CMS Info Systems Ltd || Consistently Performing Stocks #68

What has led to the consistency?

Every week I analyze a company’s fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.

This week, Let’s explore the business & fundamentals of CMS Info Systems Ltd. NSE: CMSINFO

Performance Chart

Quality Chart

Their Road to Consistency

1. Overview and Business Model

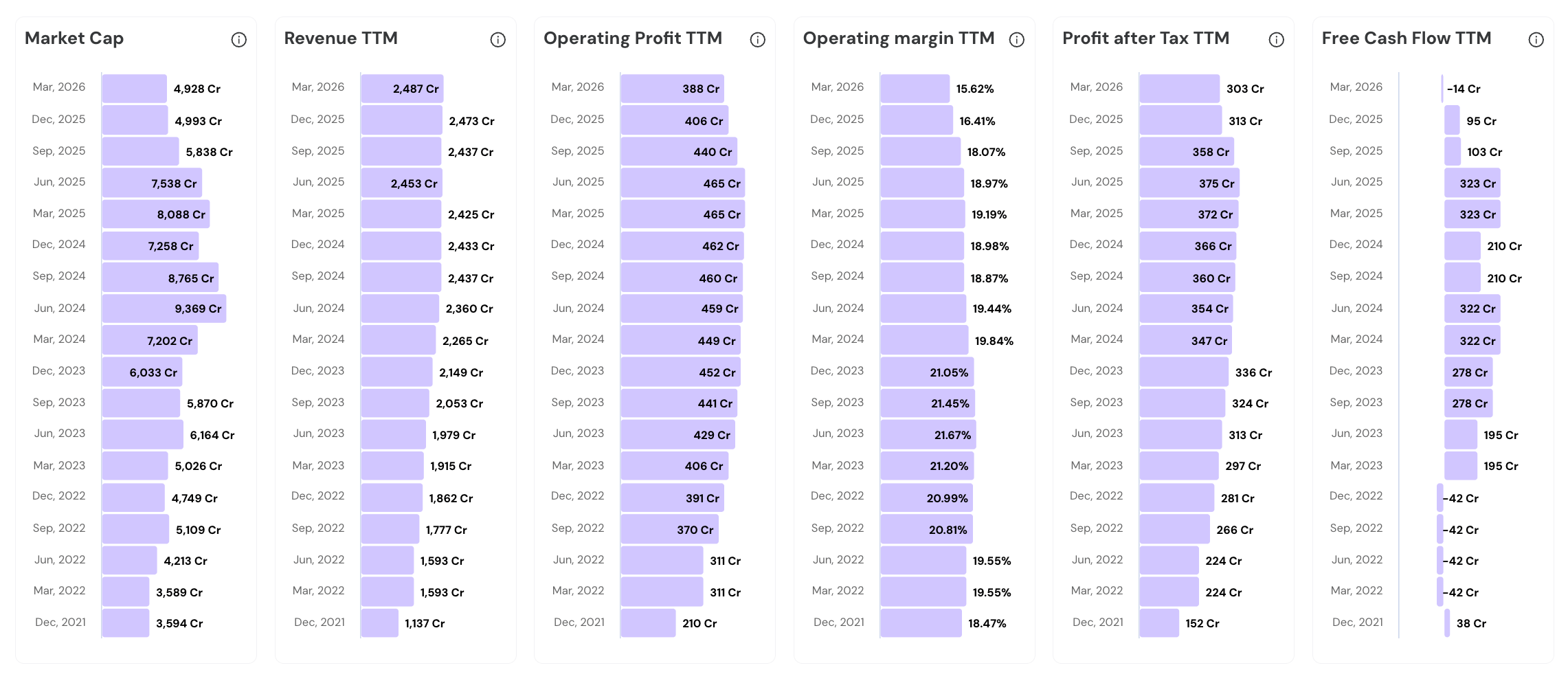

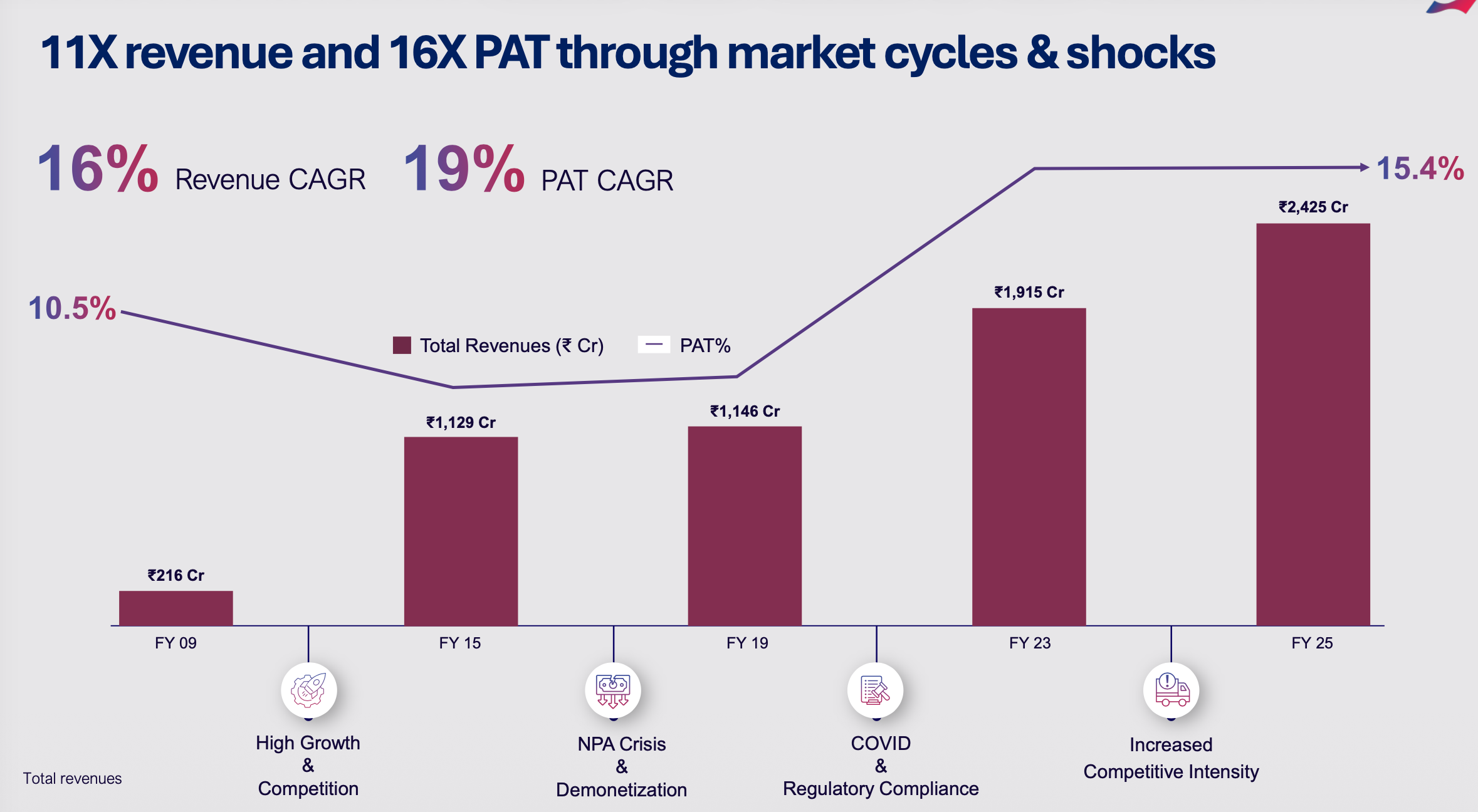

CMS Info Systems is the invisible infrastructure layer of India’s physical financial system. It manages ATM replenishment, retail cash automation, and banking technology end-to-end. Revenue grew from ₹1,306 crore in FY21 to ₹2,425 crore in FY25, a 17% CAGR. Profits compounded faster at 22%.

The 3 segments above drive the business.

CMS earns through recurring service fees charged to banks and retailers. Fees cover cash pickups, ATM replenishment, machine maintenance, and software subscriptions. Revenue is annuity-based by architecture.

Their core clients are India’s largest banks. SBI, ICICI Bank, and HDFC Bank. Insurance companies, e-commerce firms, airlines, and retail chains are growing rapidly in the mix.

CMS covers 97% of India’s districts. No competitor has assembled a comparable national footprint. Geographic depth is the single hardest competitive asset to replicate in this industry.

Net profit grew from ₹151 crore in FY21 to ₹373 crore in FY25, a 2.5x increase. Revenue grew 1.86x in the same period.

Card Personalization produces over 10 million payment cards annually from a certified Chennai facility. India has over 105 Crore cards in circulation. Every new bank account opened is a potential card order.

Once a bank integrates CMS into its ATM network or a retailer into its cash cycle, migrating away is operationally disruptive. Stickiness is engineered into every client relationship.

2. Unmatched Physical Reach

CMS has assembled a physical network that took over 16 years to build. The company manages 153,000 business touchpoints across 97% of India’s districts, supported by 4,500+ cash vans and 240+ branches.

As of Jun 2025, CMS managed 153,000 business touchpoints, up 9% year-over-year from 137,000. The network kept expanding despite industry debates about cash’s relevance these days.

The company runs 240+ branches nationwide as regional hubs for cash processing and fleet maintenance. Local presence enables faster incident response for bank clients. In cash logistics, proximity builds reliability. Reliability wins contracts.

CMS vans travel approximately 4 lakh kilometers every single day across India (all vans combined). That equals circling Earth ten times daily. Operational intensity at this scale is extraordinary. Difficult to replicate too.

The fleet comprised 4,500+ cash vans in FY24, equipped with GPS tracking and security systems. Building this fleet requires significant capital and time.

CMS connects over 12,000 bank branches for cash-in-transit services. These connections form the backbone of bulk currency movement in Indian banking. Removing CMS from this network would be deeply disruptive for clients.

The company handles ₹14 lakh crore in currency annually, a meaningful share of India’s total currency in circulation.

CMS employs over 25,000 people and third-party personnel trained in specialized logistics and security protocols.

The company holds 42% of India’s organized cash logistics market. Every new touchpoint added to the network increases route density, lowering cost per stop across the board. Interesting economics.

3. Route Density Economics

CMS generates margins above 25% in its cash management business, well above the industry average. This profitability is a direct output of route density. More stops per kilometer means lower cost per pickup. CMS, with the largest network, achieves the highest density in the country. Dense routes are profitable routes.

CMS vans travel in dense clusters, minimizing road time between pickups. Their Fuel costs grew only 3.6% in FY24 despite significantly higher activity levels. Density absorbs inflation that would hurt smaller, thinner operators.

Proprietary route planning technology ensures 4,500+ vans take optimal daily paths. This is algorithm-driven logistics dispatch, not manual scheduling.

One van can service multiple bank clients in a single trip due to high stop density. Fixed travel costs are shared across more stops. Cost per pickup falls as volume rises.

Adding retail pickup points adjacent to existing ATM routes generates incremental revenue at near-zero marginal cost. Standard logistics routes become high-margin service lanes.

The company maintained a 15%+ PAT margin in Q3 FY26 despite wage hikes and inflationary pressures. Route efficiency absorbed cost increases that would have squeezed smaller and less dense operators significantly.

4. Annuity Contract Stability

Around 80% of Cash Logistics revenue is secured through 3 to 5-year contracts. The largest deals now span 10 years. This structure gives CMS a predictable revenue floor regardless of quarterly business conditions.

In January 2026, SBI awarded CMS a ₹1,000 crore integrated cash solutions contract for 5,000 ATMs. The deal spans 10 years. Decade-long revenue visibility from a single client.

HDFC Bank awarded a ₹400 crore ATM managed services contract in May 2026 covering 6,000 ATMs for five years. This adds approximately ₹80 crore in steady annual revenue. Large private banks are outsourcing infrastructure aggressively.

New order wins in FY24 reached a record ₹1,850 crore, nearly double the prior year’s total. These are multi-year contracts that ramp and compound over their execution periods.

The Managed Services order book stood at approximately ₹1,400 crore as of December 2025. This provides revenue visibility extending four to seven years forward.

ATM managed services contracts bundle currency forecasting, site maintenance, and software together. This comprehensive scope makes switching providers costly and operationally disruptive.

ICICI Bank awarded CMS the ALGO MVS software mandate in FY26, a multi-year software-linked deal. Software contracts are stickier than logistics contracts.

CMS has maintained a high renewal rate with top banking clients over the last decade.

5. Managed Services Pivot

CMS moved from #5 to #3 in India’s ATM managed services market between FY21 and FY25. The Managed Services segment contributed 40% of total revenue by July 2025. This pivot from pure logistics toward a technology-led services model has expanded the company’s value proposition, addressable market, and margin profile simultaneously.

CMS jumped from #5 to #3 in managed services by displacing technology-focused firms, not just logistics players. The integrated logistics-plus-technology model is a product pure-play tech firms cannot easily replicate.

The company manages 39,000 ATMs through its Managed Services portfolio as of March 2026. In addition, 68,000 machines are covered through standard cash logistics. Together, that is more than one in three ATMs across India.

The ATM-as-a-Service model makes CMS a single point of accountability for the entire ATM operation. Security, software, cash, and maintenance are bundled into one vendor relationship. Banks prefer one vendor over five.

Technology-led services within Managed Services are growing faster than traditional cash handling. This signals higher lifetime client value and structurally better margin profiles.

The FSS ATM managed services business was acquired in March 2026 for ₹115 crore, adding 8,000 ATMs and new banking relationships.

6. AIoT Technology Moat

CMS built a proprietary AI and IoT surveillance platform. The HAWKAI Vision AI system monitors thousands of ATM and branch sites in real time. It has prevented over 2,700 potential incidents to date. This technology creates a distinct revenue stream and makes the overall platform significantly harder to displace.

HAWKAI prevented over 900 burglaries through proactive monitoring in FY25 alone. This translates into measurable savings on insurance and incident losses for bank clients.

AIoT Remote Monitoring generated ₹100 crore in annual revenue in FY24. Management expects its share to grow from 5% to 8% of total revenue within three years. A high-margin revenue stream with a clear growth trajectory forming.

CMS acquired Securens Systems in FY26 for approximately ₹80 crore, gaining 100% stake in a focused AIoT leader. The combined entity is double the size of its closest competitor in this space.

CMS operates centralized command centers monitoring 25,000+ live sites using AI to prioritize alerts. Human staff handle escalations. AI handles volume. This combination is both scalable and cost-efficient.

The company is executing an AI-enabled surveillance project for a leading bank covering all its branches. This moves CMS beyond ATM monitoring into total branch security.

The ALGO OTC solution prevented 19,000 errors in the cash cycle for one major bank. CMS becomes the accuracy and auditability layer embedded inside banking operations.

7. Retail Ecosystem Expansion

CMS is building a second growth axis in India’s organized retail sector through its Retail 360 platform. The company services 65,000+ retail points today, including fuel stations, apparel chains, airlines, quick commerce firms, and NBFCs. India’s consumption-driven expansion is actively driving this segment.

A leading quick commerce chain uses Retail 360 across 1,500 locations to digitize daily cash. Automated cash handling removes a manual bottleneck in fast-paced operations.

CMS provides API-integrated cash reconciliation across 1,000 stores for a major eyewear retailer. Real-time data updates eliminate manual discrepancies at the store level.

CMS provides 24x7 cash collection for a large airline at 40 airport sites. The airline receives early credit for collected cash, improving daily liquidity positions. A niche use case with reliable and recurring demand.

Less than one-third of India’s 550,000+ organized retail touchpoints currently outsource cash management. The untapped opportunity is substantial. CMS is early in penetrating a market growing alongside India’s consumption story.

Retail cash management revenue grew 11.2% YoY to ₹1,474 crore in FY24.

8. Disciplined M&A Playbook

CMS has completed eight acquisitions over the last decade, all funded from internal cash accruals. Each deal targets a specific gap: a technology capability, a new customer base, or a competitor’s market position. The acquisition machine is systematic, self-funded, and executed without debt.

Hemabh Technology was acquired in March 2022 to enter AI-based remote monitoring and video analytics. This early move positioned CMS as a technology company before the industry broadly recognized the category.

The Securens Systems deal in FY26 was valued at approximately 10x FY25 EBITDA. Post-synergy estimates drop the effective multiple to approximately 4x. A highly accretive acquisition if execution goes to plan.

FSS’s ATM managed services business was acquired in March 2026 for up to ₹115 crore. It added 8,000 ATMs and new banking client relationships.

The Securus acquisition in Q3 FY26 for ₹70 crore further strengthened the technology portfolio. Three acquisitions completed in FY26.

Cumulative external equity raised across the company’s entire history is less than ₹200 crore.

The company’s market share in cash logistics reached 42% by FY25 through organic growth and acquisitions combined.

9. Capital Allocation Discipline

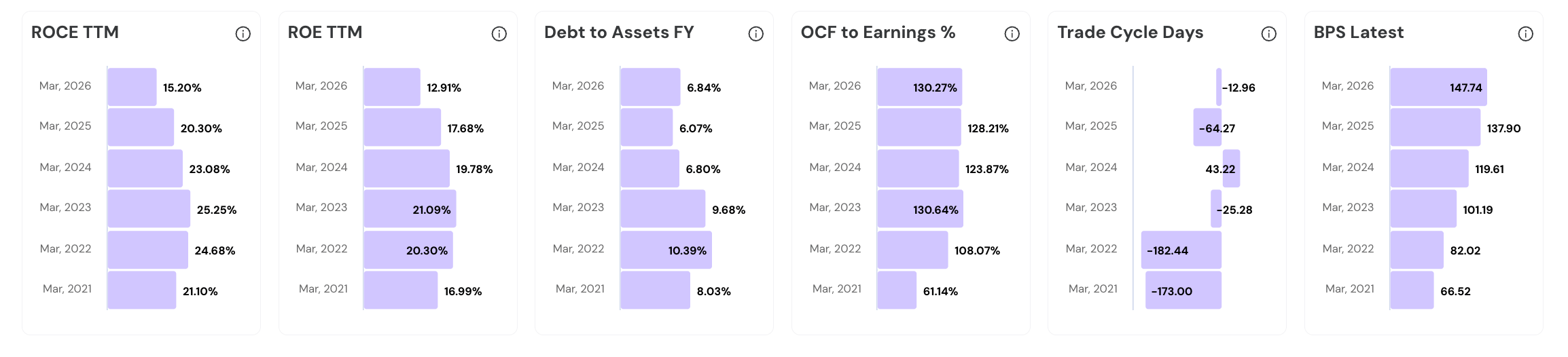

CMS generates strong operating cash and deploys it with visible discipline across dividends, capex, and acquisitions. The company is debt-free, pays regular dividends, funds all capex internally, and still holds ₹1,000+ crore available for future moves. Operating cash flow reached ₹439.89 crore in FY25.

CMS has paid dividends for six consecutive years. The payout ratio reached 42% of PAT in FY25.

Operating cash flow to EBITDA conversion was 75% in FY24. Most earnings become actual cash.

CMS plans capex of over ₹400 crore in FY26, entirely from internal cash flows.

In Q3 FY26, management pruned unprofitable retail network points rather than protect revenue optics.

Revenue growth guidance of 15% to 19% for FY25 was paired with explicit emphasis on high-quality service revenue.

10. Risks and Red Flags

CMS moves ₹14 lakh crore annually across 97% of India’s districts. At this scale, risks are real, specific, and worth tracking carefully.

CMS reported 28 embezzlement cases in FY25, with losses of ₹21.72 crore, nearly double the ₹12.05 crore loss from FY24. Only ₹3.20 crore was recovered. The ₹21.72 crore embezzlement loss represents less than 0.01% of the ₹14 lakh crore handled annually. Proportionally small, but the rising trend is the actual concern. Embezzlement is a financial crime where a person entrusted with money or assets legally steals them for personal use.

Contingent liabilities stood at ₹604 crore as of the latest reported period, significantly exceeding FY25 net profit of ₹373 crore. Tax disputes form the bulk of this exposure. Any adverse court ruling could cause sudden material cash outflow.

Subsidiary Securitrans India received a ₹19.34 crore service tax demand plus penalties in April 2024. Authorities alleged suppression of facts to evade payment.

India’s total ATM count is declining. If this contraction continues, the core Cash Logistics segment faces a structural volume headwind.

UPI transactions have crossed 14 billion per month. ATM transaction growth is slowing. The long-term direction of physical cash usage is genuinely uncertain.

In Q1 FY26, payment delays from certain Managed Service Providers caused a temporary spike in receivables. CMS is exposed to the financial health of its partner chain, not only its direct banking clients.

Hitachi Payment Services recently acquired a competitor and now offers a full-service suite directly competing with CMS in managed services. A well-capitalized rival with a broad platform is a more serious threat.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

These TTM numbers perfectly illustrate the hidden operating leverage at play here. The market gets distracted by the macro digital payments narrative, but the consistent PAT and FCF growth show a business efficiently scaling its high-margin managed services. I just published a deep dive on this exact financial transition—great to see the raw data validating the thesis!

Sir why there is no promoters holding in this stock. Is it negative or positive for this stock?