. Plants sit close to scrap generators. African input costs are structurally low.

Americas and Europe together cover 100+ touchpoints and collect 60,500+ MT annually. Developed-market scrap quality is often higher purity. Geographic diversity removes dependence on any single feedstock market.

Domestic scrap sourcing rose from 43% in FY25 to 52% in Q2 FY26, driven by EPR and BWMR mandates. The India scrap cycle is formalizing.

Scrap collected directly from OEMs and battery brands compresses the working capital cycle to 74 days. Intermediaries are bypassed entirely. Every node eliminated saves cost and accelerates cash conversion.

Replicating 39 owned yards across five continents would take decades and hundreds of crores of investment. This network is a time-built, capital-intensive entry barrier.

Total production capacity stands at 4.36 lakh MT as of May 2026. Capacity utilization is 70%, excluding recent additions. The feedstock pipeline is feeding the plant base at a healthy rate.

4. Value-Added Product Mix

Gravita has shifted from basic recycled ingots toward customized alloys and specialty compounds. Value-added products contributed 42% of FY26 revenues, up from 36% in FY22.

The product catalog includes customized lead alloys, lead sheets, red lead, TPO, aluminium alloys, plastic granules, copper sheets, brass cups, and copper foils. A full-spectrum product library across six materials.

Value-added products were 42% of FY26 revenues and 36% in FY22. Product mix quality is the rising tide underneath the revenue numbers.

OEM approvals for customized alloys require significant time and technical validation. Once granted, switching costs make customer relationships structurally sticky.

Average lead EBITDA per tonne reached ₹23,043 in recent periods. Basic recyclers earn far less on the same tonne of scrap. They earn a customization premium.

The plastic segment targets ₹10-11 per kilogram EBITDA as a steady-state margin. Per-unit margin targets guide production mix decisions. This pricing discipline shows up in the EBITDA consistency.

African facilities added value-added processing in FY23. Cheap African scrap is now converted into premium alloys and exported to European and Middle Eastern customers.

The company holds a healthy 60,000 MT+ orderbook as of May 2026. This forward visibility supports consistent quarterly delivery. Orderbook depth is a lead indicator.

5. Capital-Efficient Expansion

Gravita enforces a strict capital allocation mandate: maximum 3-year payback, 25%+ ROIC, and 8+ asset turns on every new project. Brownfield expansions over greenfield bets keep the balance sheet clean. Capacity scales from 4.2 lakh MT in FY26 to 8 lakh MTPA by FY29, mostly self-funded.

Capital allocation rules are non-negotiable: payback below 3 years, ROIC above 25%, asset turns above 8x. Every project clears this filter before money is committed.

FY26 capex was ₹372 crore: ₹200 crore for existing verticals, ₹172 crore for new ones.

Mundra lead recycling capacity expanded by 80,300 MTPA to 1,45,100 MTPA using existing port-side infrastructure.

The 6,000 MTPA Li-ion battery recycling plant at Mundra was commissioned in FY26 at a modest initial cost.

Capacity grows from 4,19,959 MT in FY26 to 6,54,959 MT by FY29E in existing verticals alone. New verticals add another 1,46,600 MT. Total target: 8,00,000+ MTPA by FY29.

Total capex through FY29 is approximately ₹755 crore, spread across four years. Internal cash generation covers this without external equity raises.

ROIC held at 24% in FY26 despite heavy expansion activity.

6. Global Ops

Gravita operates 14 plants across Asia, Africa, Europe, and the Americas. Overseas revenues were 72% of FY26 total. Factories in Africa’s Least Developed Countries provide full corporate tax exemptions and zero-duty metal imports into India.

Operations span 14 plants across four continents: India, Sri Lanka, five African countries, Romania, and Dominican Republic. Overseas contributed 72% of FY26 revenues.

Factories in Mozambique, Senegal, and Tanzania qualify for full corporate tax exemptions as LDC-classified operations. These tax savings flow directly to net margins.

Approximately 80% of lead produced in LDC plants enters India duty-free, bypassing the standard 5% import tariff. Africa processes cheap scrap. India receives zero-duty refined metal.

The Mundra port facility enables direct ship-to-plant raw material intake and finished product export. Port proximity lowers logistics cost per tonne of both inputs and outputs.

African facilities export value-added formulations to European and Middle Eastern customers since FY23. The Africa-to-Europe value chain is high-margin arbitrage.

Rubber recycling in Romania started in FY25, capturing EU-mandated demand for certified recycled polymers. Europe’s environmental regulation is Gravita’s growth catalyst.

The expansion playbook is reproducible: start small, grow volumes, commission a plant near proven scrap sources. 9 overseas facilities were built this way across 25 years.

70% of total manufacturing capacity is located outside India. This scale of international presence reduces single-country regulatory, economic, and policy concentration risk.

7. Policy Creates Tailwind

India’s Battery Waste Management Rules, EPR mandates, Vehicle Scrappage Policy, and GST are systematically closing the informal recycling sector. Every tonne displaced from an informal smelter flows into Gravita’s authorized network.

Battery Waste Management Rules legally bind brands like Exide, Amara Raja, and Tata Batteries to meet EPR targets only through authorized recyclers. Gravita is a primary authorized partner.

GST eliminated the tax arbitrage that unregistered scrap traders used to undercut organized players. The informal cost advantage is permanently gone. Competition has narrowed to execution quality and feedstock access.

The Vehicle Scrappage Policy mandates retirement of old commercial vehicles, releasing end-of-life batteries into formal collection channels. Policy feeds feedstock at scale. Volume flowing formally is a compounding benefit.

State pollution control boards are systematically shutting non-compliant local smelters. Their scrap volumes redirect to authorized collection networks. Informal closures are Gravita’s feedstock gain.

Domestic scrap sourcing rose from 43% in FY25 to 52% in Q2 FY26, driven directly by EPR and BWMR compliance pressures.

ILA-accreditation (International Lead Association) is rare in India. Premium customers require it before placing orders. Certification acts as both an entry barrier and a demand qualifier.

ESG-conscious global corporations need certified recycled materials to meet their own sustainability commitments. Gravita’s ISO 14001 and ISCC credentials make it the default preferred supplier.

8. New Verticals Unlocked

Gravita is actively reducing lead concentration through acquisitions and new commissioning across copper, lithium, rubber, and steel. The RMIL acquisition for ₹561.84 crore is the largest deal in company history. Non-lead businesses are targeted at 35-40% of revenues by FY29, versus approximately 13% in FY26.

Gravita acquired 99.44% stake in Rashtriya Metal Industries Limited (RMIL) for ₹561.84 crore in FY26. RMIL’s Sarigam, Gujarat plant has 31,200 MTPA copper and alloy capacity.

RMIL reported ₹1,040 crore in revenue and ₹82 crore in EBITDA for FY26. The acquisition adds immediate P&L scale.

Founded in 1946, RMIL serves established electrical and defence sector customers. These are high-barrier, loyalty-heavy relationships built over decades. Gravita acquires a customer book alongside a plant.

The entire ₹561.84 crore acquisition was funded from Gravita’s liquid investment portfolio of approximately ₹737 crore.

Copper scrap-to-alloy capability enables backward integration, reduces supplier dependence, and creates cross-selling opportunities using RMIL’s existing customer base.

Lithium-ion battery recycling commenced at Mundra in FY26 with a 6,000 MTPA pilot plant. EV battery retirement volumes will peak in the late 2020s. First-mover market positioning, secured at low cost.

Rubber recycling is now operational in both Romania (FY25) and India (FY22). Two geographies, growing regulated demand, and no serious Indian competitor with comparable scale.

Steel recycling is the next listed vertical on the Vision 2030 roadmap. Each addition widens the scrap basket and diversifies revenue streams further.

9. Management and Governance

The management team averages 30+ years of industry experience, with 15-year average company association. CMD Rajat Agrawal has led Gravita since founding in 1992. Four ESOP rounds and 100% employee incentive coverage align compensation with outcomes across a 3,500-person global workforce.

CMD Rajat Agrawal founded Gravita in 1992 and has driven strategy for 33 consecutive years. Founder-led continuity over three decades is a compounding organizational asset.

Average management industry experience exceeds 30 years. Average management association with Gravita is 15 years. This team has navigated multiple commodity cycles together.

Four rounds of ESOPs have been issued. 100% of employees across the 3,500-person workforce are covered under incentive schemes.

The senior team includes a standalone CEO, CFO, and three Executive Directors leading specific business lines. Leadership depth enables the delegation that global scale requires.

The board maintains 50% independent directors. An ESG committee was created at the board level. No visible governance lag for a business operating in 14 countries.

Zero complaints of ethical breaches or statutory non-compliance were recorded across all plants in FY26. BRSR core indicator assurance was completed.

15 consecutive years of dividend payouts reflect a capital return culture that has held through volatile periods.

10. Risks and Red Flags

African operations in Mozambique, Senegal, and Tanzania carry political instability, currency volatility, and unpredictable regulatory risk. An FY25 disruption in Mozambique visibly dented overseas margins.

In Q3 FY26, aluminium volumes fell 43% YoY as scrap aggregators withheld feedstock during a period of high primary metal prices. No active aluminium hedging mechanism existed at the time.

The Labor Code implementation is expected to create ₹42 crore in total liability, with ₹35 crore being prior-period. Provisioned but not fully closed.

The ₹561.84 crore RMIL acquisition is the largest in Gravita’s history. Integrating copper scrap sourcing, customer migration, and operational culture across geographies takes time.

That’s it for today.

FINVEZTO.COM | One Wealth-Building System. For Life.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

I think this stock is overvalued as of now

Can you explain net cash flow some stocks having negative value is this good