APL Apollo Tubes || Consistently Performing Stocks #56

What has led to the consistency?

Each week I analyze one company's fundamentals as part of my research work. My goal is to understand what drives their consistent performance. This is an educational post to understand the business and not a recommendation to buy the stock.This week, Let’s explore the business & fundamentals of APL Apollo Tubes Ltd.

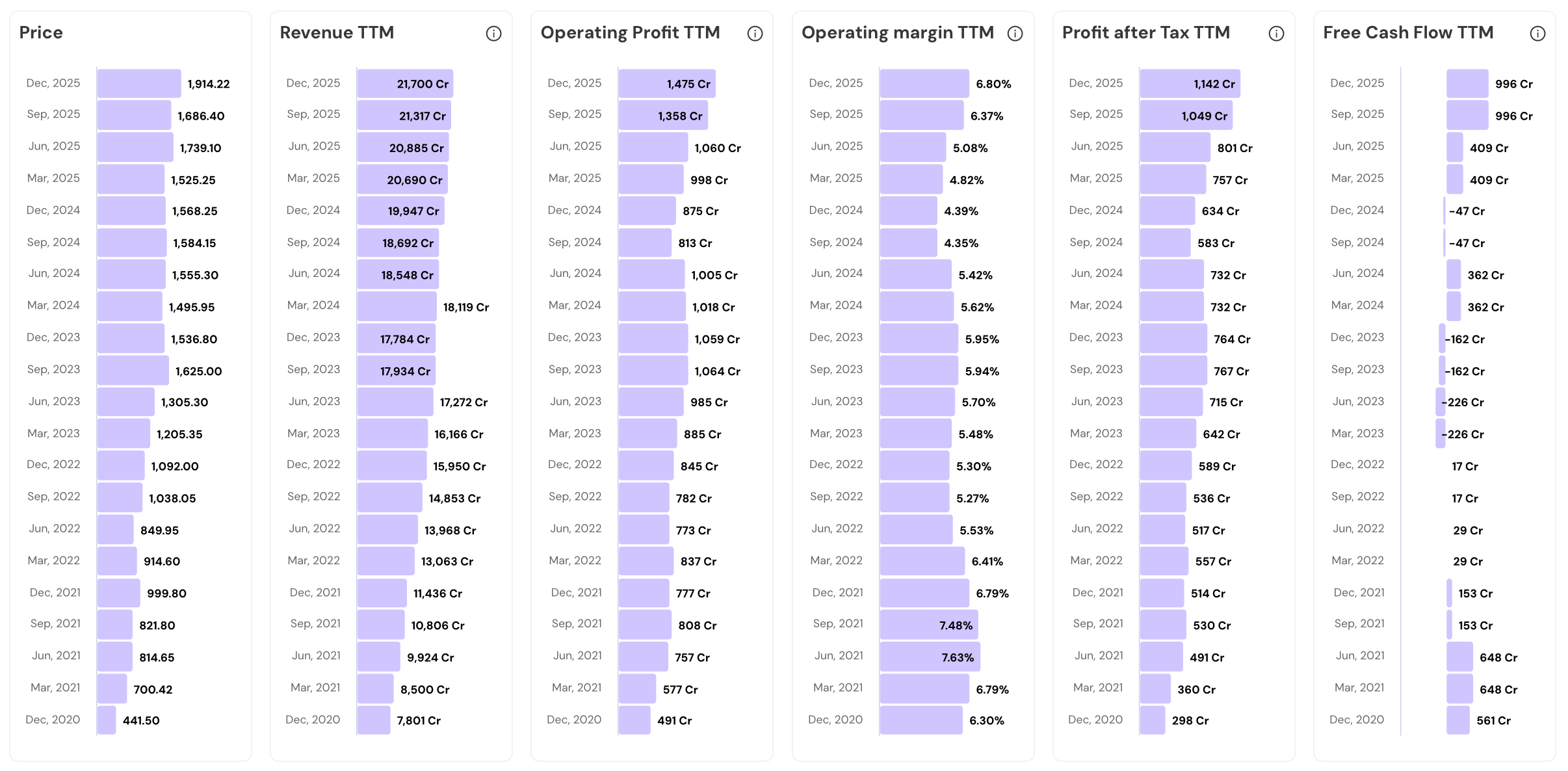

In the last 5 years…

- Stock price has grown 4.3 times (from 441.50 to 1,914.22)

- Revenue has grown 2.8 times (from 7,801 Cr to 21,700 Cr)

- Operating profit has surged 3.0 times (from 491 Cr to 1,475 Cr)

- PAT (Profit after Tax) has surged 3.8 times (from 298 Cr to 1,142 Cr)

Take a look at the fundamentals chart below.

Their Road to Consistency

1. Overview & Business Model

APL Apollo Tubes is India’s largest structural steel tube manufacturer, commanding a 55% domestic market share.

The company purchases hot-rolled coils from JSW Steel, Tata Steel, and SAIL, converts them into specialized structural shapes, and sells through 800+ distributors.

The business earns money on conversion, not steel prices. APL Apollo charges a premium for transforming flat coil into engineered shapes. This is the conversion margin.

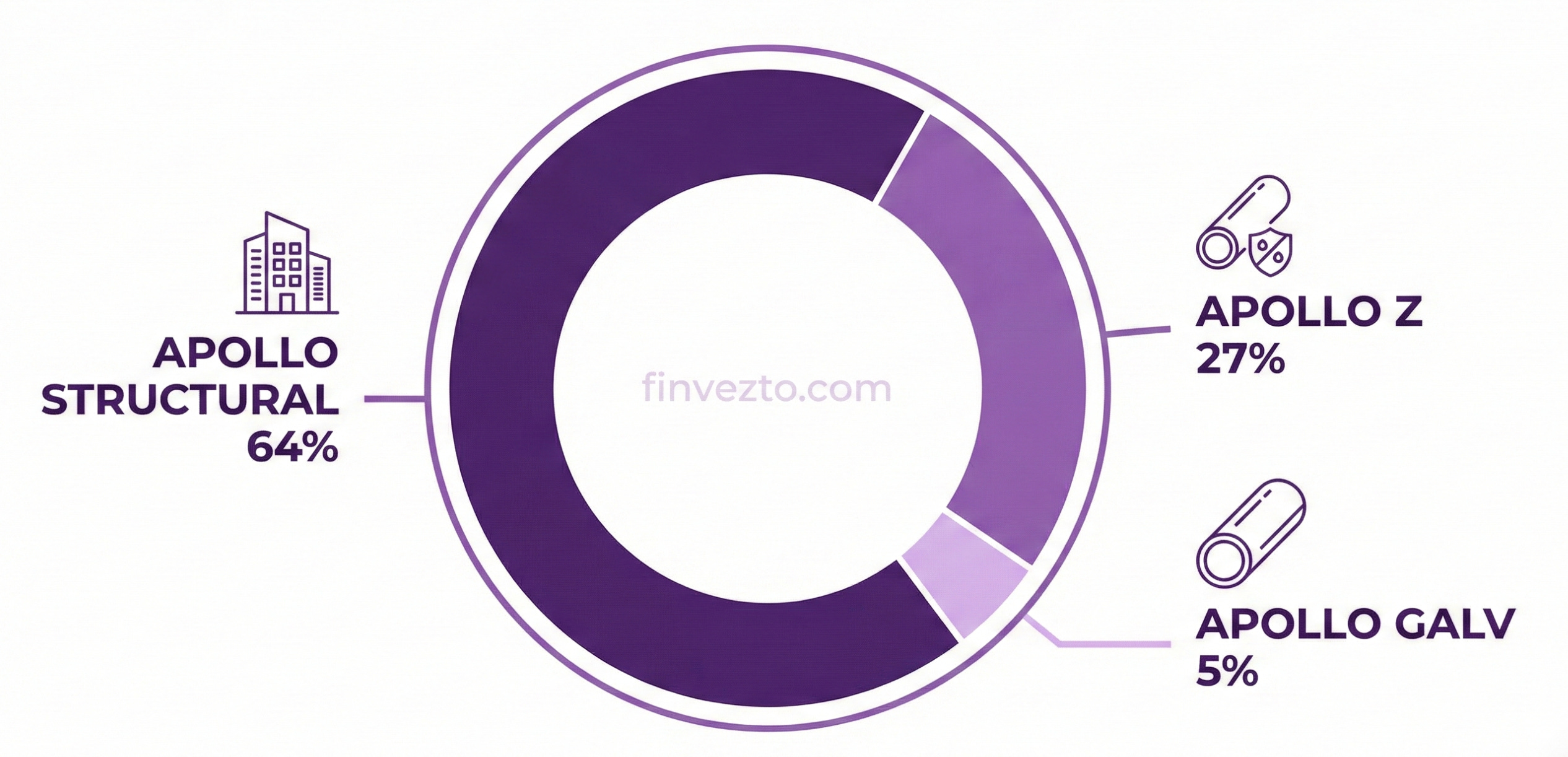

Revenue Mix

The core product portfolio splits into three categories. Each segment has distinct pricing and margin profiles.

Apollo Structural forms 64% of volume, used in residential and commercial buildings.

Apollo Z coated products contribute 27%, targeting high-corrosion environments.

Apollo Galv galvanized pipes add the remaining 5% for agricultural and industrial use.

Revenue grew from ₹7,723 crore in FY20 to ₹20,690 crore in FY25. Volume followed, climbing from 1.63 million tonnes to 3.16 million tonnes. It is continuing to increase in FY26 as well.

Customer Mix

The customer mix tilts heavily toward real estate.

Residential housing drives 67% of revenue.

Commercial construction adds 19%.

Infrastructure projects contribute 10%.

Industrial and agricultural applications round off the final 4%.

This housing concentration ties the business tightly to India’s real estate cycle. Not a pure infrastructure play.

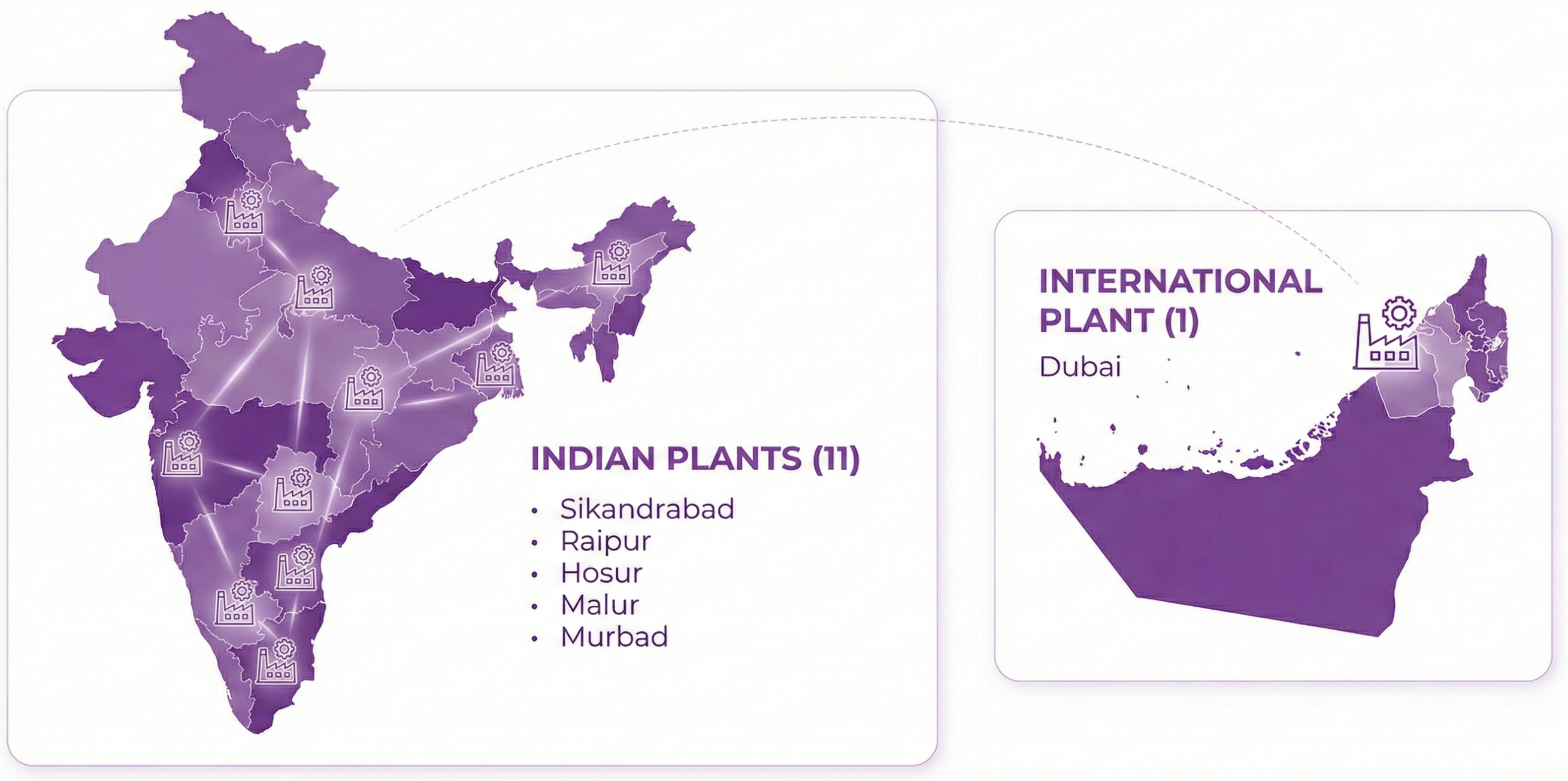

Location Mix

The company operates 11 Indian plants and one international facility in Dubai.

Indian Plants are strategically spread across Sikandrabad, Raipur, Hosur, Malur, and Murbad.

Decentralized manufacturing cuts freight costs significantly. It also enables a 48-hour delivery commitment that keeps distributors loyal.

2. DFT Technology Edge

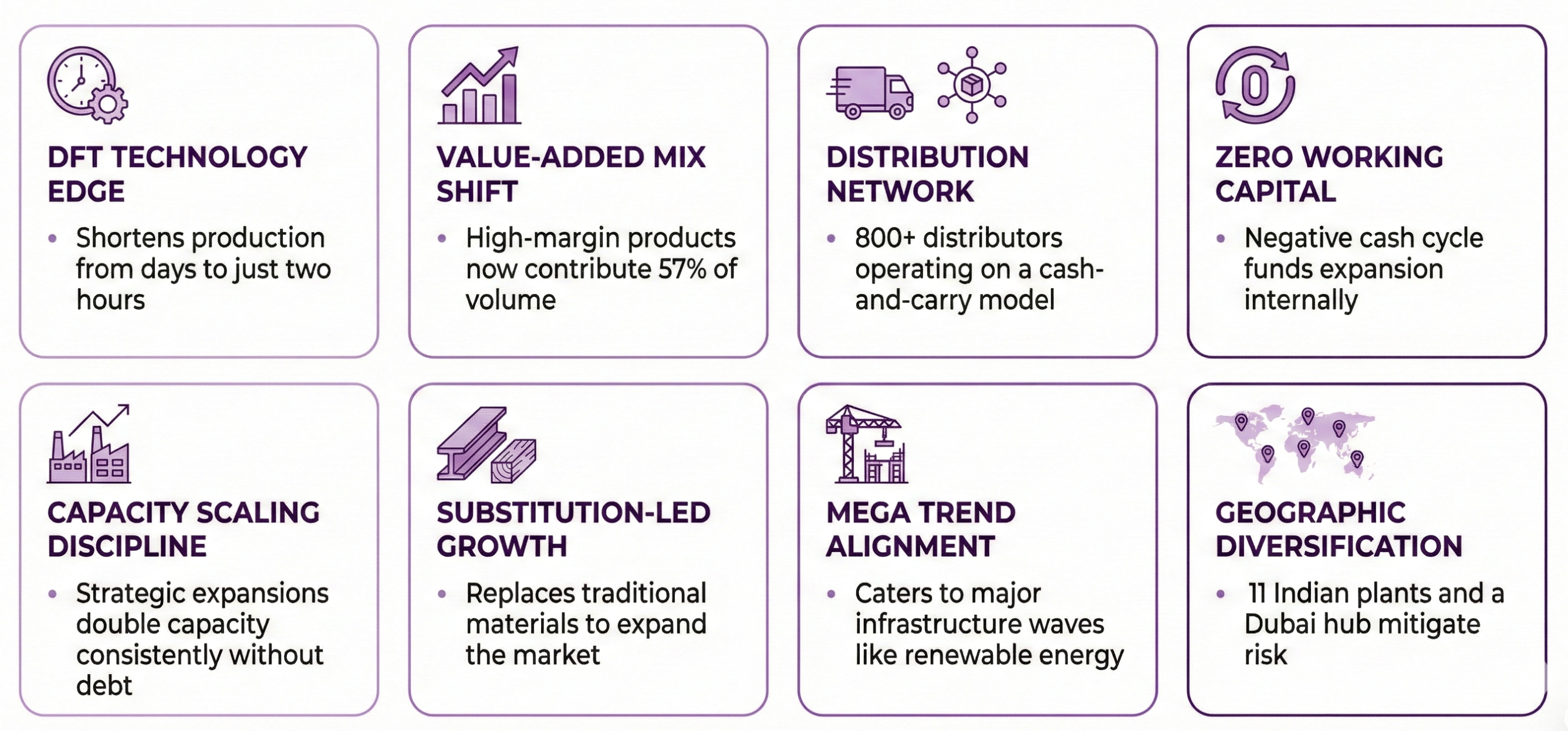

Direct Forming Technology is the manufacturing backbone that separates APL Apollo from other domestic competitors. Imported from Italian firm Olimpia 80 and first deployed at Hosur in FY17, DFT forms flat steel strip directly into the final structural shape, skipping the intermediate round-tube step entirely. APL Apollo now runs DFT across all 11 Indian plants.

- Bringing The Cutting-Edge Italian Technology For The First Time In India - APL Apollo")

Conventional ERW tube-making requires a two-step process. Steel strip is first formed into a round, then cold-reformed into square or rectangular shapes.

DFT eliminates the intermediate round step entirely. Production time drops from two days to just two hours. That is not a huge efficiency gain.

The raw material savings alone justify the investment. DFT generates 2% to 10% less scrap because there is no round-to-square reshaping wastage.

Conversion costs drop by approximately 10% compared to conventional mills. Every tonne of steel saved flows straight to the bottom line. Even small percentages at 3.16 million tonnes of volume add up fast.

Minimum batch sizes shrink from 400-550 tonnes to just 10-20 tonnes. This unlocks the ability to fulfill highly customized architectural orders economically.

For example, a Hospital needing 500x500mm columns requirement gets a quick turnaround. Conventional competitors cannot match this flexibility without massive minimum orders.

Software-controlled roll stands eliminate physical changeover downtime. Size changes happen automatically between orders. There is no manual intervention and no production stoppages. This is what enables 3,000+ SKUs across a size range of 8x8mm to 1,000x1,000mm. No other company globally covers this full spectrum.

By FY25, all 11 Indian plants run DFT. Competitors have not matched this rollout. First-mover advantage.

But what is worth noting is that the DFT equipment is becoming more accessible. Indian equipment makers like MKK Metal Sections now operate DFT mills. So, this MOAT for APL Apollo is not permanent.

3. Value-Added Mix Shift

The most important financial transformation at APL Apollo is the product mix upgrade from commodity pipes to premium structural solutions. Value-added products (VAP) now contribute 57% of volume, up from 40% just 2 years ago. This shift decouples profitability from basic steel price cycles and improves EBITDA per tonne significantly.

The EBITDA differential across product categories is stark. General structural pipes earn roughly ₹1,700 to ₹2,000 per tonne. Heavy structural products deliver ₹7,865 per tonne. Coated Apollo Z products generate ₹5,351 per tonne. Selling more of the right products matters more than selling more total volume.

Heavy structural tubes grew from 7% of mix in FY23 to 9% in FY25. That represents approximately 294,000 tonnes of high-margin steel. These tubes replace RCC columns in hospitals, airports, and high-rise buildings.

Apollo Z coated products jumped from 2% mix in FY23 to 6% in FY25. Coastal construction markets now have a purpose-built product that resists salt air corrosion over decades. Customers in these regions willingly pay a premium for guaranteed longevity. Premium pricing, loyal customer base.

steel tubes for coastal regions - Construction Week India")

The Raipur Simga plant serves as the primary engine for premium production. Commissioned in Dec 2022 across 190 acres, it handles India’s largest hollow sections and color-coated tubes. It operated at 70% utilization by Q2 FY26 with more room to run.

Blended EBITDA per tonne reached ₹5,146 in Q3 FY26, a 23% year-on-year improvement. Management targets ₹5,500 per tonne blended by FY27.

A price hike of ₹2,000 to ₹3,000 per tonne on general products was implemented in Jan 2025. The market absorbed this entirely without any demand drop. Pricing power exists.

The SG Premium sub-brand targets the price-sensitive unorganized segment. Priced at ₹5,000 per tonne below the flagship Apollo brand, it steals volume from local scrap-steel players without cannibalizing the premium line.

Management targets 70% value-added mix by FY28.

4. Distribution Network

APL Apollo’s 800+ distributor network, spanning 50,000 retailers and 200,000 fabricators across 2,000+ Indian towns is one of their core strengths. This three-tier system took decades to build.

Remember the 48-hour delivery guarantee that we mentioned earlier. This generates capital efficiency for distributors. Distributors rotate their invested capital up to 8 times annually. This makes them loyal.

Cash and carry model was implemented across the entire network in 2021. Distributors pay before the products leave the APL Apollos’ factory gate. Debtor days collapsed from 23 days to just about 3 to 5 days. Credit risk almost at zero.

The Aalishaan digital app directly engages 30,000+ fabricators. This digital layer builds a direct ecosystem around the brand. Fabricators are skilled installers who cut, shape, assemble, and fit materials on-site, strongly influencing brand choice and reorders. Fabricators become advocates. Advocacy converts to reorders.

APL Apollo conducts regular fabricator meets to expand structural steel applications. Teaching local welders new installation techniques grows the market itself, not just APL Apollo’s share. This is a long-term investment in demand creation.

When fabricators recommend a specific brand to homeowners, price resistance vanishes. Influencer Marketing at industrial scale.

29 warehouse-cum-branch offices support logistics coordination nationally. SG Green Logistics Private Limited manages heavy material movement across this network. Efficient logistics prevents bottlenecks at factory gates.

The network absorbed a record 916,976 tonnes in Q3 FY26. Moving nearly one million tonnes of heavy steel in three months requires completely coordinated logistics. Capacity for the product and capacity for the distribution must grow together.

Mr. Amitabh Bachchan has been brand ambassador since November 2019. Mr. Tiger Shroff promotes Apollo Column. IPL sponsorship with Delhi Capitals brings mass visibility. Retail homebuilders now walk into hardware shops and specifically request the Apollo brand. Industrial products rarely achieve this kind of consumer recall.

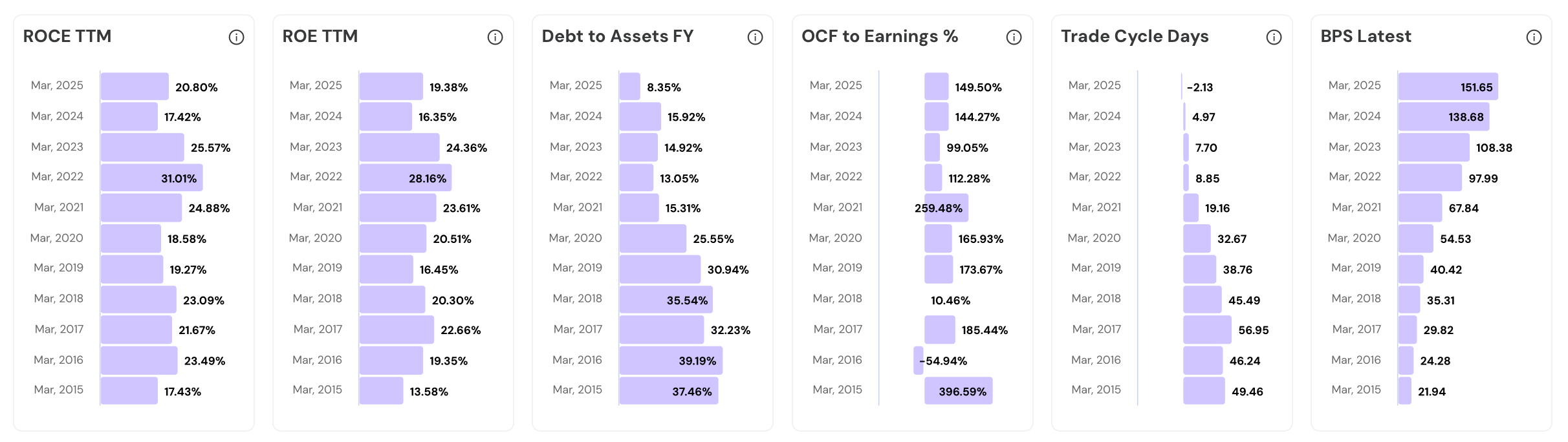

5. Zero Working Capital Engine

APL Apollo’s financial model is structurally unusual for a manufacturing company. Net working capital days collapsed from 25 in FY20 to 0 in FY25. The cash conversion cycle turned negative at minus 8 days, meaning the company collects cash before paying suppliers. This negative working capital funds growth without external borrowing.

Ten years ago, APL Apollo waited 81 days to collect payments. By FY25, it collected in 3 to 5 days. This improvement happened through disciplined implementation of cash-and-carry across 800+ distributors. Behavioral change at this scale is operationally difficult. But, they have pulled it off.

Operating cash flow reached ₹1,213 crore in FY25. The OCF-to-EBITDA ratio exceeded 100%, meaning every rupee of operating profit converted to cash.

In FY26’s first 9 months, the net cash position stood at ₹560 crore. Cash on the balance sheet exceeds total borrowings. A steel company with a solid balance sheet.

The negative working capital model funds capacity expansion entirely from internal cash flows. ₹2,370 crore of cumulative capex was executed between FY20 and FY25 without net borrowing. The balance sheet moved from ₹790 crore net debt to ₹310 crore net cash parallely. Building factories + Reducing debt. Extra-Ordinary.

DFT accelerates inventory turns by compressing production time to two hours. Steel coils never sit idle. Raw material becomes finished tube almost immediately. High inventory churn minimizes exposure to sudden HRC price drops. This is the operating mechanism behind the financial efficiency numbers.

Unutilized working capital limits with partner banks exceed ₹5,700 crore. This liquidity buffer provides acquisition firepower if an opportunistic deal surfaces. More importantly, it ensures operations remain unaffected during any macroeconomic stress. A zero-debt company with ₹5,700 crore of untapped credit is effectively indestructible in downturns.

6. Capacity Scaling Discipline

APL Apollo has consistently doubled its manufacturing capacity every few years without borrowing. The company follows a clear expansion framework: brownfield additions at existing sites for speed, greenfields at untapped geographies for long-term market capture.

Brownfield expansions are underway at Dubai (+200K tonnes), Raipur roofing (+500K tonnes), and Raipur heavy (+100K tonnes). These add 800,000 tonnes in aggregate. Adding capacity to existing sheds is faster than building new factories. Speed to market matters when demand is growing.

Greenfield plants are coming up in 4 strategically chosen locations. Gorakhpur adds 200,000 tonnes for eastern Uttar Pradesh. Kolkata adds 300,000 tonnes for eastern India and the northeast. Bhuj adds 300,000 tonnes inside a Special Economic Zone near a port. New Malur adds 360,000 tonnes for South India. Each location plugs a specific supply gap.

The Dubai plant hit 80% to 85% capacity utilization by early FY26. It produced 145,000 tonnes in FY25 at ₹7,000 to ₹8,000 per tonne EBITDA, dramatically above domestic averages. Middle Eastern infrastructure spending creates pricing premiums.

The Bhuj plant sits inside an SEZ, eliminating multiple domestic taxes. Port proximity slashes inland transport costs for export shipments. This gives APL Apollo mathematically better export pricing than any inland competitor. Targeting African and European markets from Bhuj creates a structural cost advantage.

Current capacity utilization at approximately 70% provides significant volume headroom. New plants are not urgently needed to meet demand.

Management has articulated a longer-term vision of 8 to 10 MTPA by FY30.

4 dedicated 250,000-tonne plants for super specialty tubes are planned for this phase. These facilities will target aerospace and heavy engineering applications. Whether this vision materializes depends on demand signals from these niche sectors.

7. Substitution-Led Market Creation

APL Apollo does not merely compete for market share in existing segments. It creates new demand by replacing wood, aluminum, and concrete with steel tubes. This substitution strategy expands the total addressable market. The company grows the pie, then takes the largest slice of the larger pie.

India’s structural steel tube consumption stands at 6.5% of total steel output. Europe sits at 11%, Japan at 8%, and the global average is 9%.

If India converges toward global norms, the market grows from roughly 4.5 million tonnes today to 17.3 million tonnes by 2030.

APL Apollo’s 55% market share positions it as the primary beneficiary.

Apollo Chaukhat is replacing traditional wooden door frames after its Feb 2021 launch.

These closed steel frames are termite-proof, fire-resistant, and cheaper than quality timber over their lifespan.

500x500mm heavy structural tubes physically replace RCC columns in commercial buildings. Steel construction erects a multi-storey framework in 8 days per slab. RCC takes 24 days. Speed is money for developers paying construction financing costs.

The 1,000x1,000mm column launched from Raipur is the first in India and only the second globally. Global mega-projects needing this size essentially have only one non-Chinese option. APL Apollo captures this demand.

Apollo Fence replaces concrete boundary walls and agricultural wooden posts. The patented H-shaped tube is lighter, faster to install, and more durable. Rural farmers adopt it quickly because the total cost of ownership over a decade is lower.

Pre-engineered building customers now specify APL Apollo tubes instead of solid steel angles. The hollow tubular shape provides a higher strength-to-weight ratio for equivalent load-bearing capacity. This reduces total steel consumption per structure. Builders get stronger buildings with less material cost.

Now all the products above are relatively new. Customer segments are new. But the distribution network will be the same. This leads to high asset efficiency.

8. Mega Trend Alignment

APL Apollo is structurally aligned with India’s largest infrastructure spending waves. Renewable energy, airport modernization, metro rail expansion, data center construction, and warehouse growth all require structural steel tubes. The company designs products specifically for these applications, securing long-term volume pipelines tied to government capex commitments.

India targets 500 GW of renewable energy by 2030. This creates immediate demand for approximately 830,000 tonnes of specialized solar mounting structures. APL Apollo targets a 15% market share in this segment, translating to 125,000 tonnes of incremental volume annually. Rust-proof galvanized tubes are the core product here. A new demand stream.

APL Apollo tubes currently support roofs at Leh Airport, Kushinagar Airport, and Bengaluru’s Terminal 2.

11 airport projects across India are underway using their structural tubes.

Airports require both high load-bearing capacity and aesthetic appeal. APL Apollo’s premium sections uniquely serve both requirements.

Metro rail expansions require continuous heavy structural steel. Indore Metro, Chennai Metro, and Bhubaneswar Metro are confirmed supply relationships. Elevated station frameworks rely almost entirely on steel structures. As metro networks expand to 50+ cities over the next decade, this demand compounds year after year.

Railway station redevelopments are an underrated volume driver. More than 1,500 station redevelopments are expected over the next five years. New Delhi station is among the flagship projects. Steel construction above live train tracks requires prefabricated structures.

Data center construction requires massive, fast-erected structural buildings. Heavy steel columns provide the load-bearing capacity for thousands of server racks. Steel structures cure in days, not in weeks like concrete. APL Apollo is well positioned here.

Post-GST, e-commerce mega-warehouses have become a structural growth driver. Companies like Amazon, Flipkart, and Delhivery are building million-square-foot distribution centers. Wide-span roofing tubes create column-free interior spaces. These spaces allow autonomous forklifts to operate without obstruction. Warehouse design is evolving.

The Jal Jeevan Mission drives demand for water infrastructure nationwide. APL Apollo demonstrated a 200,000-litre steel water tank installed in 3 days versus 4 to 5 months for RCC. Sister company Apollo Pipes handles PVC and HDPE piping for the same mission. The Apollo ecosystem captures multiple layers of this government spending.

Healthcare sector expansion is creating consistent high-margin volume. Large hospital chains are aggressively building multi-city branches. Hospital construction demands vibration-free, structurally predictable frameworks. Pre-fabricated heavy steel tubes offer reliable structural integrity for sensitive medical equipment environments. APL Apollo has 45 heavy structural projects covering 42 million square feet in its active pipeline.

9. Geographic Diversification

APL Apollo is systematically eliminating its geographic concentration risk. The company is simultaneously building toward 10% export revenue by FY28, penetrating underpenetrated eastern Indian markets, and scaling the Dubai operation into a dedicated international hub.

The Dubai plant operates at 80% to 85% utilization. It produced 145,000 tonnes in FY25, generating ₹7,000 to ₹8,000 per tonne EBITDA. Middle Eastern pricing premiums are structurally higher because fewer regional alternatives exist. Exports currently represent 6% of total sales.

APL Apollo exports to 30 countries, shipping 3,000+ distinct tube specifications. No single foreign market creates dangerous concentration. This international diversification also provides currency revenue streams that partially hedge domestic input costs.

Eastern India remained significantly underserved by APL Apollo until recently. Gorakhpur will add 200,000 tonnes targeting eastern Uttar Pradesh. Kolkata will add 300,000 tonnes for eastern India and the northeast. These regions were served by smaller, fragmented local players.

Having 11 geographically dispersed plants is a natural hedge against localized disruptions. For example, monsoon flooding in Tamil Nadu does not halt Uttar Pradesh production.

The Dubai subsidiary benefits from significantly lower corporate tax rates. International profits face lower tax burdens than domestic Indian operations. This mathematically reduces the consolidated group tax rate as the export mix grows. It is an underrated financial benefit of the international expansion strategy.

10. Risks and Red Flags

APL Apollo carries specific risks that require monitoring alongside its structural strengths.

A June 2020 SEBI order barred CMD Sanjay Gupta from securities markets for 2 years. The violation fell under Prohibition of Fraudulent and Unfair Trade Practices regulations. The company called it historical and minor. For the CMD of a ₹45,000 crore market cap company to carry a PFUTP finding is not a footnote. It is a black mark.

The Apollo TriCoat transaction sequence raised arm’s-length concerns. Rahul Gupta (Sanjay’s son) acquired a shell company, renamed it Apollo TriCoat, built it using APL Apollo’s distribution infrastructure, then sold it back to APL Apollo’s subsidiary. The entity merged into APL Apollo at a 1:1 share exchange in Oct 2022.

Related party transactions with APL Apollo Mart, Apollo Metalex, and SG Green Logistics require ongoing scrutiny. The company regularly lends money and trades goods with promoter-linked entities.

HRC constitutes approximately 85% of cost structure, making margins acutely sensitive. In Q2 FY25, a ₹7,500 per tonne steel price decline caused inventory losses of approximately ₹2,000 per tonne.

Competition in the premium heavy structural segment is intensifying. Jindal Steel and Power has emerged as the most formidable challenger. Management acknowledged rising competitive pressure during FY25 earnings calls. A ₹500 per tonne discount offered in Q2 FY25 suggests pricing discipline can slip during competitive stress. The 55% market share is not permanent.

The unorganized segment still controls approximately 50% of the ERW pipe market. Local scrap-steel players compete aggressively on price in regional markets. The SG Premium sub-brand attempts to address this. However, competing against informal players on price is a race toward margin erosion if not managed carefully.

Income Tax raids were conducted on company premises in Jun 2023. Unresolved tax investigations create contingent liabilities that cannot be quantified upfront. Management stated normal operations continued.

Summary: Growth and Consistency drivers

That’s it for today.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

FINVEZTO.COM | Build Wealth. With Clarity.

We give you a proven Flexi-Wealth System to build a Resilient Portfolio that works across market cycles. We believe your Wealth should be flexible enough to give you more options throughout your life. Learn more about the system at finvezto.com

Enjoyed reading your post on APL Apollo Tubes, very in depth and through . Have been invested since 2017. Could you or have you done a Deep Dive into Laurus Labs . Would make an Interesting study. Tks