Cupid Ltd || Consistently Performing Stocks #53

What has led to the consistency?

Each week I analyze one company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.This week, Let’s explore the business & fundamentals of Cupid Ltd.

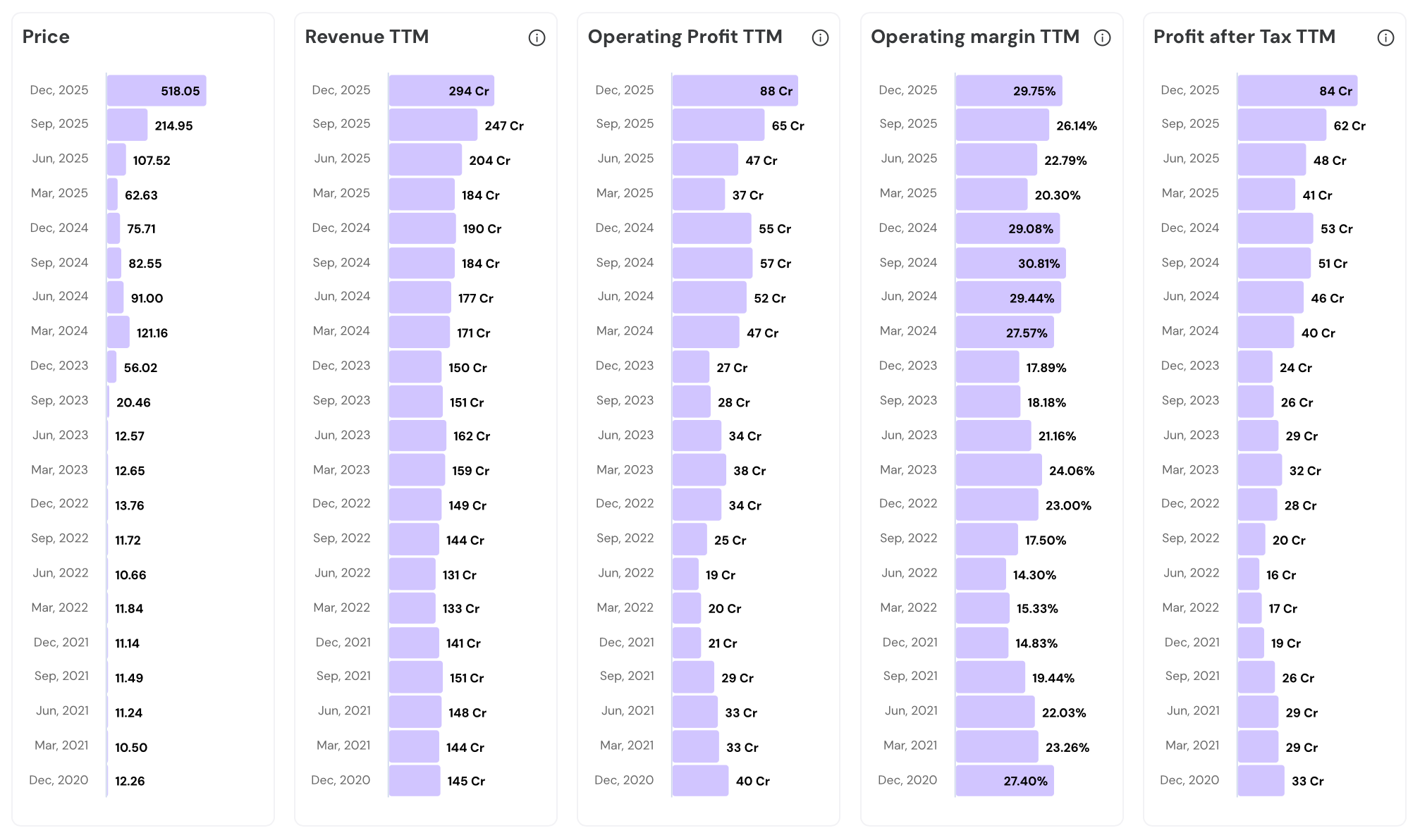

In the last 5 years…

- Stock price has grown 42.3 times (from 12.26 to 518.05)

- Revenue has grown 2.0 times (from 145 Cr to 294 Cr)

- Operating profit has grown 2.2 times (from 40 Cr to 88 Cr)

- PAT has surged 2.5 times (from 33 Cr to 84 Cr)

Take a look at the chart below.

Their Road to Consistency

1. Cupid’s Business Model

Cupid Limited, incorporated in February 1993 as Cupid Rubbers Limited in Nashik, Maharashtra, is a sexual and reproductive health products manufacturer. It is gradually evolving into a broader FMCG consumer wellness platform.

The company operates from a state-of-the-art facility at MIDC Sinnar, Nashik, roughly 200 km east of Mumbai.

The facility is equipped with German-imported machinery. It is capable of producing 480 million male condoms, 52 million female condoms, and 210 million lubricant sachets annually.

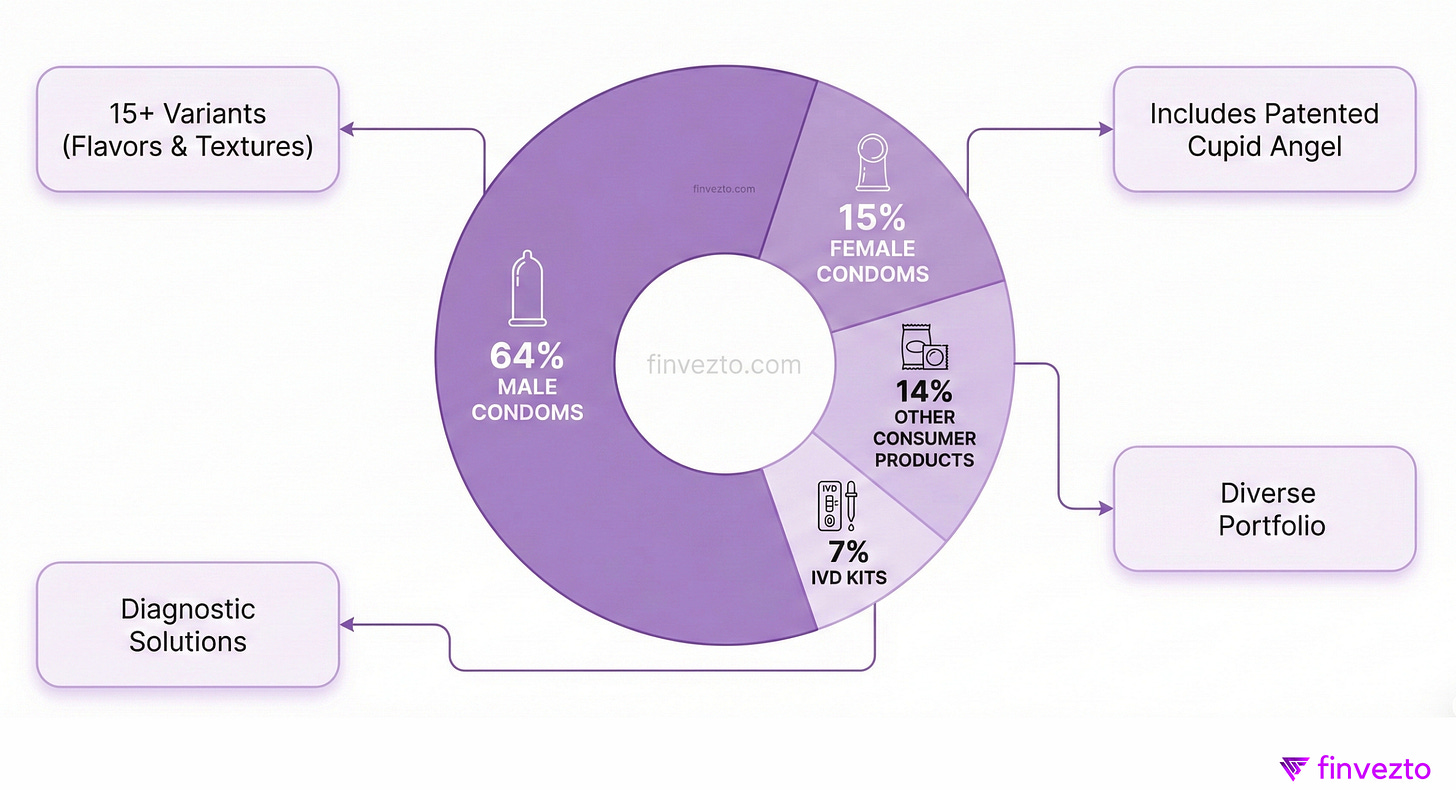

The company manufactures 15+ male condom variants across flavors and textures, plus female condoms including the patented Cupid Angel design.

Recent Product mix showed male condoms at ~64% revenue, female condoms ~15%, IVD kits ~7%, and other consumer products ~14%.

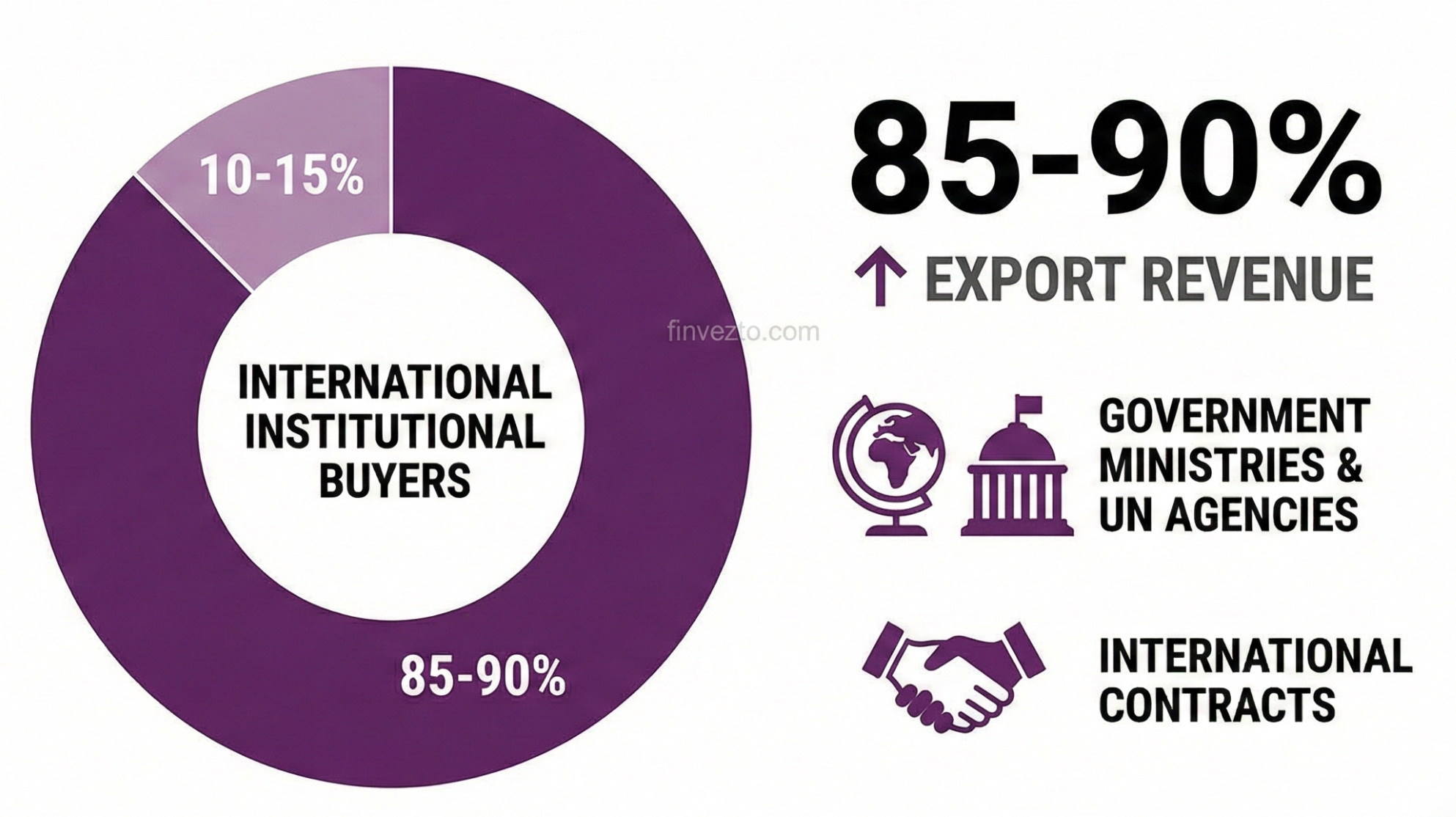

Cupid’s revenue is export-heavy with 85 to 90% coming from international institutional buyers like government ministries and UN agencies. This B2B focus creates stability. Quite different from consumer brands volatility.

Key institutional customers include UNFPA, South African Ministry of Health, Tanzania’s Medical Stores Department, and Brazil’s health ministry. These relationships span decades.

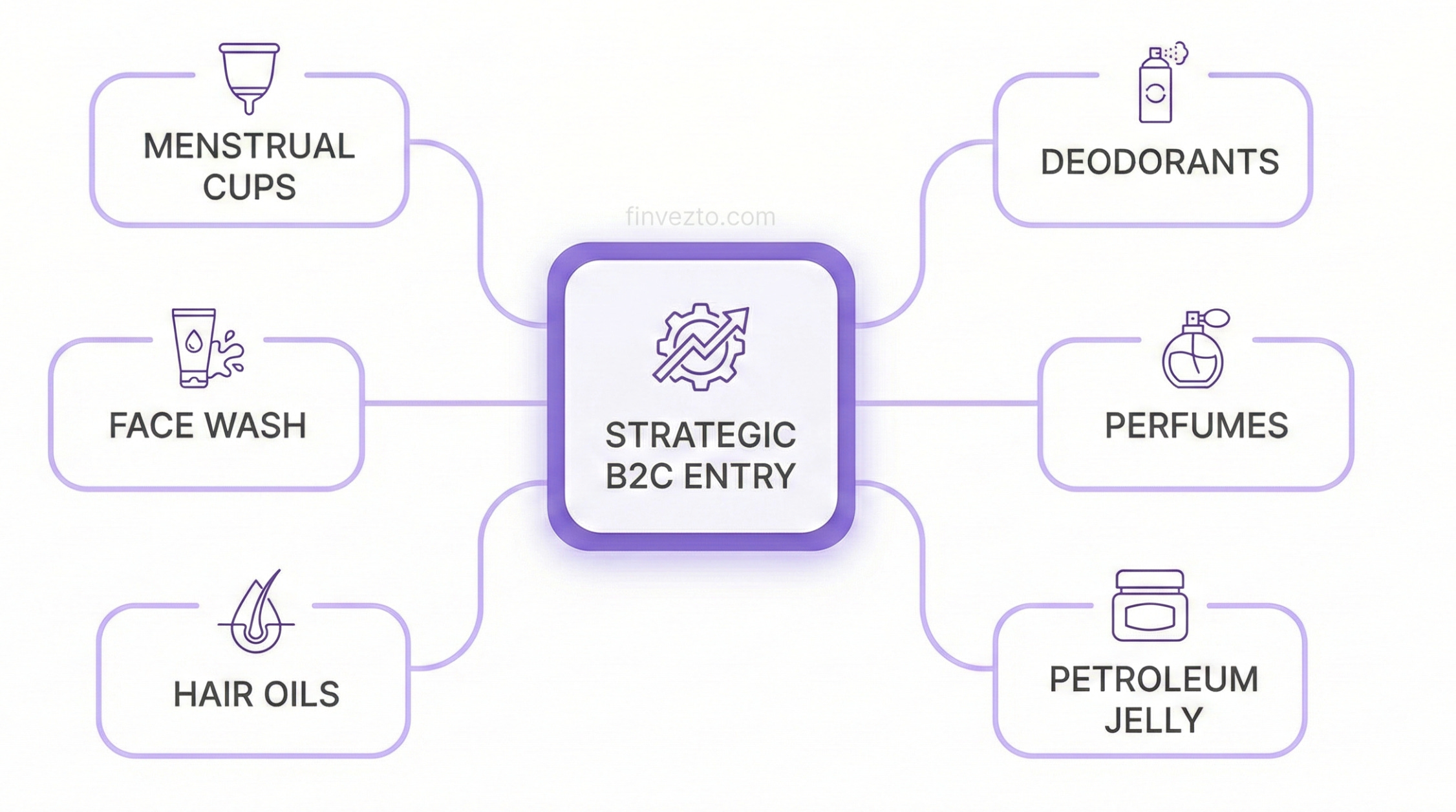

Since FY25, Cupid aggressively entered B2C with deodorants, perfumes, petroleum jelly, hair oils, face wash, and menstrual cups. Bold pivot into FMCG.

2. Dual Prequalification Moat

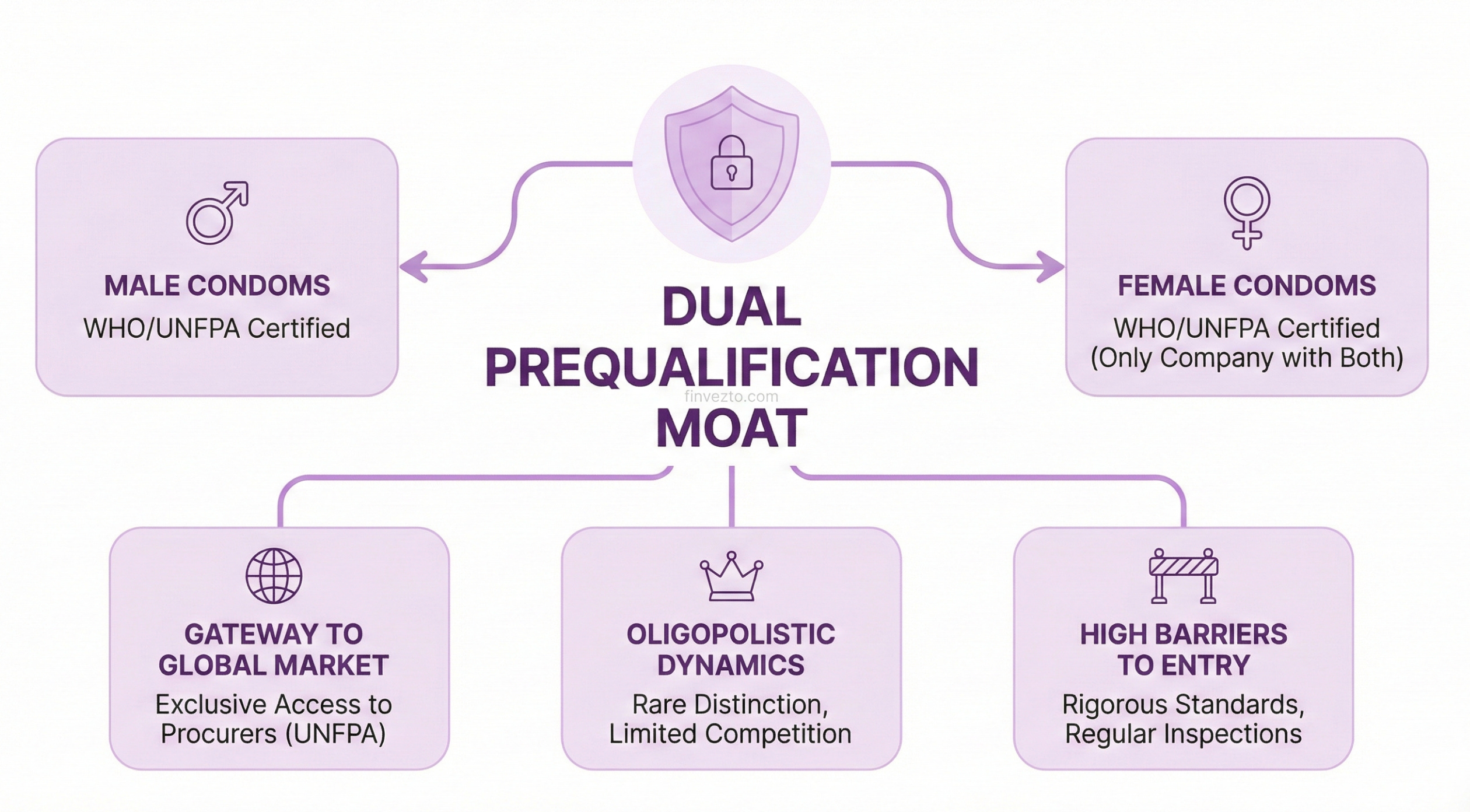

The single most powerful driver of Cupid’s consistent performance is its WHO/UNFPA prequalification for both male and female condoms. A distinction no other company in the world holds. This certification is the gateway to the global institutional contraceptive market. UNFPA, the world’s largest public-sector procurer of contraceptives purchases exclusively from prequalified manufacturers such as CUPID.

Only 22 manufacturing sites globally hold WHO/UNFPA prequalification for male condoms, and just three for female condoms worldwide. This creates oligopolistic dynamics.

Cupid achieved female condom prequalification in 2018, becoming the first Indian and second global manufacturer to do so.

In Jan 2025, Cupid obtained WHO/UNFPA prequalification for its Brown Caramel female condom variant, making it eligible for 100% of South Africa’s tender.

The prequalification process demands ISO 4074 compliance, WHO Technical Report Series specs, GMP standards, and rigorous facility inspections every 3 years. Barriers to entry are high in this business.

Beyond UNFPA prequalification, Cupid holds ISO 9001:2015, ISO 13485:2016, CE marking, SABS certification, Brazil’s ANVISA approval, and VEGAN certification.

The company is pursuing USFDA 510(k) resubmission for Version 3 Female Condom, which would unlock the lucrative US market.

Institutional buyers heavily weight regulatory compliance in tender evaluations, giving certified incumbents structural advantages.

3. Global Export Engine

Cupid’s export spans 110+ countries across Africa, Latin America, Asia-Pacific, Europe, the Middle East, and CIS nations. This is a critical consistency driver because geographic diversification insulates the company from dependence on any single market. Also, Exports have historically accounted for 80 to 90% of their revenue.

The South Africa 5-year national condom program allocates Cupid 23.4 million female condoms yearly and 153 million male condoms annually through 2030. This provides ₹115 crore annual visibility.

The South Africa procurement started in Dec 2025 with deliveries across strawberry, vanilla, caramel, banana, and grape flavors. Even institutional buyers care about flavor variety.

Tanzania’s Medical Stores Department placed a ₹42 crore order in Feb 2025 for male condoms. In Jan, they had placed orders worth ₹15 crores. Repeat orders signal deepening relationships.

Cupid won L1 position in a Brazilian government tender for 6.25 million female condoms valued at approximately ₹40 crore with future orders expected.

By mid-2025, B2B export order book crossed ₹100 crore, the highest in company history.

In October 2025, Cupid received Maharashtra State Export Award 2025 for outstanding export performance in healthcare and wellness products.

4. Female Condom Leadership

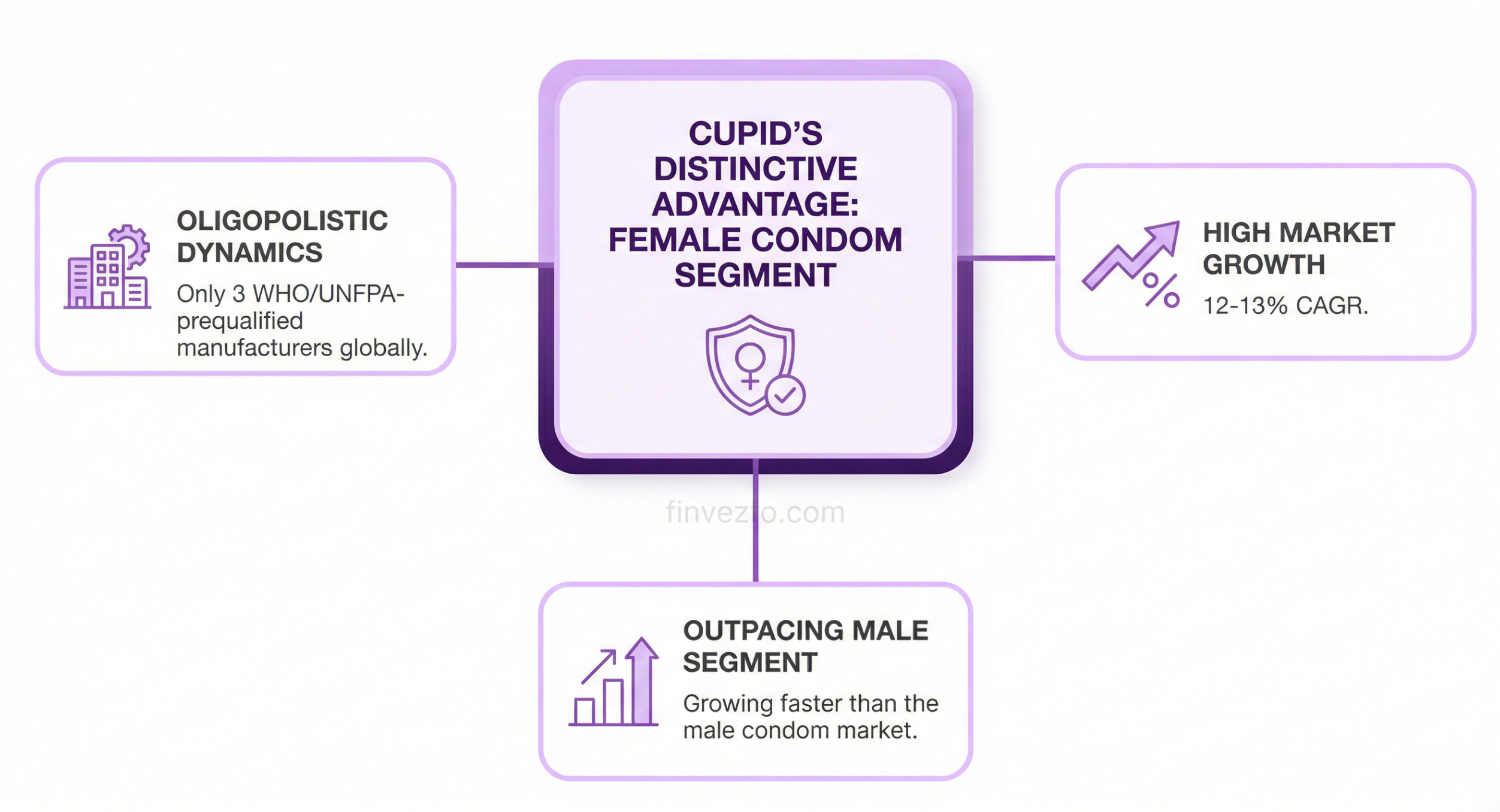

The female condom segment is arguably Cupid’s most distinctive competitive advantage. With only 3 WHO/UNFPA-prequalified manufacturers globally, Cupid operates in a market with natural oligopolistic dynamics. Also, this market has a growth rate of 12-13% CAGR. Growing Ffster than the male condom market.

Female condoms serve a critical public health function as the only female-initiated barrier method against both pregnancy and STIs. This is central to women empowerment programs funded by UNFPA, USAID, and PEPFAR.

Cupid secured 59% of South Africa’s total female condom allocation, winning 23.4 million units out of 40 million total available. Market share dominance in tenders.

Cupid manufactures FC-1 and Cupid Angel designs, with Angel featuring a patented sponge-based insertion mechanism for improved comfort. Product innovation differentiates even in commodity markets.

Version 3 ring-variant female condom development is underway. Continuous product pipeline improvements are being made.

5. Institutional Relationships

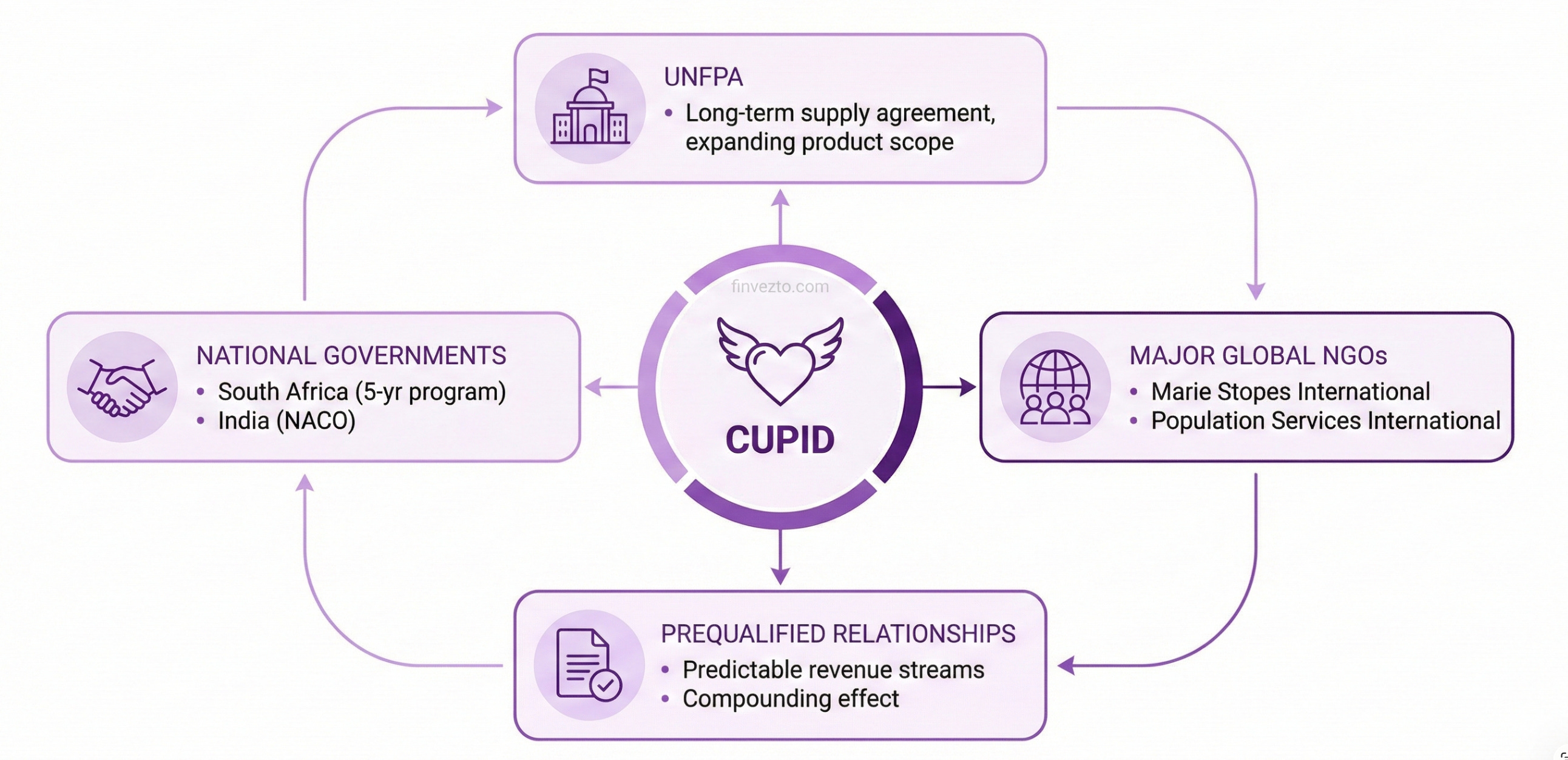

Winning a UNFPA contract or a national government tender requires years of prequalification, facility audits, sample approvals, and performance track records. Once established, these relationships tend to be remarkably sticky.

Cupid maintains a long-term supply agreement with UNFPA, which placed an ₹18.20 crore purchase order in Dec 2024. Multi-year frameworks provide predictable revenue streams.

UNFPA restarted procurement of Cupid’s lubricant products in Q3 FY25, indicating expanding product scope within existing relationships. Cross-selling to Institutions.

Their South Africa relationship began with first export order in 2010 and deepened over 15 years. It has culminated in the ₹575 crore 5-year program.

Beyond direct government tenders, Cupid supplies major global NGOs including Marie Stopes International and Population Services International operating across developing nations.

The company serves India’s National AIDS Control Programme through NACO’s condom social marketing initiative as well.

Their record-high order book reflects compounding effect of winning repeat contracts across multiple geographies.

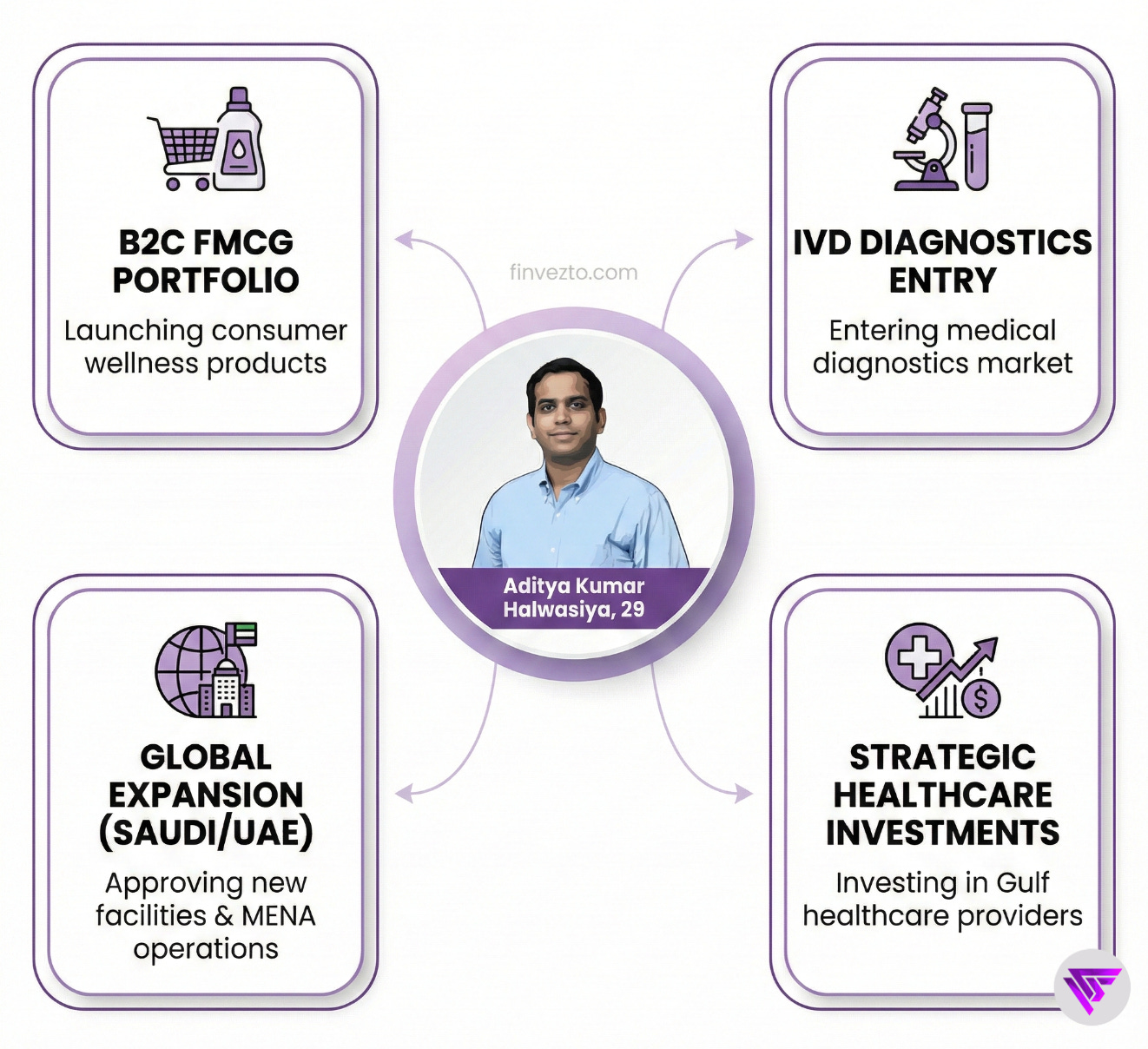

6. A Young Promoter’s Vision

The Oct 2023 management transition represents a pivotal inflection point in Cupid’s trajectory. Aditya Kumar Halwasiya, a 30 year old entrepreneur from the Universal-Halwasiya Group (a Kolkata-based conglomerate with interests in petroleum products and real estate) acquired 41.84% of the company from founding promoter Omprakash Garg.

Halwasiya’s vision transforms Cupid from niche B2B condom exporter into diversified consumer wellness and health-tech company.

At the recent AGM, he stated Cupid is no longer just a contraceptive company but a consumer wellness and health-tech leader.

Concrete actions include launching B2C FMCG portfolio, entering IVD diagnostics, approving Saudi Arabia facility, and establishing UAE subsidiary for MENA operations.

Halwasiya invested in Saudi-based healthcare provider through Gulf Islamic Investments with AUM over USD 3.5 billion and pursued stake in Mansam luxury fragrance brand.

He consistently increased personal stake through open market purchases, taking promoter holding from 41.84% to 45.55% by September 2025.

The stock has shot up big time after Mr. Halwasiya jumped in. Skin in the game working its magic, or something else going on? Only time will tell.

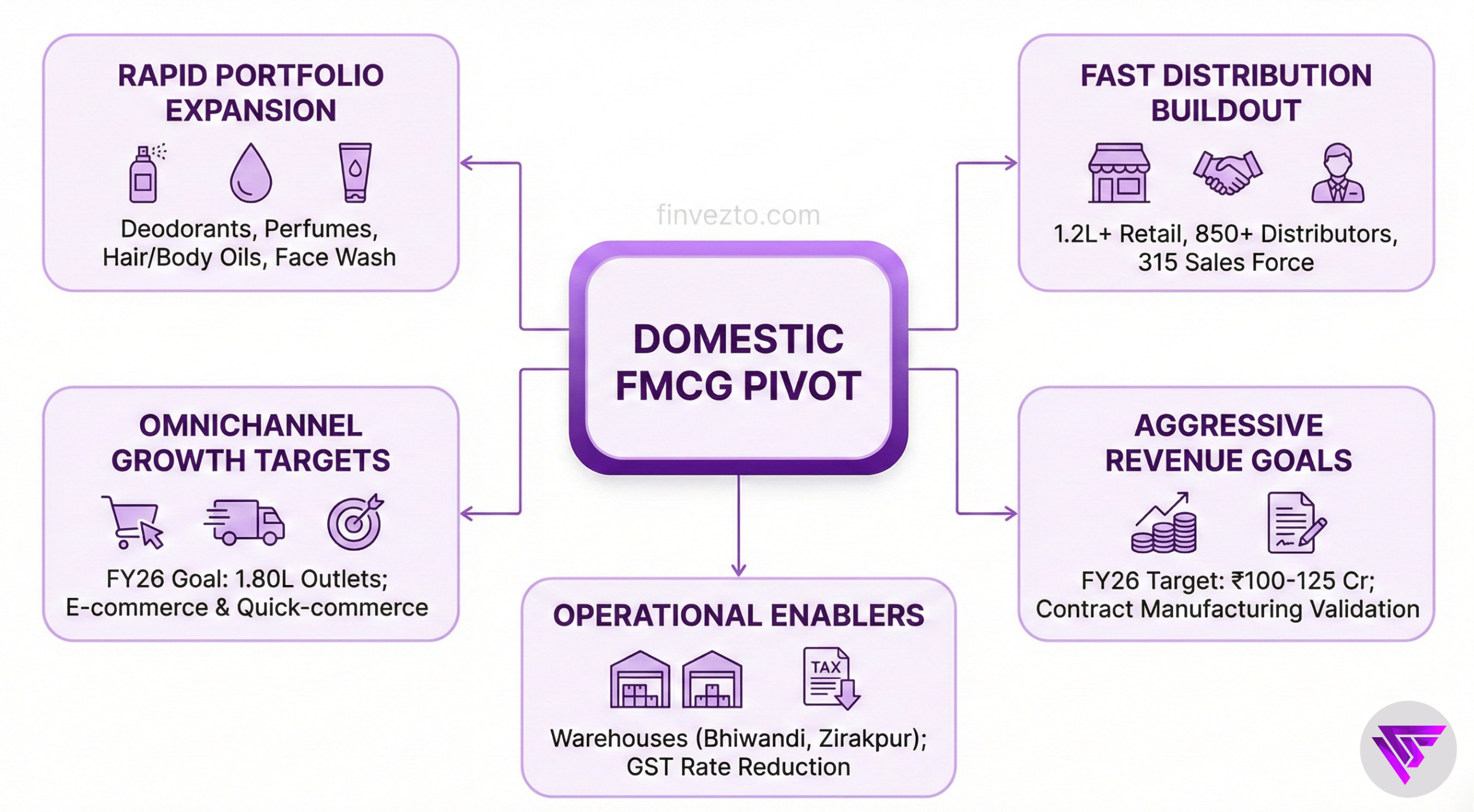

7. Domestic FMCG Pivot

As mentioned earlier, Cupid’s most significant strategic departure under new management is the aggressive entry into domestic B2C consumer products. CUPID launched its FMCG vertical in Mar 2024 with deodorants and pocket perfumes. Then it rapidly expanding to perfumes, hair oil, body oils, petroleum moisturizing jelly, face wash etc.

As of mid-2025, Cupid established 1.20 lakh+ retail touchpoints across India, supported by 55+ super stockists, 850+ distributors, and 315-member sales force. Distribution buildout happened remarkably fast.

Targets to reach 1.80 lakh outlets by end of FY26, with e-commerce presence on Amazon, Flipkart, BigBasket, and 1mg. Quick-commerce partnerships with Blinkit and Zepto underway. Omnichannel approach.

The company held distributor engagement event called AARAMBH in Hyderabad.

Established mother warehouse in Bhiwandi plus secondary warehouse in Zirakpur for pan-India distribution.

Revenue targets are aggressive with ₹60 crore targeted in FY25 and ₹100 to 125 crore in FY26 from this segment alone.

Recent GST changes reduced rates on products including hair oils, face wash, and IVD kits, creating regulatory tailwind for newest product categories.

Contract manufacturing for marquee clients such as Cipla Health and Godrej Consumer Products validates manufacturing quality and opens another revenue stream beyond owned brands.

8. Diagnostics Segment Growth

Cupid launched commercial IVD operations in 2023 after obtaining ISO 13485 certification, creating a diagnostics vertical. The portfolio now includes 15 IVD kits under the CupiKit and CupiSure brands: pregnancy detection, HIV 1&2, dengue IgG/IgM, malaria Pf-Pv, hepatitis B and C, syphilis, typhoid, COVID-19 antigen, LH ovulation, and urine test strips.

The IVD business contributed ₹12.85 crore in FY25, representing 7% of revenue, and turned PAT-positive within two years of commercial launch.

Current manufacturing capacity stands at 20 to 30 million kits annually, with automation of IVD production underway to scale capacity significantly.

In October 2025, Cupid received CE certification for CupiSURE Pregnancy Test Kit and CupiKIT Syphilis Antibody Test Kit, enabling European Economic Area distribution from Q4 FY26.

In January 2026, CE certification extended to CupiKIT HIV and Hepatitis B kits under stringent EU IVDR framework.

WHO prequalification for Malaria Pf-Pv kit expected by Q4 FY26, particularly significant given malaria diagnostic demand concentrates in African and Asian markets.

IVD kits already exported to Tanzania, Liberia, Ghana, Nepal, and the Philippines, leveraging existing institutional relationships and distribution infrastructure.

9. Continuous Expansion

Cupid’s current Nashik facility, with 480 million male condoms and 52 million female condoms annual capacity, has served the company well for 3 decades. But with order books at all-time highs and FY26 revenue on track to nearly double FY25, they have significantly increased their capacity.

In March 2024, Cupid acquired land in Palava, Maharashtra for 170,000 square-foot facility adding 770 million male and 75 million female condoms annually.

Construction progresses on schedule. Mid-2026 operational timeline looks achievable as mentioned by management.

The plant will also support FMCG and diagnostics production.

Expansion is funded entirely through internal accruals with no debt required.

On December 29, 2025 board approved Cupid’s first manufacturing facility outside India in Saudi Arabia targeting GCC region’s ~$70 billion consumer packaged goods market.

The FMCG plant will produce personal care products for Middle Eastern consumers.

10. Summary: Growth & Consistency Drivers

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

We give you a proven Flexi-Wealth System to build a Resilient Portfolio that works across market cycles. We believe your Wealth should be flexible enough to give you more options throughout your life. Learn more about the system at finvezto.com

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. We do not recommend buying or selling stocks mentioned in this newsletter. Securities market investments carry market risks. Kindly review all related documents before investing.

The company is a great company with solid fundamentals.

Om Prakash Garg is the founder of Cupid Limited.

In September 2023, Aditya Kumar Halwasiya acquired a controlling stake from the outgoing promoter.

But the promoter(Aditya Kumar Halwasiya) brother's(Ajay Halwasiya) partner (Hari Shankar Tibrewal ) involved in Mahadev betting app scam.

Analysts have noted that companies managed by the Halwasiyas, such as Cupid Ltd and Tourism Finance Corporation of India, experienced sharp stock price movements that coincided with the revelation of Tibrewal’s involvement in the betting scam.

According to me, Promoter quality is on toss.

PE of 140 is crazy.