Genus Power Infrastructures || Consistently Performing Stocks #70

What has led to the consistency?

Every week I analyze a company’s fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.

This week, Let’s explore the business & fundamentals of

Genus Power Infrastructures Ltd. NSE: GENUSPOWER

Performance Chart

Quality Chart

Their Road to Consistency

1. Overview and Business Model

Founded in 1992 in Jaipur, Genus has evolved from a conventional electricity meter manufacturer into India's leading end-to-end smart metering company. Its meters now measure over 20% of India's electricity consumption.

The company was founded in 1992 making basic electricity meters. Today it designs, manufactures, installs, and operates smart metering systems for state electricity utilities.

The business model shifted from selling meters once to operating them for 10 years. The company installs the full system, earns a fixed monthly fee per meter, and maintains the network for the contract duration. Install Once. Get a decade of recurring income.

Over 105 million meters are installed across India. The company’s devices measure more than 20% of India’s total electricity. That roughly covers 1 in 5 households nationwide.

The company is not just a hardware manufacturer. It employs 225+ software developers and 250+ device engineers managing proprietary software platforms that communicate with, read, and manage every installed meter remotely.

Annual manufacturing capacity now exceeds 18 million meters. 4 facilities in Jaipur, Haridwar, Guwahati, and Kotputli span nearly 1 million square feet. The scale was built in anticipation of a large policy push.

GIC, Singapore's sovereign wealth fund and one of the world's most sophisticated institutional investors, holds a 15.11% direct equity stake in Genus.

The NCLT sanctioned a demerger on April 24, 2025. The non-power investment business was spun off as a separate entity. What remains is a clean, focused business with no distractions on the balance sheet.

The company employs 16,800+ people and plans to add 2,200 more by 2027. Headcount growth is tracking order book execution.

The promoter family runs the company across 4 generations.

2. Policy Driven Demand

India’s Government launched a program to replace 250 million old electricity meters with new smart prepaid meters. The goal is to cut electricity theft and billing inefficiencies at state power distribution companies. At approximately ₹8,000 per meter, the total opportunity works out to ₹1,28,000 crore. This policy is the demand engine.

As of January 31, 2026, 22.4 crore meters had been approved under this national program. Only 5.5 crore have been physically installed. The gap between approved and installed is future revenue for companies executing these projects.

Bihar’s electricity theft and billing losses fell from 19.94% in FY24 to 15.5% in FY25 after smart meter rollout. Assam’s losses dropped from 23.39% in FY20 to 15.74% in FY24.

The Assam project covers 57.45 lakh meters for the state electricity utility. The Bihar project covers 1.03 crore meters under a separate government structure. Both are among the largest active smart meter rollouts in India.

Larger states like Uttar Pradesh, Tamil Nadu, and Maharashtra have approved the highest meter volumes. But installation pace is slower. Gujarat saw public protests in Vadodara, Rajkot, and Jamnagar over unexpected billing changes.

Their Joint MD stated that only 15.6 crore meters of India’s 31-32 crore requirement have been formally tendered so far. More than half the market has not yet been put out to bid.

Each smart metering contract is structured as an 8-10 year arrangement. The executing company installs meters upfront and then earns a monthly fee per meter for the full contract period.

Central government funding bodies provide financial support to state electricity utilities for smart meter procurement. This reduces credit risk for executing companies.

3. GIC Platform Architecture

In July 2023, the company structured a $2 billion JV with GIC, Singapore’s sovereign wealth fund. GIC owns 74% of the operational platform. The company owns 26%. The company is the exclusive project executor and meter supplier.

The joint venture keeps large project-specific debt off the parent company’s balance sheet. GIC funds the equity. The company earns fees for supplying meters, installing the systems, and maintaining them over 10 years.

Approximately 80% of the platform’s project value flows back to the company as revenue. The installation phase, spanning roughly 27 months, contributes 55-58% of order value. The maintenance and operations phase, covering the remaining 93 months, contributes 20-22%.

When a new project is bid, a dedicated project company is first set up as a subsidiary of the parent. Once the bid is won and execution begins, this entity transfers to the joint venture platform.

As of March 31, 2026, ₹23,361 crore of the ₹25,173 crore total order book belongs to projects under this joint venture platform. That is 93% of the total order book. The joint venture is the primary revenue engine for the next 7-8 years.

State electricity utilities in India have a long history of payment delays. This company solved that structurally. Utility payments are legally routed into a ring-fenced account before the utility can spend that cash elsewhere. The company collects from a protected pool, not from a utility's general treasury.

The US International Development Finance Corporation, the US government's development finance arm, invested $49.5 million directly into the company. The DFC applies rigorous governance and operational standards before committing capital. That bar is not easy to clear.

Beyond the joint venture, the company can sell meters to other smart metering operators as an independent manufacturer. Competitors executing their own projects can buy meters from this company.

4. Order Book Visibility

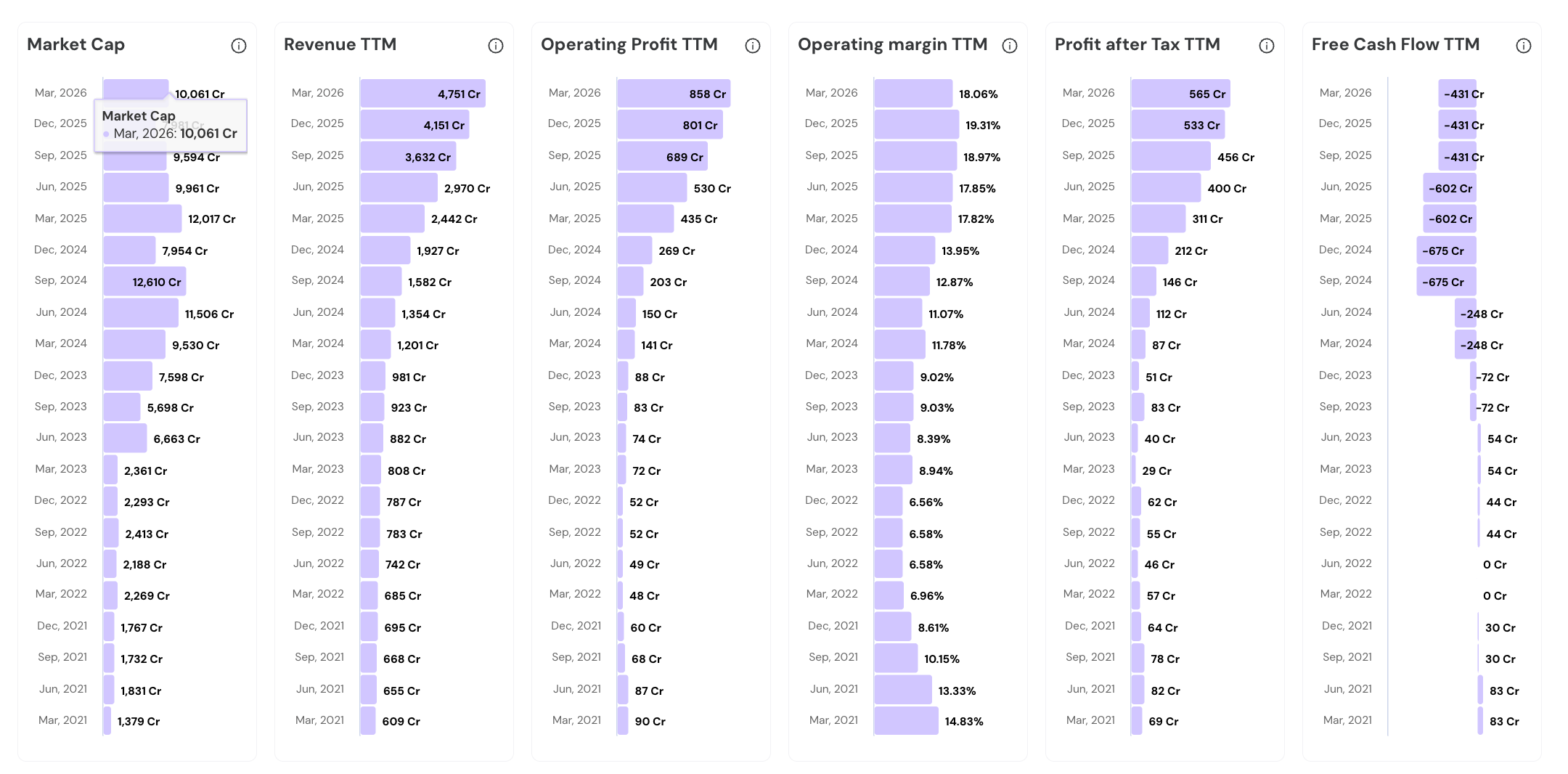

The total executable order book stood at ₹25,173 crore as of March 31, 2026. Orderbook has grown from ₹931 crore in March 2021, a 27x increase in five years. This is approximately 2.7x the company’s market capitalization of ₹9,309 crore.

Order book trajectory: ₹931 crore (March 2021), ₹4,115 crore (March 2023), ₹30,110 crore (March 2025), ₹25,173 crore (March 2026). The FY26 dip from FY25’s peak reflects execution converting orders into revenue.

An order book at 5.3x FY26 standalone revenue offers futuristic revenue visibility. Even at 30% annual growth, the current order book extends coverage well into FY29.

₹23,361 crore of the order book sits within the GIC joint venture structure. These are long-concession contracts spanning 8-10 years.

National program data shows only 5.5 crore of 22.4 crore approved meters have been installed nationally. The company has installed over 1 crore. Substantial new order potential remains within the already-approved universe.

Management plans to install 1 crore smart meters in FY27 alone. That matches cumulative installation across prior years combined. Execution velocity is doubling year-on-year. This is the most important operational metric to watch going into FY27.

The Bihar and Assam anchor projects are live and billing. Order book credibility is backed by active execution in the field.

5. Full-Stack Integration

The company is one of very few operators in India that owns every layer of a smart metering project. It manufactures the meters. It builds the communication network that connects them. It runs the central software that reads and manages the meters remotely. It processes the data into billing and consumption insights for the utility. End-to-end ownership is an edge in large government tenders.

Large government smart metering tenders require demonstrating hardware and software capabilities under a single entity. This company builds meters for residential, commercial, industrial, and grid-level applications in-house.

The central software platform that communicates with all installed meters can work across multiple network technologies, including cellular and wireless connections, in a single deployment. It also integrates meters made by other manufacturers. This flexibility reduces long-term project cost significantly.

The data management layer processes raw meter readings and converts them into billing data, energy audits, prepaid recharge systems, and consumption analytics for utility operators. Both the communication software and data software are built in-house.

The business model involves the company funding the full project cost upfront, including meters, communication hardware, and software setup. It then recovers this investment over a 10-year period through monthly per-meter service fees. Higher upfront risk, but significantly higher lifetime revenue per project.

Over 1 million meters are actively managed by the company’s proprietary software platforms. Software revenue from licensing these platforms to other operators and utility companies is capital-light. Every additional client contributes near-zero marginal cost revenue.

6. Manufacturing Muscle

The manufacturing base spans 4 facilities with combined annual capacity exceeding 18 million meters across nearly 1 million square feet. The newest Kotputli plant in Rajasthan, which started commercial production in February 2026, makes the plastic meter casings in-house, reducing dependence on external suppliers and protecting the company’s proprietary product designs from replication.

Making meter casings internally reduces freight costs and prevents design copying by competitors.

4 manufacturing locations spread across Rajasthan, Uttarakhand, and Assam reduce single-site concentration risk. Positioning capacity closer to major project geographies also reduces logistics cost and delivery timelines on large state-level rollouts.

The factory infrastructure includes dedicated clean rooms, precision electronic assembly lines, automated testing stations, and plastic molding machinery. This is proper electronics-grade manufacturing with the same standards as consumer electronics factories.

The government-recognized R&D center has a hardware team of 250+ engineers focused on meter design. A software team of 225+ developers focuses on the communication and data management platforms. 2 separate R&D teams build technology that gets stronger with each cycle.

Over ₹150 crore has been invested in R&D over recent years. Combined development experience in the software team alone exceeds 450 years.

The company secured a $49.5 million investment from the US International Development Finance Corporation specifically to expand its manufacturing and deployment capacity.

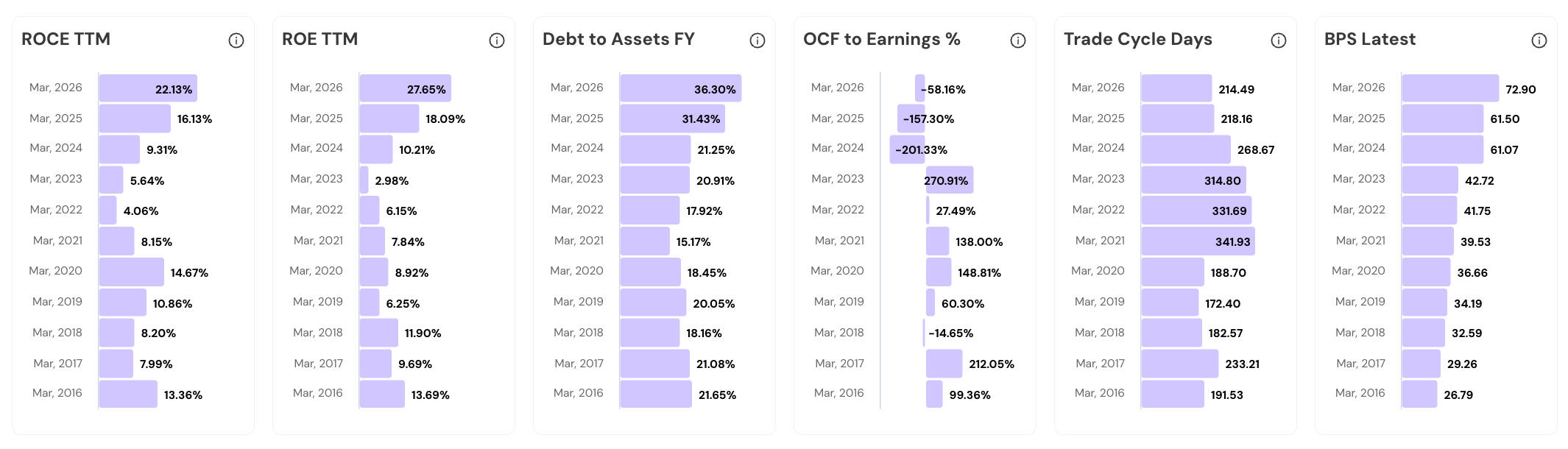

7. Working Capital Improving

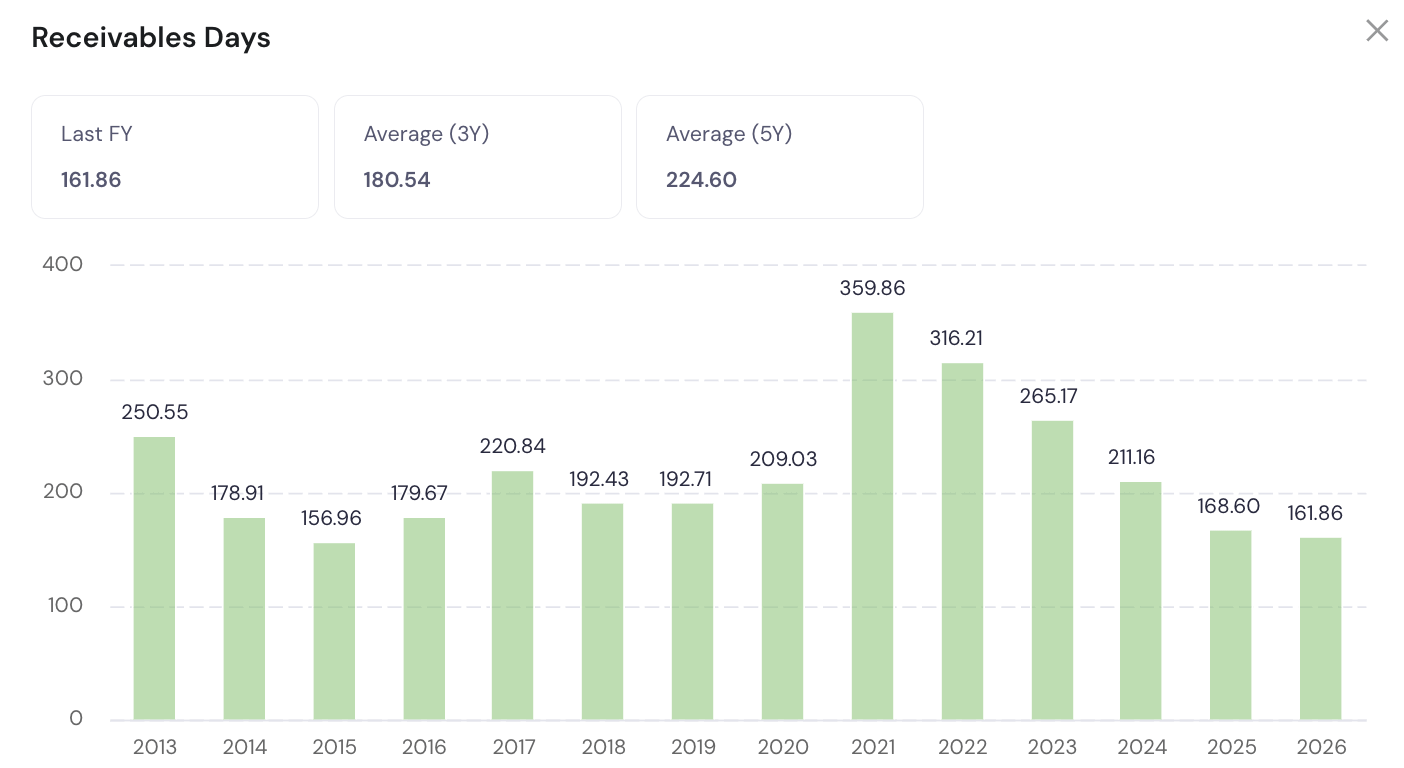

The joint venture project structure is systematically improving cash collection timelines. The number of days taken to collect payment after invoicing is falling consistently. A good signal.

Days to collect payment from customers has been falling. The direction is steep and consistent. Management targets 75-80 days by FY27. If the trajectory holds, this is a fundamental improvement in cash conversion quality.

Under the joint venture structure, project companies pay the parent within 90-120 days after invoicing. This is structurally faster than the old model of billing state electricity utilities directly.

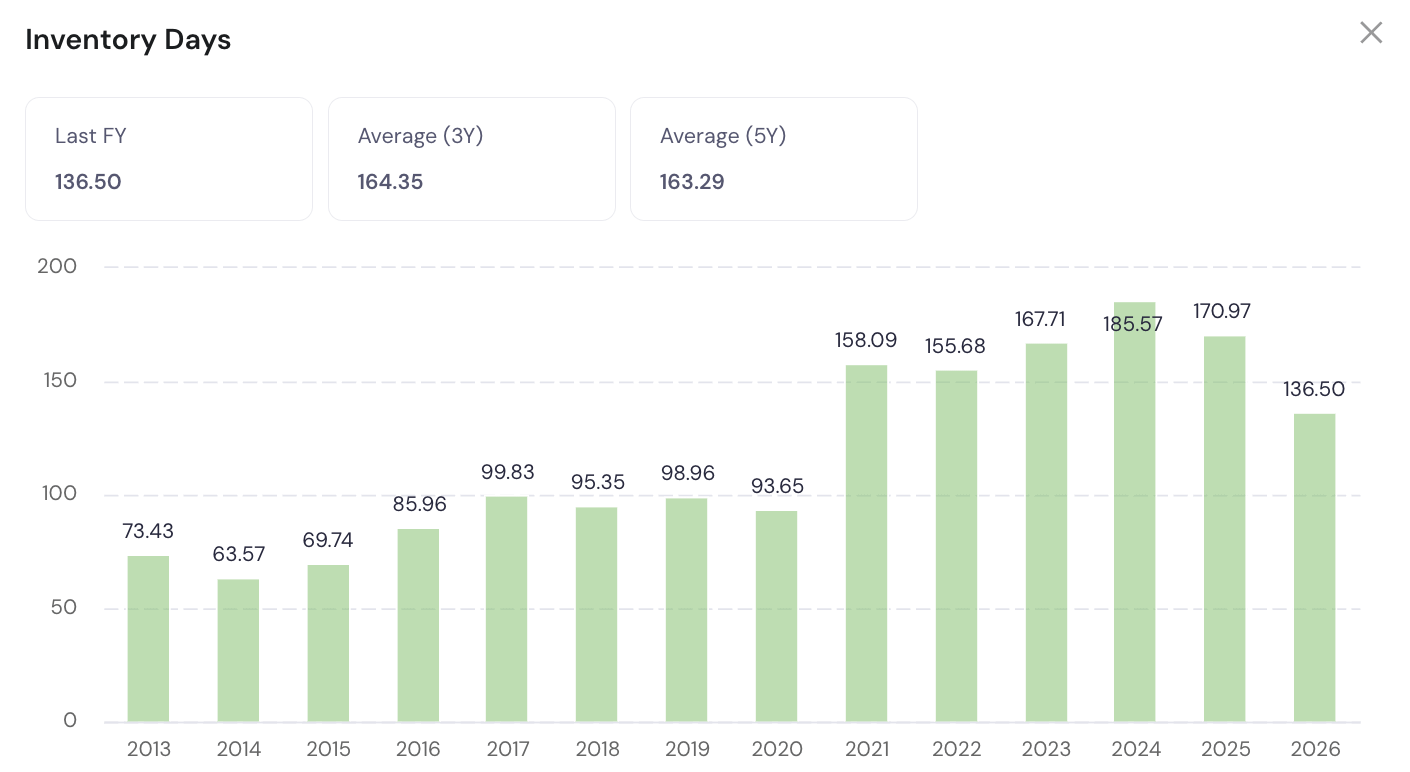

Inventory days remain elevated at 104 (March 2026) because multi-state rollouts require pre-positioned materials and communication hardware across multiple project locations.

Net debt rose from ₹605 crore (March 2025) to ₹1,573 crore (March 2026). This is almost entirely short-term working capital borrowings. Peak net debt is expected around ₹1,900-2,000 crore in FY27.

Payments from state electricity utilities are routed directly into dedicated project bank accounts. These accounts must always maintain a cash buffer equal to five times the monthly fee due. Revenue distributions to the parent begin only after certified performance milestones are met.

The joint venture has received cumulative equity infusions of ₹487 crore by March 2026, projected to reach ₹1,100 crore by FY27. This is the capital investment phase. Cash generation begins in FY28. The company is in year three of a 10-year concession lifecycle.

8. Adjacencies and Exports

Beyond electricity metering, the company is building positions in smart gas meters, smart water meters, and export markets. India alone targets 12 crore gas connections by 2030. The domestic gas metering opportunity could require 12 crore smart gas meters over 6-7 years. Globally, water utilities are projected to spend USD 340 billion on digital transformation over the next 10 years.

India’s government targets gas to account for 15% of the national energy mix by 2030. Accurate billing for gas requires smart meters similar to electricity meters. The company is India’s only manufacturer with British Standards certification for gas meters.

12 crore gas meter installations over 6-7 years is a market potentially as large as the current electricity smart metering cycle. Existing relationships with state utility operators create a natural channel to cross-sell gas meters.

Smart water meters address non-revenue water losses, regulatory requirements, and environmental compliance for municipalities. Global water utility digitization spending is projected at USD 340 billion over 10 years.

Export markets in the Middle East, Africa, and Asia-Pacific are being developed. Rapid urbanization and infrastructure investment in these regions drive demand for integrated metering solutions.

The communication and data management software platforms can be licensed to other smart metering operators and utility companies globally. This is intellectual property revenue.

The first wave of smart meter installations in Europe and the United States is approaching end-of-lifecycle. A second replacement cycle is emerging. Indian manufacturers with globally certified, compatible products are positioned for this cycle.

9. Risks and Concerns

Net debt rose from ₹605 crore (March 2025) to ₹1,573 crore (March 2026). Peak net debt is expected near ₹2,000 crore in FY27. These are short-term working capital borrowings. Any credit tightening or interest rate spike directly increases costs and squeezes near-term margins.

Operating profit margin is guided to compress to approximately 18% in FY27, down from 20.3% in FY26. A higher share of installation-phase revenue versus pure meter supply drives this compression. Margin recovery is dependent on FY28 as more projects shift to the recurring maintenance phase.

40-45% of smart meter components, primarily the chips and processing units that make meters smart, are imported. Fixed-price contracts with state utilities make cost recovery difficult when input costs rise. Global semiconductor supply chains remain volatile.

Promoters have pledged a portion of their shareholding, representing approximately 2.11% of total outstanding equity. In absolute terms this is not high.

Larger states with the highest approved meter volumes are the slowest in actual deployment. Gujarat saw public protests over unexpected billing changes during rollout. State government cooperation and utility execution capacity vary significantly across India. Revenue velocity depends partly on factors outside the company’s control.

Free cash flow has been negative across FY24-FY26 due to ongoing investment into joint venture projects. Cash generation begins in FY28 as projects enter recurring billing phases. Investors need patience for the cash cycle to turn.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.