Campus Activewear || Consistently Performing Stocks #60

What has led to the consistency?

Every week I analyze a company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.This week, Let’s explore the business & fundamentals of Campus Activewear Ltd.

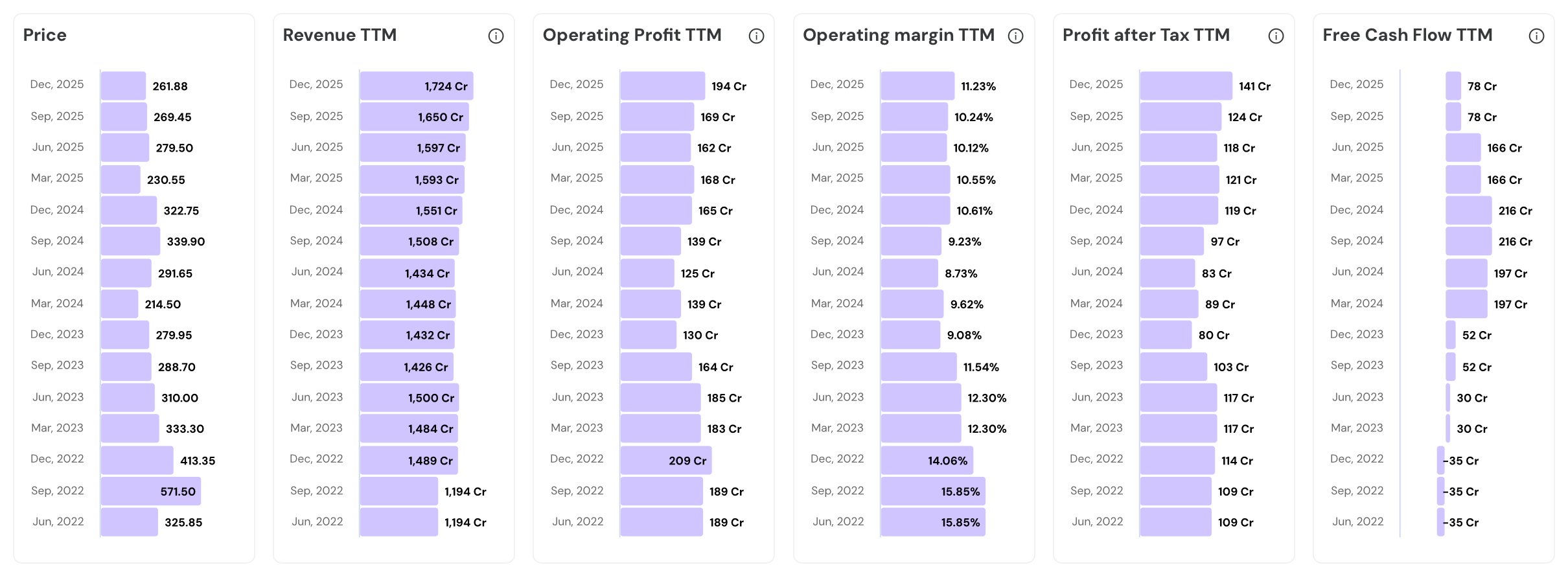

In the last 3 years…

- Revenue TTM has grown 1.44x (from ₹1,194 Cr to ₹1,724 Cr)

- Operating Profit TTM has grown 1.03x (from ₹189 Cr to ₹194 Cr)

- PAT TTM has grown 1.29x (from ₹109 Cr to ₹141 Cr)

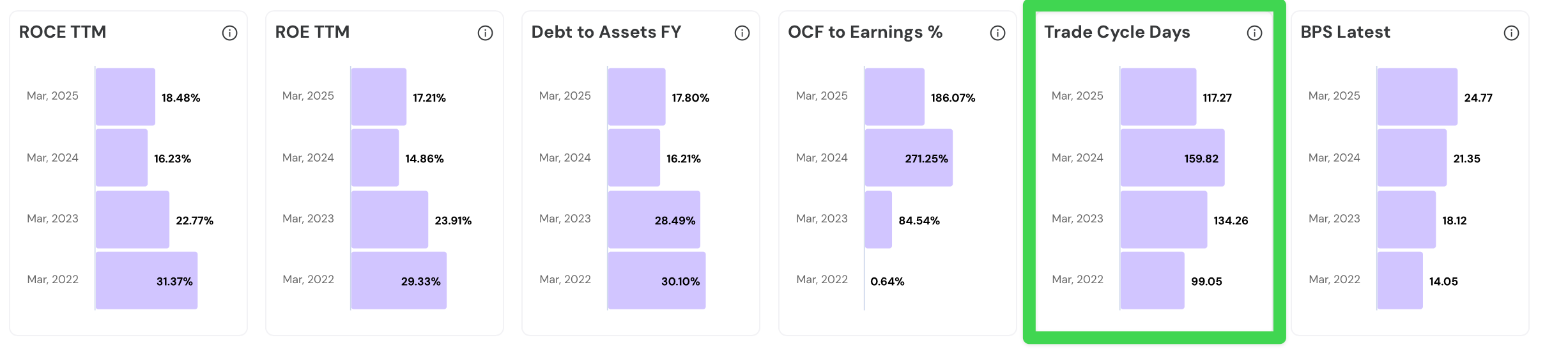

Take a look at the fundamentals chart below.Performance Chart

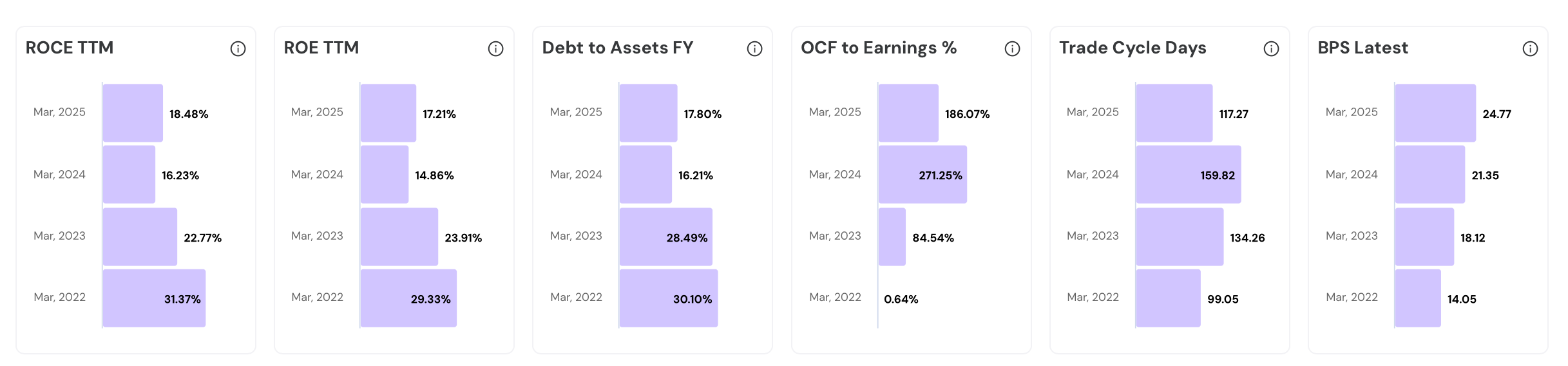

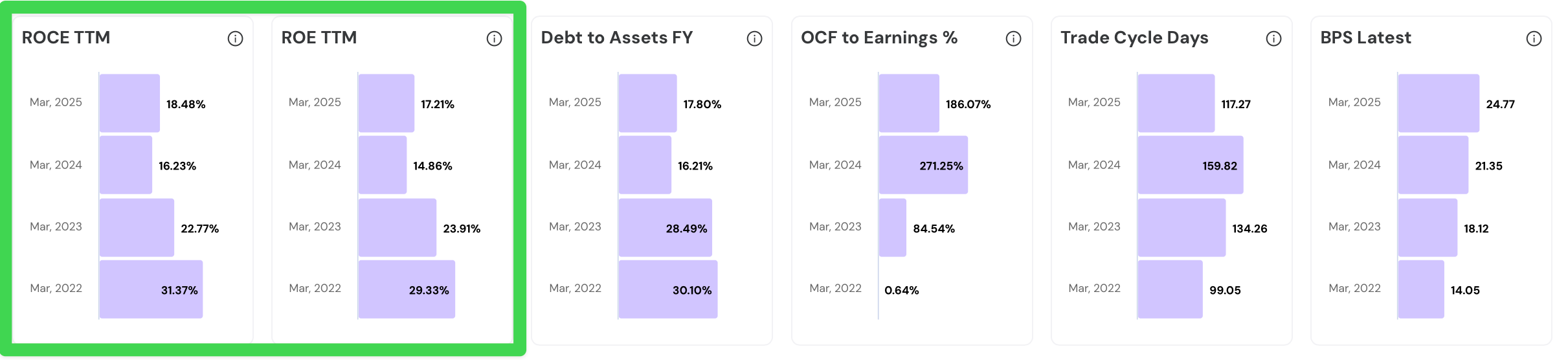

Quality Chart

Their Road to Consistency

1. Overview and Business Model

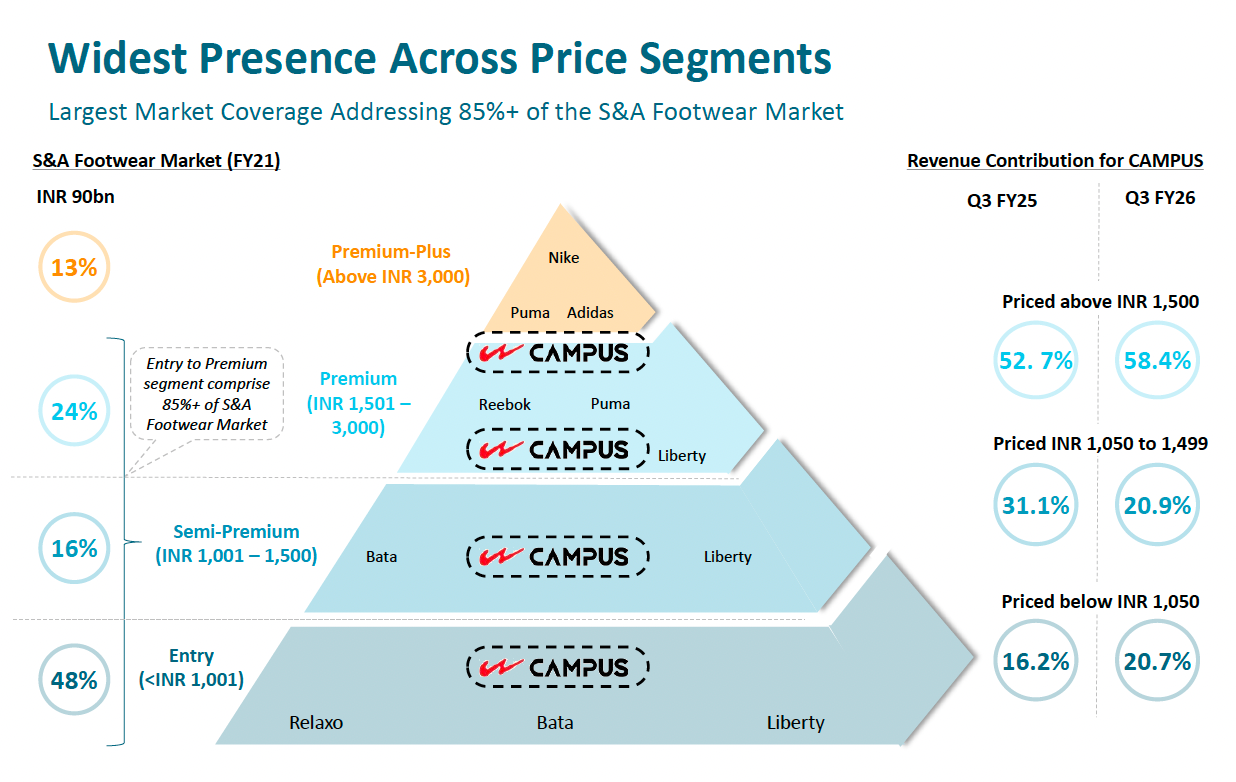

Campus Activewear is India’s largest sports and athleisure footwear brand by value and volume. The company sells running shoes, walking shoes, and casual sneakers for the entire family.

Campus holds 17% of India’s branded sports and athleisure footwear market. It competes directly against Nike and Puma at a fraction of the price.

Revenue grew from ₹1,448 Cr in FY24 to ₹1,593 Cr in FY25. Latest TTM Revenue is about ₹1724 Cr. Volume rose from 22.2 million to 25 million pairs in the same period. Volume and value growing together is a positive.

Men’s footwear dominated with 81.3% of revenue in Q3 FY25. Women and children together now represent 18.7% of the business.

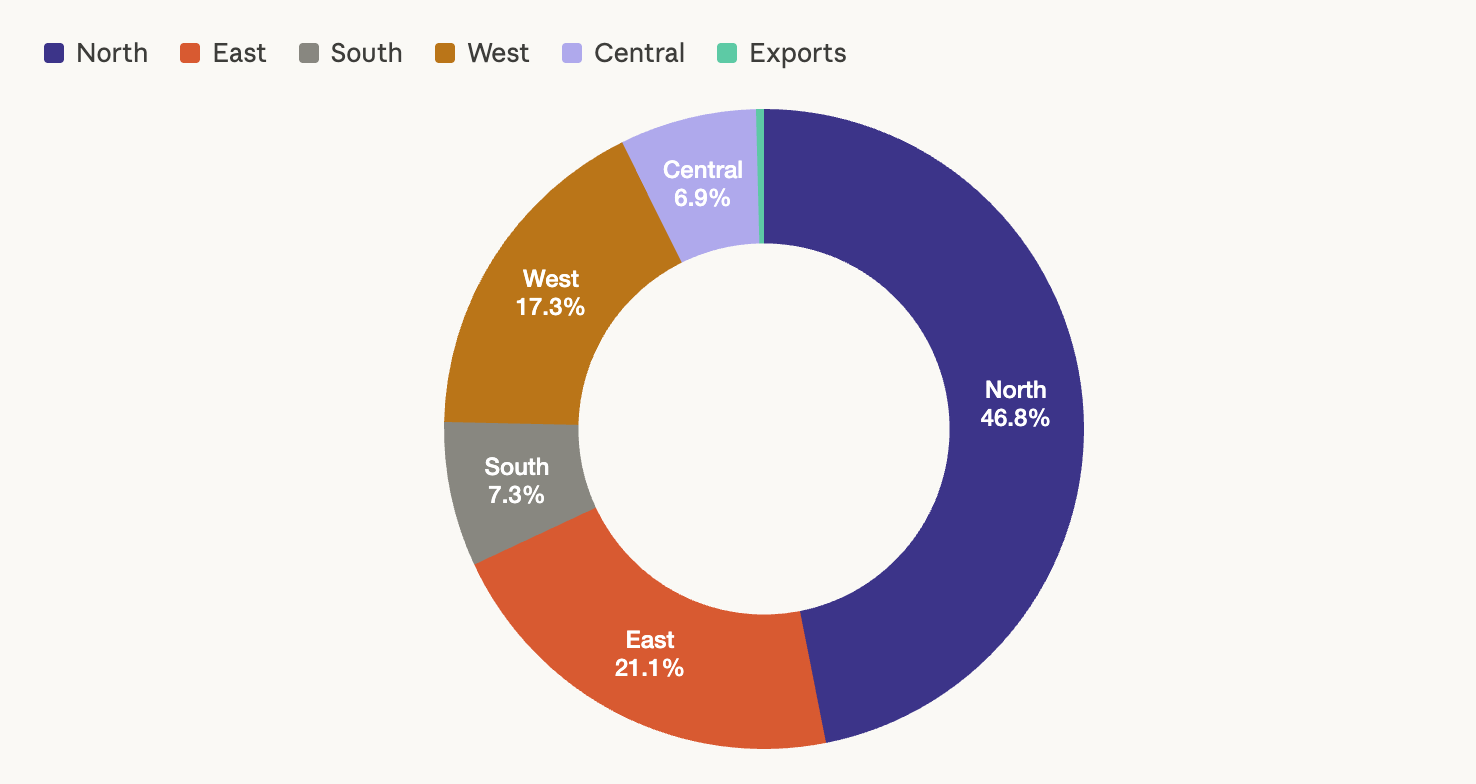

North India accounts for ~47% of total revenue.

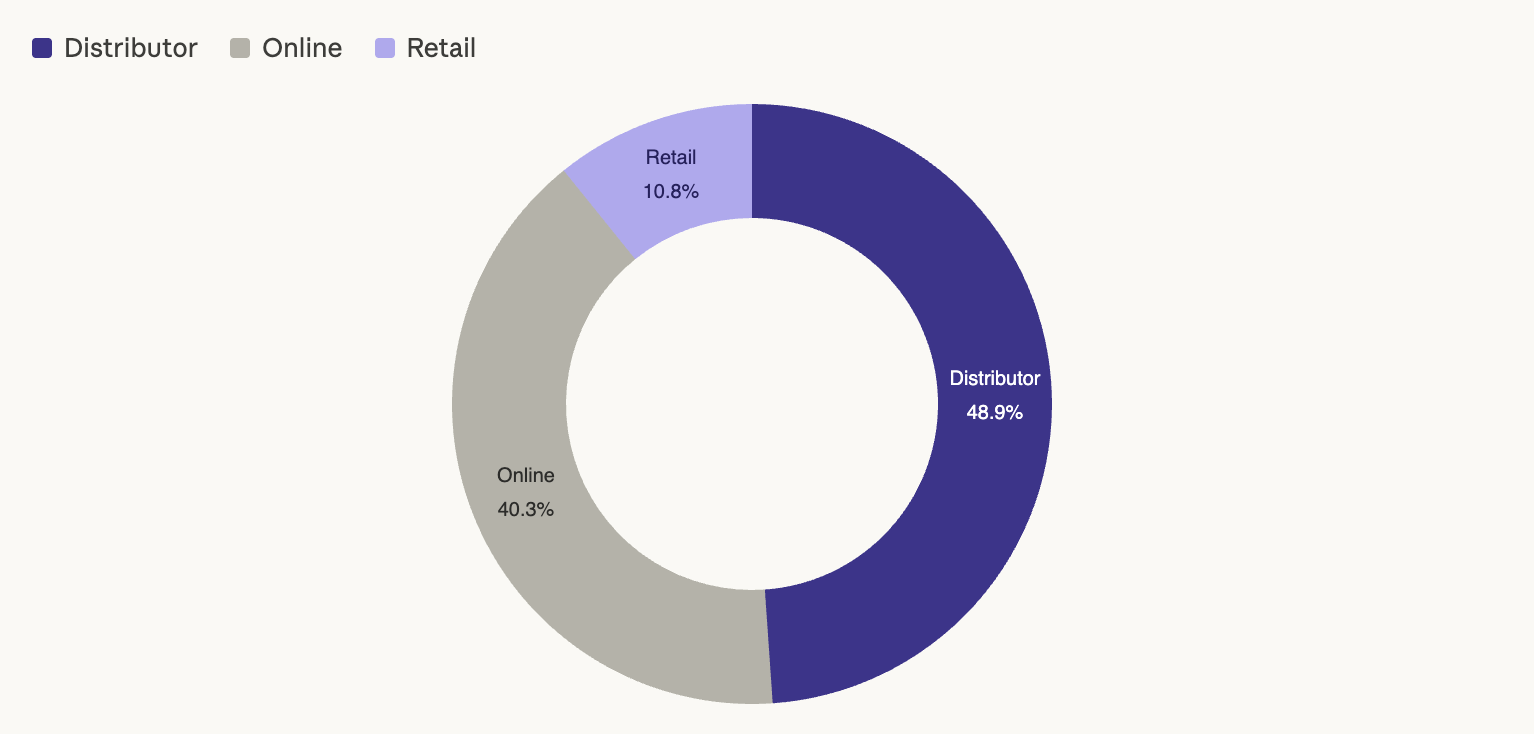

Trade distribution contributes ~50% of sales. D2C & Online platforms account for ~50%. A balanced channel mix.

The brand reaches 29,000+ retailers across 700+ cities in 28 states. It also runs 290+ Exclusive Brand Outlets nationally. Distribution density of this scale is impressive.

Campus was built on one idea. Global designs at Indian price points.

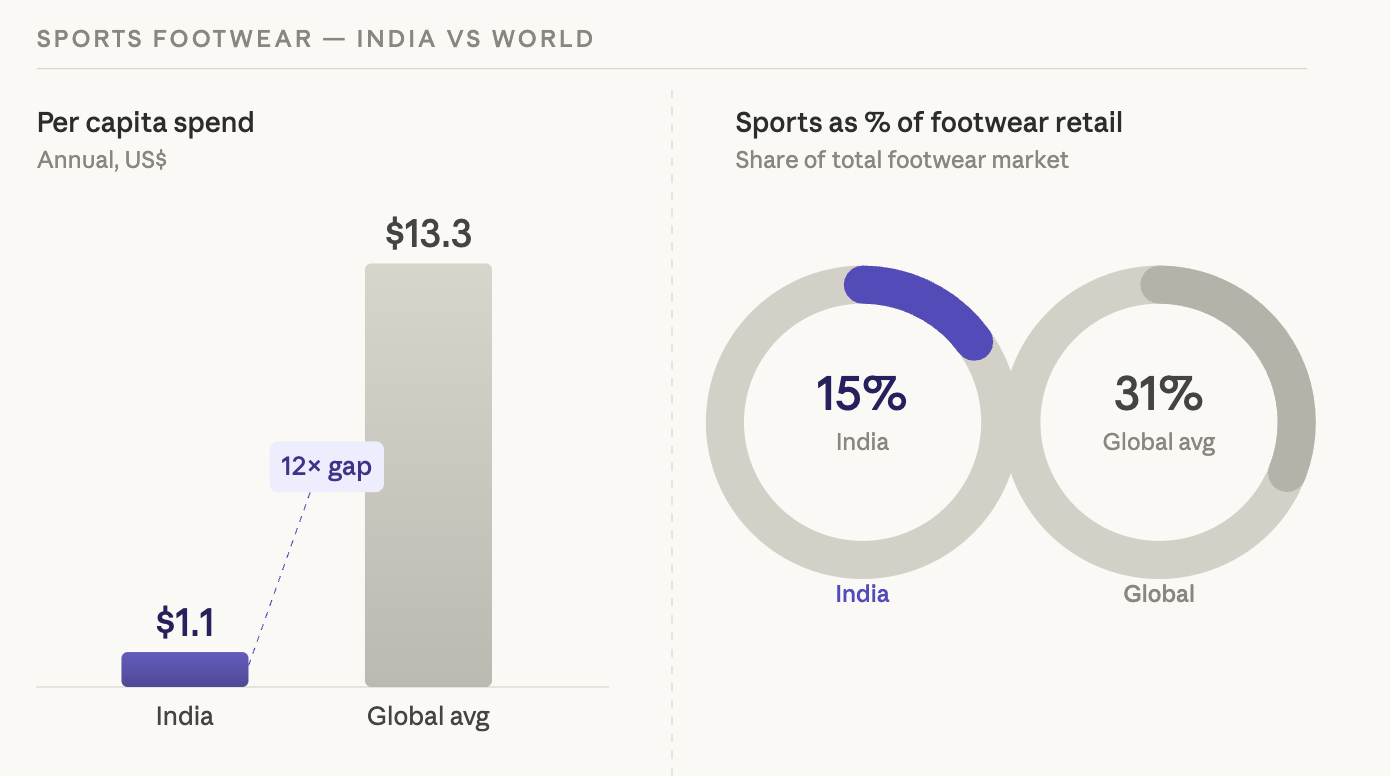

India's per capita Sports footwear spend is just US $1.1, against a global average of US $13.3. The Sports footwear segment is only 15% of Indian footwear retail, versus a global average of 31%. These numbers indicate a long-term structural opportunity.

2. Vertically Integrated Manufacturing

Campus operates a fully vertically integrated manufacturing system covering soles, uppers, and final assembly. This control over every production step allows the company to maintain quality, protect margins, and launch new designs faster.

5 manufacturing facilities operate across India. Total assembly capacity stands at ~30.7 million pairs.

100% of footwear is assembled in-house, ensuring every pair meets the company’s quality benchmarks.

The Gannaur facility was recently expanded to increase production of specialized soles.

A Haridwar II upper plant dedicated specifically to sneaker production has been commissioned in FY26. This is a direct response to the 116% sneaker category surge.

An upper manufacturing facility at Paonta is now operational, adding a third upper plant alongside Haridwar I and Haridwar II.

Land and building were acquired at Pant Nagar in FY26, signalling the next phase of capacity expansion.

Over 90% of raw materials are sourced domestically. This shields the business from global shipping disruptions and trade volatility.

Vertical integration enabled launch of ~270 new designs in FY25 alone. That speed of design-to-shelf is nearly impossible without in-house manufacturing. Fast fashion logic successfully applied to branded footwear.

Their proprietary technologies like Nitrofly and Air Capsule use specialized molds and tooling during production. Design registrations legally protect these innovations from being copied.

In Sep 2025, the company invested ₹74.75 crore to acquire land and buildings in Uttarakhand. This signals long-term commitment to expanding production capacity.

Increasing captive production of uppers is expected to reduce the cost of semi-finished goods.

Regional warehouses store components and finished goods close to markets. This shortens replenishment cycles for 300+ distributors nationally.

Manufacturing lead times are 80 to 100 days, against an industry average of 90 to 120 days. This speed advantage is a direct output of vertical integration.

3. Multi-channel Distribution

Campus reaches consumers through trade distribution, e-commerce marketplaces, exclusive brand outlets, and large format stores. With over 29,000 retailer touchpoints and 280+ distributors, this network took years to build.

Trade distribution generated ₹832.9 crore in FY25. Over 280 distributors provide the brand with premium shelf space nationwide. Traditional trade still remains the backbone of the business (~50%)

D2C channels (Online + Exclusive Business Outlets + Large Format Stores) crossed 50.6% of revenue in Q3 FY26, surpassing trade distribution for the first time.

Campus partnered with Zepto in late 2024 to enter quick commerce. Customers can now receive footwear within minutes of ordering.

The company transitioned its online business to a marketplace model for better inventory and pricing control. This shift from the older B2B approach improved sales quality and profitability.

290+ Exclusive Brand Outlets operate across India. These stores showcase the full product range and deliver a premium in-store experience.

During FY24, the company added 66 new stores targeting the Western and Southern regions. This directly reduces reliance on the North Indian market.

Products are available at over 2,200 Large Format Store counters inside high-footfall malls and departmental stores.

A Distributor Management System tracks secondary sales and monitors inventory health at every touchpoint daily.

An internal sales force of 220+ employees directly covers approximately 15,000 retailers.

High-spending urban consumers in premium malls are the next growth segment.

The company is now penetrating rural markets through a super stockist model, extending reach beyond 700 districts into areas where standard distributor economics do not work.

4. Fast Design Refreshes

Campus launches around 300 new shoe designs every year through a dedicated 30-member team working with global design consultancies. This constant product refresh keeps the brand exciting for young Indian consumers.

A 30-member design team collaborates with global consultancies to produce roughly 300 new designs every year. This output frequency is unusually high for a domestic footwear brand. A fresh footwear catalog keeps consumers returning.

The full product development cycle from conceptualization to launch is typically 120 to 180 days.

The sneaker category grew 116% in Q3 FY25 as the brand captured a major shift toward casual fashion. Sneakers in India have moved from sportswear into everyday wardrobe staple.

The Air Capsule Pro collection launched in early 2025 with upgraded impact cushioning technology. It targets consumers who move between work and workouts without changing shoes.

Nitrofly and Nitro Boost technologies deliver energy return and lightweight performance at accessible price points. Performance-grade technology was previously exclusive to ₹10,000+ international shoes. Campus has to an extent democratized it for consumers spending under ₹2,000.

The company maintains over 2,500 active shoe styles covering every price segment from economy to premium. No consumer price point goes unaddressed.

600+ active styles were running simultaneously in Q3 FY26, each selling 1,800+ pairs per style on average. This is a useful proxy for demand per style.

A “never out of stock” replenishment system keeps core evergreen models continuously available.

The premium segment grew to 57.2% of total sales in Q2 FY26.

Shoes with shock absorption and reflect technology are available at prices as low as ₹699. Performance features at these price points are unmatched globally.

Accessories like socks are being introduced to improve the product mix and grow average transaction values.

Campus is building a complete athleisure ecosystem.

5. Celebrity Brand Building

Campus invests heavily in Bollywood celebrity endorsements and 360-degree multimedia campaigns to build an aspirational identity at accessible price points.

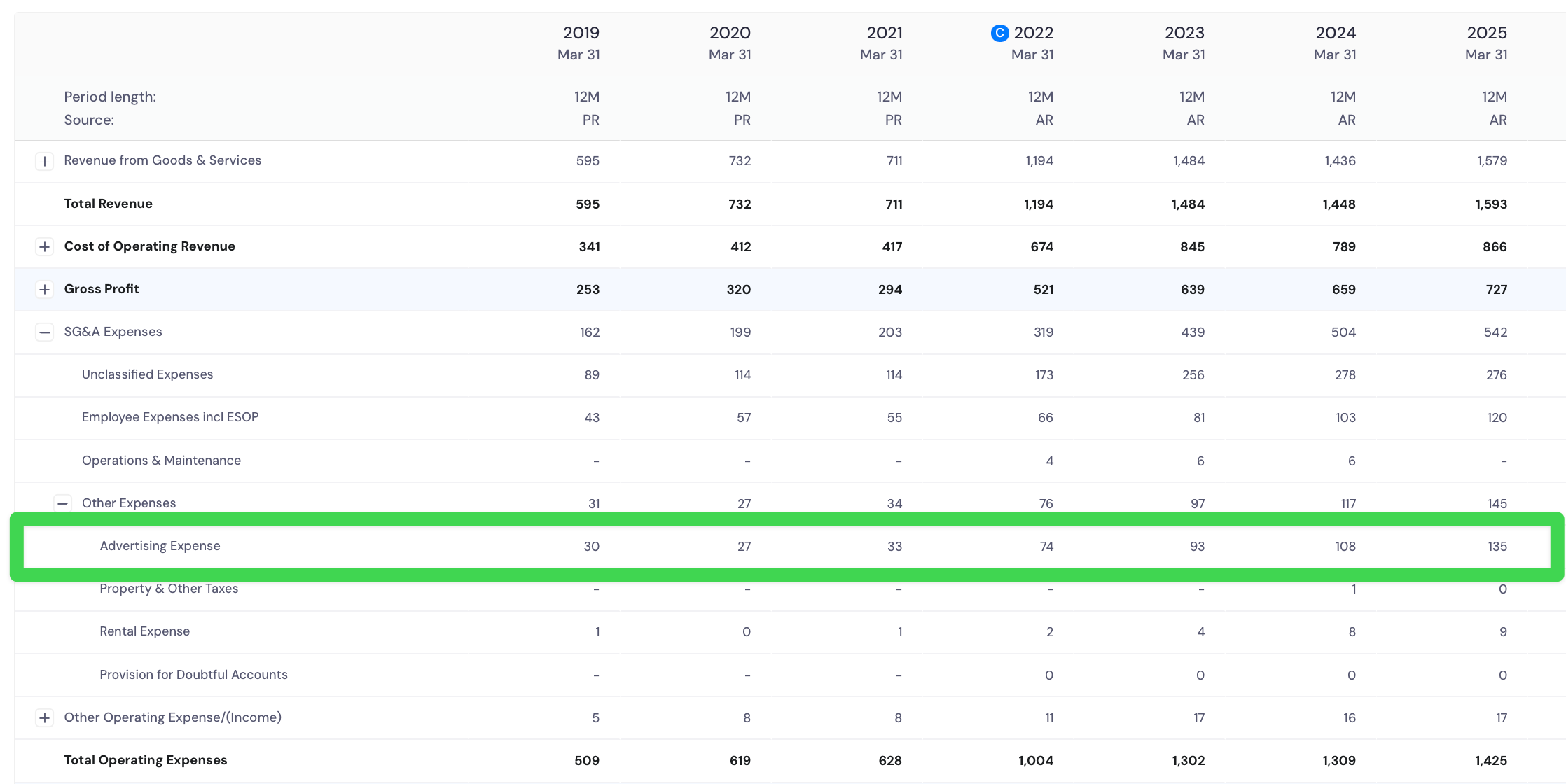

Advertising and promotion spend grew to ₹135 crore in 2025 from ₹108 crore the prior year. This sustained investment keeps the brand continuously visible across television and digital platforms. Brand spend in this particular case is not an expense. It is more of a long-term asset.

Vicky Kaushal was appointed brand ambassador for the “Move Your Way” campaign in late 2024.

Kriti Sanon fronted the “You Go, Girl!” campaign in early 2025 to target women’s footwear specifically.

Siddhant Chaturvedi voiced the campaign anthem “Aye Bro, Capsule Pro” for the Air Capsule Pro launch.

The 360-degree strategy spans television, print, digital, influencer, and outdoor formats simultaneously. Comprehensive coverage builds brand recall across every consumer touchpoint.

A multimedia strategy in FY25 ran across digital media, news channels, and outdoor advertising at the same time. Reaching consumers through multiple formats reinforces brand memory.

Marketing is increasingly data-driven with a focus on Tier 2 and Tier 3 city consumer preferences.

Social commerce is used to micro-launch products and test consumer demand before full-scale rollout. This reduces the risk and cost of failed product launches significantly.

Celebrity endorsements have successfully shifted the brand’s perception from budget to fashionable lifestyle. Campus can now sell premium shoes priced above ₹3,500 with genuine consumer desire. Brand image improvements directly unlock higher price points.

6. Digital Systems Scale

Campus has invested heavily in enterprise software, data analytics, and automation across its supply chain, manufacturing floor, and retail operations. These technology investments are improving forecast accuracy, reducing inventory waste, and accelerating time-to-market.

Campus completed the SAP S/4HANA implementation in April 2025. This provides real-time data visibility across all business processes for the management team.

The company invested ₹150 crore in technology in 2024 to upgrade supply chain and e-commerce infrastructure. Operational efficiency is expected to improve by 15% with reduced delivery lead times.

A Distributor Management System connects 300+ distributors and monitors secondary sales daily. It prevents inventory buildup and ensures smooth product flow toward retailers.

Advanced data analytics forecast demand for specific shoe styles and colors across different Indian regions. Efficient stock allocation reduces instances of popular items going out of stock. The right product, in the right place, at the right time.

3D designing and virtual sampling processes are now used on the manufacturing floor. A new shoe model can now be developed in days rather than weeks. Speed to market has never been faster.

An integrated Warehouse Management System optimizes storage and movement of over 24 million pairs annually. On-time delivery rates improved by 10% to 20% over the past year.

Omnichannel technology syncs inventory across the website and physical stores simultaneously. Customers can buy online and collect from a nearby store. Unified inventory management is the backbone of modern consumer retail.

Data links between the company and 26,000+ retailers enable demand-driven stock allocation. Each store receives the specific styles most popular in its local market.

AI-based product recommendations on e-commerce platforms have improved online conversion rates. Showing the right shoe to the right consumer at the right moment maximizes digital revenue.

Technology improvements have also streamlined reverse logistics for online returns, which can run as high as 25%. Faster return processing puts inventory back into available stock more quickly.

7. Geographic Expansion

Campus is systematically reducing its North India dependence by expanding into the West, East, and South through new stores, stronger distributor networks, and digital-first market entry.

North India contributed 39.7% of revenue in FY25, but the concentration is gradually declining. Reducing geographic dependence is a deliberate and ongoing management priority.

The Western region now contributes 23.8% of total revenue. Aggressive store openings in Maharashtra and Gujarat are driving this growth.

Eastern India accounts for 20.6% of revenue in FY25. Campus’s affordable pricing resonates strongly with price-sensitive consumers in this region.

Southern India is currently 7.7% of sales but the fastest-growing region. The brand uses online platforms to test the Southern market before committing to physical stores.

In FY24, the company added 66 new Exclusive Brand Outlets primarily in the Western and Southern regions. This builds recognition in territories where global brands were previously dominant.

Campus products are now available across 650+ cities in 28 states. This is among the widest geographic footprints of any Indian footwear brand.

Management consolidated its distributor base to 350 high-performing partners. Focusing resources on the best distributors improves volume per partner.

8. Financial Discipline

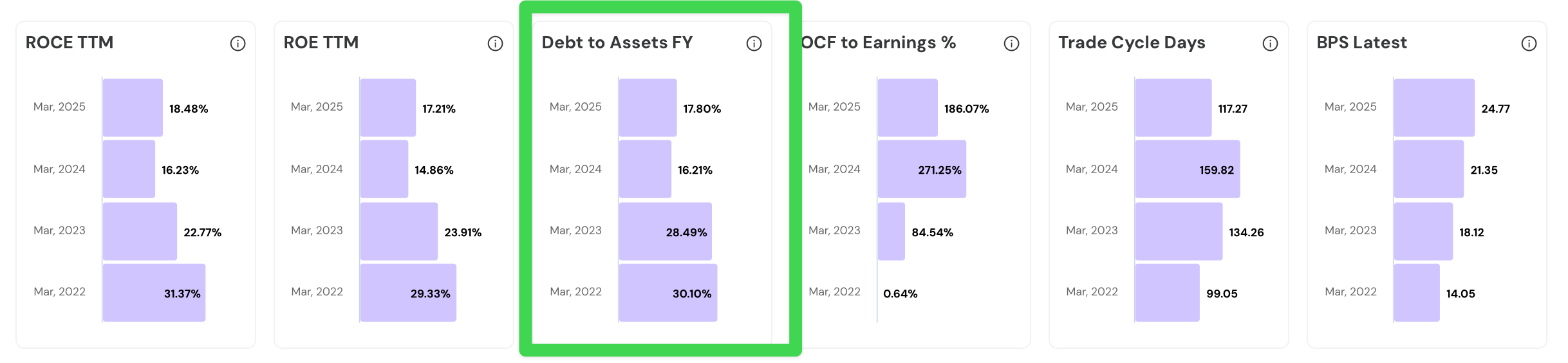

Campus has transformed its balance sheet over the last three years through debt repayment, faster receivables collection, and better inventory management.

The company has been reducing the debt as a percentage of total assets over the years.

Trade Cycle days dropped from 159 days in FY24 to 117 days by end of FY25. This shows vastly improved cash cycle efficiency across the business.

Although ROCE and ROE has dipped over the years, they are showing signs of improvement since 2025.

9. BIS Compliance Advantage

The Bureau of Indian Standards certification regime for footwear has become a powerful structural tailwind for Campus. As the first footwear company in India to receive BIS certification, Campus enjoys quality credibility while smaller and unorganized rivals struggle with costly compliance.

Campus was the first footwear company in India to receive a BIS certificate.

This gave the brand a substantial head start over all peers navigating the compliance process.

The company is 100% BIS compliant across its entire product portfolio. This acts as a structural entry barrier against low-quality footwear imports from China and Vietnam.

BIS norms are expected to significantly curb cheap non-compliant footwear imports. Removing this unfair price competition directly benefits organized domestic brands.

Non-BIS compliant inventory was reduced to less than 10% of total stock by early 2025. Proactive liquidation of old stock cleaned the supply chain ahead of the regulatory deadline.

The liquidation process impacted gross margins by 20 to 40 basis points over recent quarters. This was a deliberate and calculated short-term trade-off.

Footwear companies with under ₹50 crore in turnover are struggling to afford BIS compliance costs. This is directly channeling market share toward larger organized players.

The government set a Jun 2025 deadline to remove all non-compliant footwear from the Indian market.

Campus uses in-house testing facilities to verify every batch of raw materials and finished goods against BIS criteria.

BIS transition is accelerating consumer migration from unorganized to organized footwear brands. Campus is perfectly positioned to absorb these newly converted consumers.

BIS compliance also strengthens the brand’s credibility for its export business. Meeting strict domestic quality norms builds a foundation for global market entry.

10. Risks and Red Flags

Abros, a brand founded by a former Campus COO, poses a genuine competitive threat. This rival knows the company’s internal distribution strategies and product playbook intimately. Insider competition is one of the most dangerous forms of rivalry.

After achieving net-debt-free status in FY24, the company’s net debt returned to ₹128.7 crore in TTM 9MFY26. While capex-driven and manageable, this reversal deserves monitoring especially if revenue growth slows.

North India’s share spiked back to 46.8% in Q3 FY26, suggesting geographic concentration risk is seasonal and structural, not yet fully diversified.

During economic slowdowns, global brands like Nike and Puma tend to discount heavily. Their products then enter the same price range as Campus shoes. Premium global brands going price-aggressive can directly hurt Campus’s positioning.

Raw material price volatility in EVA and PU compounds is a persistent cost risk. Many inputs are imported or tied to international commodity cycles. Margin compression from raw material spikes happen faster than pricing adjustments.

The shift to a marketplace model online increases inventory risk on Campus’s own balance sheet. Under the older B2B model, e-commerce platforms absorbed that inventory risk entirely. Campus now carries more exposure on its books.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.