₹1,70,000+ Crore Sold in last 2 months. But FIIs Are Quietly Betting on This Theme in India.

There is a theme-driven rotation that is happening beneath the surface.

In this Article…

What FII Flow Data Actually Tells You

The Fortnight at a Glance

Theme 1: The India Energy Infrastructure Bet

Theme 2: The Commodity Play

Theme 3: The Systematic Unwind of IT, Healthcare, and Consumer Services

Theme 4: Financial Services Is Being Reduced, Not Exited

Theme 5: Oil and Gas Exit

What This Means in Aggregate

Before we begin the analysis, let me just brief you on what the FII flow data actually is.

What FII Flow Data Actually Tells You

Foreign Institutional Investors (FII) are the largest category of external participants in Indian equity markets. They include global pension funds, sovereign wealth funds, hedge funds, and large asset management firms operating out of the US, Europe, and Asia.

Their buying and selling moves prices, shifts sector valuations, and often precedes broader market trends by several weeks.

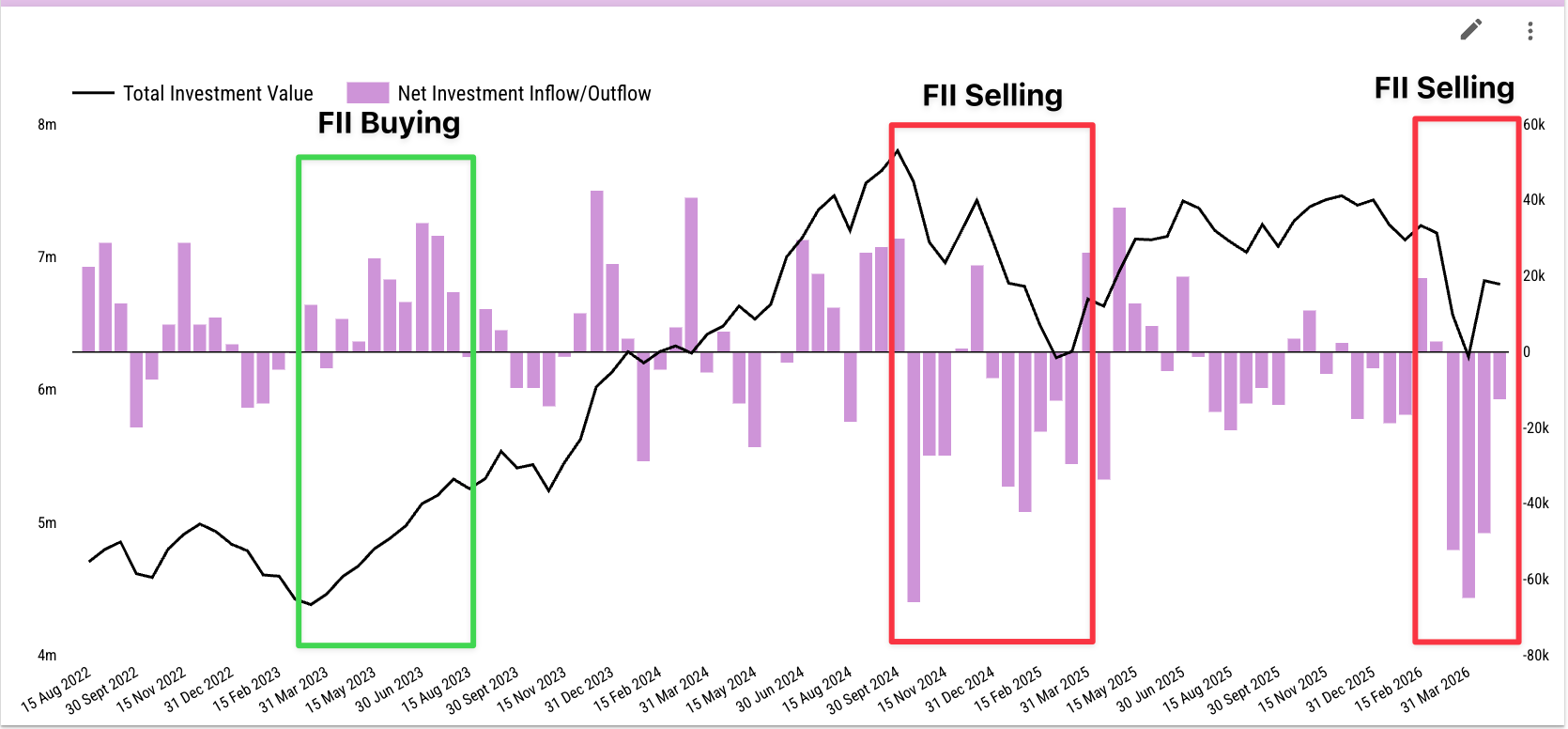

Look at the chart below. The green box marks a period of sustained FII buying from early 2023, and the black line shows total FII investment value climbing steadily through that phase. The two red boxes mark the major selling episodes in late 2024 and early 2026, with the black line dropping sharply each time. The correlation is direct. When FIIs buy consistently, markets rise. When they sell in streaks, markets fall.

Heavy Selling in the last 2 Months

FIIs have sold approximately ₹1,70,000+ crore of Indian equities in the last 2 months alone.

That number gets most of the attention. But the sectoral breakdown tells a different story.

Within the selling, there is a rotation happening. Certain sectors are being bought across every fortnight even as everything else is sold.

Understanding that rotation is more actionable.

The Recent Fortnight at a Glance

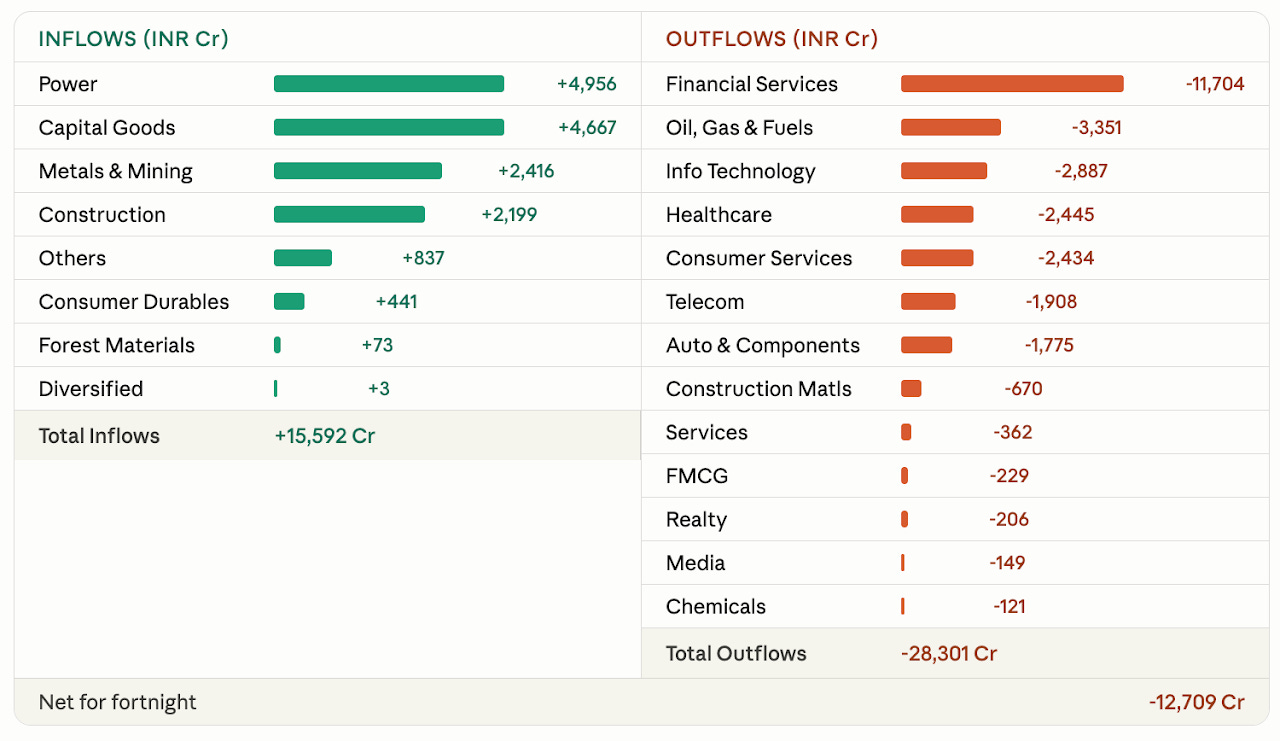

This article covers the data till the latest fortnight of April 16-30, 2026.

Total inflows this fortnight (Apr 16-30) were ₹15,592 crore. Total outflows were ₹28,301 crore. Net selling was ₹12,709 crore.

That ₹12,709 crore figure matters for context. The prior fortnight saw net selling of ₹48,141 crore. This is the smallest net outflow in six fortnights. Selling pressure is not gone, but the peak appears to have passed.

On the inflow side:

Power received ₹4,956 crore and Capital Goods received ₹4,667 crore. These were the only two sectors with significant net buying.

Metals and Mining added ₹2,416 crore and Construction added ₹2,199 crore.

Everything else on the inflow side was marginal.

On the outflow side:

Financial Services led all selling at ₹11,704 crore.

Oil, Gas and Consumable Fuels lost ₹3,351 crore.

IT lost ₹2,887 crore, Healthcare lost ₹2,445 crore, Consumer Services lost ₹2,434 crore, and Telecom lost ₹1,908 crore.

Five clear themes emerge when we connect the latest fortnight data with the previous fortnights.

Theme 1: The India Energy Infrastructure Bet

FIIs are placing a concentrated, consistent bet on India’s physical energy buildout.

Power at +₹4,956 crore and Capital Goods at +₹4,667 crore are the two largest inflows this fortnight by a wide margin. Construction at +₹2,199 crore adds a third leg to the same thesis. Together, these three sectors absorbed ₹11,822 crore in net buying even as everything else was being sold.

India’s installed non-fossil fuel capacity has tripled to over 250 GW since 2014. India has committed to 500 GW of renewable capacity by 2030.

Achieving that target requires an estimated ₹25-26 lakh crore in sectoral investment through FY2030. It is a contracted pipeline that underpins cash flows for Power sector companies.

Capital Goods companies making turbines, transformers, switchgear, and transmission equipment are the direct supplier chain to power companies.

FII buying in Capital Goods is not a separate bet. It is buying the enabler of Power’s growth. The two sectors move together because they are structurally linked.

The Union Budget 2026-27 raised public capex to ₹12.2 lakh crore. Rail, roads, and urban infrastructure all create new demand centers that require uninterrupted power supply. This extends the Power sector opportunity beyond renewable generation alone.

AI data centers are becoming a meaningful driver within this theme. Data centers in India require 24x7 reliable baseload power. Their expansion is creating a structural demand floor that makes Power sector cash flows increasingly predictable for foreign investors with long holding horizons.

FIIs have been accumulating in Power and Capital Goods across multiple fortnights even as they sold out of almost everything else.

The weight of Capital Goods in FPI holdings has risen 0.29% in FY27 to date. Power has risen 0.12%. Both are rising despite aggregate outflows.

Theme 2: The Commodity Play

Metals and Mining at +₹2,416 crore in the latest fortnight flipped from -₹1,198 crore in the prior fortnight.

The immediate trigger was the US-China tariff escalation in early 2026. Chinese steel, aluminum, and base metal exports are being redirected away from the US market. This has created a global commodity repricing event. That is, in some markets, it created price pressure from oversupply. In others, it created supply tightness.

India’s domestic steel companies benefit from this position. They have large captive ore bases and are selling into a domestic consumption story.

The tariff disruption makes them relatively more attractive compared to producers exposed to the US-China trade corridor.

Construction’s return to buying reinforces the commodity thesis. Infrastructure activity consumes steel, cement, and aggregates domestically.

FII buying in both Metals and Construction at the same time is not a coincidence. It signals conviction on India’s internal demand for commodities, driven by the same capex cycle that is supporting Power and Capital Goods.

Theme 3: The Systematic Unwind of IT, Healthcare, and Consumer Services

IT at -₹2,887 crore, Healthcare at -₹2,445 crore, and Consumer Services at -₹2,434 crore collectively account for ₹7,766 crore in outflows this fortnight.

All three were FIIs’ primary overweight positions through FY2024. All three have been sold in nearly every fortnight since.

The IT sell-off has two distinct layers.

The cyclical layer is US macro. Rising inflation expectations compress US growth forecasts, which reduce IT order books for Indian vendors. Deal ramp-up timelines are lengthening. Discretionary spending on legacy modernization is being deferred in favor of internal AI buildouts at large US enterprises.

The structural layer is more permanent. AI is fundamentally rethinking what software development costs. Agentic coding tools are compressing the number of engineers required to deliver the same output. Indian IT’s core value proposition was labor arbitrage at scale. That moat is being eroded from both ends. Clients are doing more with fewer seats, and the margin on each seat is under pressure.

Large US enterprises that anchor the revenue of TCS, Infosys, Wipro, and HCL are actively renegotiating contracts. The conversation has shifted from “how many Engineers do we need” to “how much of this can AI handle.” FIIs see this structural shift clearly, and they are pricing it into their holdings.

Telecom at -₹1,908 crore is being sold for a related reason. Telecom was the infrastructure play for India’s digital economy. If the software layer of the digital economy is being compressed by AI, the downstream demand assumptions for bandwidth, enterprise connectivity, and managed services weaken in parallel. The Telecom outflow is a downstream consequence of the IT thesis.

Consumer Services has now seen 11 consecutive fortnights of net outflows. That is one of the longest single-sector selling streaks. Consumer Services includes hospitality, airlines, and discretionary experience spending. This sector’s sell-off is driven by war and global risk-off sentiment. High-PE consumption-driven sectors with limited margin buffer lose allocation first when global risk appetite contracts.

Theme 4: Financial Services Is Being Reduced, Not Exited

Financial Services saw -₹11,704 crore this fortnight. That is the largest single-sector outflow.

FIIs are reducing their Financial Services exposure, not exiting. The distinction matters. Reducing means they still hold a large position and are trimming. Exiting would mean a fundamental reassessment of the sector’s prospects.

The evidence supports the reducing interpretation. Despite persistent net selling, the sector’s weight in FPI holdings has actually risen 0.57% in FY27 to date. The reason is price appreciation. Nifty Bank and Nifty Financial Services have both risen, so even as FIIs sell units, the rupee value of their remaining position has gone up.

The selling in Financial Services is not a bear call on Indian banks or NBFCs. It is an emerging market risk-off response driven by two macro factors.

US 10-year yields remain elevated, making dollar assets more attractive relative to EM assets on a risk-adjusted basis.

The Iran conflict has added a geopolitical risk premium that reduces appetite for high-beta EM exposure.

When either of those conditions reverses, Financial Services is likely to be the first sector where FII net buying returns. Historically, every major FII buying wave in India has started with Financial Services.

If the April 30 fortnight is indeed a turning point in the aggregate selling cycle, watch Financial Services flows in the next two fortnights as the early indicator.

Theme 5: Oil and Gas Exit

Oil, Gas and Consumable Fuels has been consistently among the top three sectors for outflows across the last 12 months. This fortnight’s -₹3,351 crore continues that trend.

The weight of Oil, Gas and Consumable Fuels in FPI holdings has declined 0.57% in FY27 to date. That is the single largest weight reduction of any sector. FIIs are reducing exposure in absolute rupee terms, not just as a percentage of a rising portfolio.

Two dynamics explain the selling.

First, the macro headwind. Higher crude prices from West Asia tensions raise India’s import bill, worsen the current account deficit, and reduce the appeal of rupee-denominated assets. Global FPI debt flows out of India were negative at USD 1.9 billion in April 2026. Part of that is oil-linked.

Second, and more structurally, the energy transition is a real capital allocation decision. Money coming out of oil refiners and gas distributors is moving into power generators and capital goods manufacturers. It is a rotation from the old energy economy to the new one.

What All This Means in Aggregate

When we connect the data from the previous fortnight, they tell a coherent story.

Exit the old economy: oil and gas, legacy IT labor arbitrage, rate-sensitive high-PE consumption plays.

Enter the new economy: India’s physical energy infrastructure, the capital goods supply chain, and domestic commodity demand.

Financial Services sits in the middle. It is being reduced due to macro conditions that have nothing to do with India’s banking fundamentals. It will likely be restored when those macro conditions improve.

What is already confirmed is the sectoral direction. FIIs have voted consistently with their money across multiple fortnights.

Power, Capital Goods, and domestic infrastructure are where global conviction sits right now. Everything else is either being trimmed or actively exited.

That’s it for today.

FINVEZTO.COM | Build Wealth. With Clarity.

Disclaimer: Anand Ganapathy K is a SEBI-registered Research Analyst with SEBI registration number INH000016630. This post is purely for learning purposes. I do not recommend buying or selling stocks mentioned in this newsletter. I do not hold any positions in the stock discussed. Securities market investments carry market risks. Kindly review all related documents before investing.

Fantastic article.

Very thoughtful and researched analysis.👍